In Pain? Call Caine

Can You Sue an Insurance Company? A Florida Guide

5 Min read

By: Caine Law

Share

You did what people are told to do. You reported the crash. Got medical care. Turned over the paperwork and answered the adjuster’s questions. Then the letter came, or the phone call, or the offer that did not come close to covering what happened to you.

That is when the question gets real. Can you sue an insurance company?

Yes. In the right case, you can.

Sometimes the problem is simple. The insurer is refusing to pay as required by the policy. Sometimes it is worse. The company delays, misstates coverage, ignores proof, or treats a valid claim like a nuisance until the pressure forces the injured person to give up. That is where contract law, bad faith law, and careful litigation strategy matter.

In Florida, this is not just about frustration. It is about their strategic advantage. Insurance companies know many people are dealing with pain, missed work, family stress, and medical bills at the same time. They also know that many claimants do not know the difference between a denied claim and a legally actionable denial. That gap is where insurers gain ground.

An attorney who understands defense tactics can quickly close that gap. The point is not to file a lawsuit in every dispute. The point is to know when negotiation still works, when documentation is missing, and when the insurer has crossed the line.

Your Claim Was Denied: Is a Lawsuit Your Next Step

A common version of this starts the same way. A driver gets rear-ended at a light. The car is damaged. The neck and back pain get worse over the next few days. Treatment starts. Time off work follows. Then the insurer comes back with an offer that covers only a fraction of the bills, or denies the claim outright with a thin explanation.

That moment feels personal, even when the company calls it routine. Many clients are not thinking about legal theories at first. They are thinking about rent, prescriptions, child care, and whether they are being blamed for asking to be treated fairly.

Why denials happen

Not every denial is illegal. Some claims fail because the policy does not cover the loss, the claimant failed to meet a requirement, or key evidence is missing. But some denials happen because the insurer takes an aggressive position and bets the claimant will not challenge it.

That pressure exists in a larger system. Insurance fraud costs American consumers at least $308.6 billion annually and occurs in approximately 10% of property-casualty insurance losses. Fraud is real, but honest claimants often get caught in the dragnet when carriers become overly suspicious, overly rigid, or overly focused on limiting payouts.

When a lawsuit makes sense

A lawsuit is usually not the first move. It becomes the next move when the insurer has had a fair chance to review the claim and still does one of the following:

Ignores clear evidence: Medical records, crash reports, photos, and witness statements all support the claim, yet the insurer acts as if they do not exist.

Misstates the policy: The adjuster points to an exclusion that does not apply, or describes the coverage in a way the policy language does not support.

Drags out the process: Delay becomes a tactic, not an investigation.

Makes a token offer: The offer is so disconnected from the documented damages that it signals the company is not evaluating the claim fairly.

A denial does not answer the legal question. It only tells you the insurer’s position. The next question is whether that position is defensible.

The practical answer to “can you sue an insurance company” is this: yes, but only after you identify what the company did wrong, what evidence proves it, and what law gives you a remedy. That distinction matters because anger alone does not win these cases. Documents, timing, and strategy do.

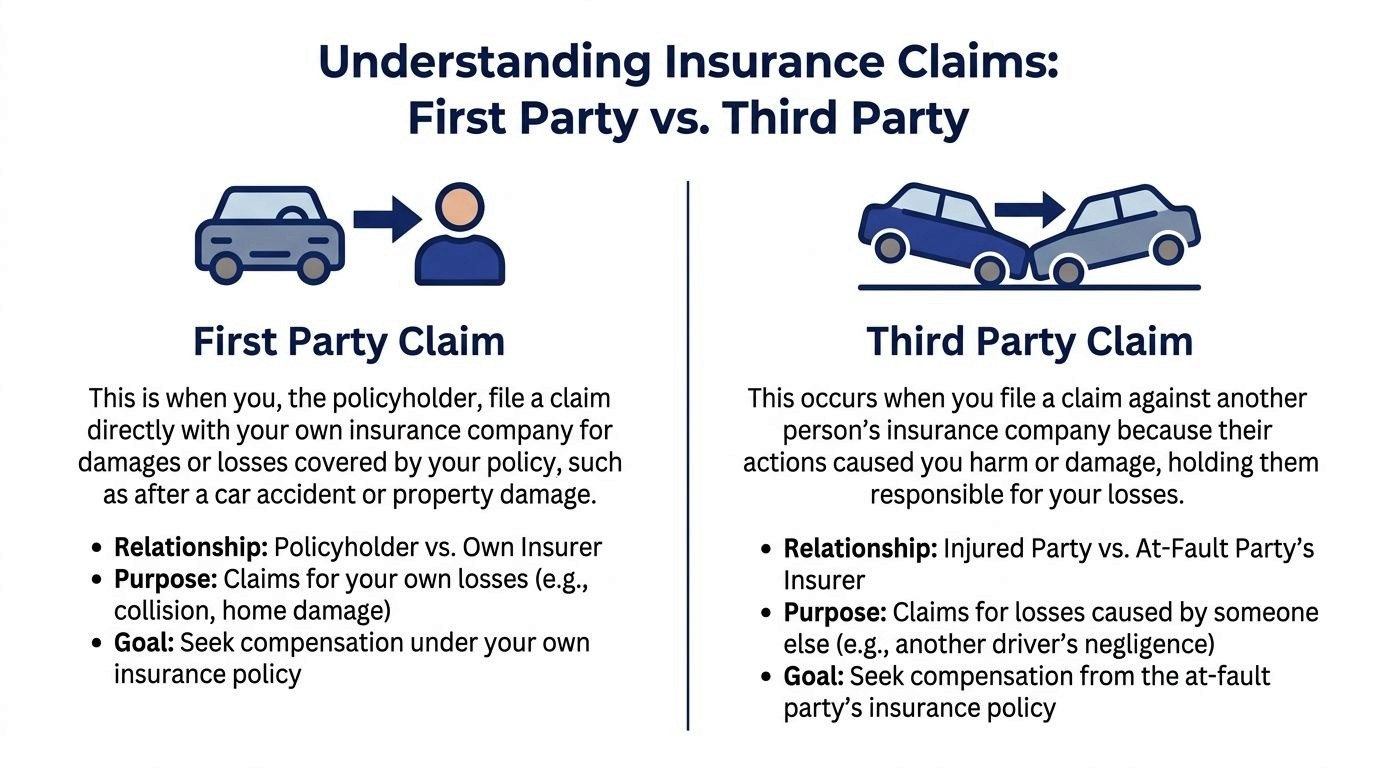

First Party vs Third Party Claims: Understanding Who You Can Sue

Before deciding whether to sue, you need to know which insurance company you are dealing with. That one issue changes the whole case.

The easiest way to understand it is this. One insurer is on your team, at least on paper. The other is on their team from the start.

First-party claims

A first-party claim is a claim you make under your own policy.

You paid premiums. The policy is a contract. You are asking your own insurer to provide a benefit that the contract says you bought in a Florida injury context, which can come up in several ways, including uninsured or underinsured motorist coverage and other policy-based benefits.

Because this is your insurer, the relationship matters. The company owes duties arising from the policy and the law governing claim handling. If it refuses to honor the policy without a valid basis, the issue may become more than a disagreement. It may become a contract dispute or a bad-faith dispute.

Third-party claims

A third-party claim is different. You are making a claim against the at-fault person’s insurer.

That company did not sell you a policy. You are not its customer. It does not owe you the same contractual duties as your own insurer. Its job is to protect its insured and resolve claims within the bounds of the law.

That means the tone often feels different. The third-party insurer may be tougher on liability, harder on damages, and less cooperative in general. That is not always misconduct. Often, it is merely the posture of an adversary.

Why this distinction changes strategy

If people miss this distinction, they often make avoidable mistakes. They assume every insurer has to “take care of them” because an accident happened. That is not how the legal relationship works.

Here is the practical difference:

Claim type | Who the insurer represents | What you are trying to enforce |

First party | Your own insurance company | The benefits promised in your policy |

Third party | The at-fault person’s insurance company | Compensation based on the at-fault person’s legal responsibility |

In a first-party dispute, the policy language becomes central early. In a third-party dispute, the fight usually starts with fault, causation, and the value of the injury claim.

What people often get wrong

They speak too freely to the wrong insurer: A recorded statement to an opposing insurer can create issues that didn't need to arise.

They assume delay means the same thing in every claim: Delay in a first-party claim may raise different legal issues than hard bargaining in a third-party claim.

They do not request the full policy: Partial information leads to bad decisions.

If you are asking, can you sue an insurance company? First, identify which insurance company it is with. That answer shapes the duty owed to you, the claim you can bring, and the evidence you need.

A lawyer with defense-side insight often spots this immediately. The insurer’s duty is not just a technical point. It determines whether you are enforcing a contract, pursuing a negligence-based injury case, or setting up a bad faith claim.

The Legal Grounds for an Insurance Lawsuit

Most insurance lawsuits fall into two broad buckets. Breach of contract and bad faith. They overlap, but they are not the same claim, and treating them as interchangeable is a mistake.

Breach of contract

A breach of contract case is the more straightforward of the two. The insurance policy is a contract. You paid premiums. The insurer promised certain coverage under certain conditions. If the company refuses to provide a covered benefit, that can be a breach.

Common examples include:

refusing to pay a covered loss under the policy

underpaying a claim despite clear documentation

applying policy language incorrectly

relying on an exclusion that does not fit the facts

In these cases, the central question is often narrow. What does the policy say, and did the insurer follow it?

That sounds simple, but insurers often create complexity by focusing on definitions, exclusions, notice requirements, prior conditions, or valuation disputes. Good contract cases are built by reading the entire policy, not just the denial letter.

Bad faith

Bad faith is more serious. It is not just “the insurer was wrong.” It is the insurer's act that was unreasonable in handling the claim.

The conduct matters. So does the process. A bad faith case may involve an insurer that failed to investigate, ignored evidence, misrepresented policy terms, delayed without justification, or used the claim process as a means to pressure a vulnerable claimant.

The legal concept of bad faith holds that insurance is not an ordinary product. A policyholder depends on the company to evaluate claims with integrity and fairness when the policyholder is under financial and medical stress. When the insurer abuses that position, the exposure can go beyond the unpaid amount.

The difference in plain terms

This comparison helps:

Issue | Breach of contract | Bad faith |

Core complaint | The insurer did not do what the policy required | The insurer handled the claim unfairly or unreasonably |

Main evidence | Policy language, denial letter, claim records | Claim handling conduct, delays, investigation failures, and misrepresentations |

Typical focus | Coverage and payment | The insurer’s behavior and decision-making |

A breach case asks, “Did they pay what they owed?”

A bad faith case asks, “How did they handle the claim, and was that conduct lawful?”

Examples that matter in real cases

Suppose the policy covers a particular loss, the documentation is complete, and the insurer still refuses payment because it reads the policy in a way that does not match the actual text. That leans toward breach of contract.

Now change the facts. The insurer delays for months, avoids responding directly to records, shifts reasons for denial, and never performs a fair investigation. That begins to look like bad faith conduct.

The same file can contain both issues. Many bad-faith disputes begin with an underlying breach of contract. But from a litigation standpoint, lawyers have to carefully separate the claims, preserve the right deadlines, and build the file in the right order.

Time limits can decide the case before the merits do

Deadlines matter early, not late. That is one reason waiting “to see what happens” can backfire. Even a strong claim becomes weaker if records disappear, witnesses become harder to reach, or a policy limit runs first.

A denial letter is not just a business communication. It is often the document that tells a lawyer whether the dispute is a contract fight, a bad-faith setup, or both.

The strongest cases are rarely built on outrage. They are built on a disciplined comparison between what the insurer promised, what it did, and what the claim file shows.

Florida's Rules for Suing an Insurance Company

Florida gives injured people tools to challenge unfair insurance conduct, but the process is technical. If you miss a required step, a strong claim can get delayed or thrown off course.

Florida bad faith law

Florida’s main bad faith statute is § 624.155. In practical terms, it allows an insured person, and in some situations others with a qualifying interest, to pursue a claim when an insurer fails to act fairly and ethically under the circumstances.

That does not mean every denial becomes a bad-faith case. Florida law still requires proof. The file has to show more than frustration, more than a low offer, and more than a disagreement over value.

A viable case often involves conduct such as:

Unreasonable delay: The insurer sits on the claim without a legitimate reason.

Misrepresentation: The company misrepresents the policy or the facts.

Failure to investigate: The insurer concludes first and looks for support later.

Ignoring cure opportunities: The company has a fair chance to fix the problem, but chooses not to.

The Civil Remedy Notice requirement

Florida claimants often hear about bad faith before they hear about the procedural gatekeeping. That is backward. Procedure is everything here.

Before filing many bad-faith actions, the claimant must serve a Civil Remedy Notice (CRN). The notice identifies the conduct at issue and allows the insurer to cure.

This is not a throwaway document. A weak CRN can create unnecessary fights later. An overly vague one can fail to preserve the issues clearly. A rushed one can box the case into arguments you did not need to make.

Why careful drafting matters

The CRN should line up with the actual record. That means counsel needs the policy, correspondence, adjuster communications, denial rationale, and supporting proof before treating the notice as a formality.

Problems that show up often include:

Mistake | Why does it hurt the case |

Vague accusations | The insurer argues it was not given fair notice |

Missing policy language issues | The notice may not match the later lawsuit |

Incomplete factual detail | It weakens your position's strength during the cure period |

Florida-specific remedies

Florida law can increase the stakes for insurers that act improperly. That does not mean punitive damages are routine. They are not. But the availability of those damages changes the conversation when the conduct is serious, and the proof is strong.

What works in Florida disputes

Florida insurance cases often turn on preparation rather than drama.

The approaches that tend to work are:

Get the full policy early: Declarations pages are not enough.

Preserve every communication: adjuster emails, letters, claim notes (if available), and denial explanations.

Match facts to statutory duties: General complaints carry less force than documented violations.

Use experts when the file calls for it: In technical cases, expert analysis can give the judge or jury a real standard to apply.

What usually does not work is threatening a lawsuit before the groundwork is done. Insurers see that every day. What changes outcomes is a file that shows the company had the facts, had the chance to act properly, and chose not to.

Building a Winning Case: What Evidence You Need

Insurance cases are won in the file before they are won in the courtroom. If the paperwork is thin, the insurer controls the story. If the record is organized and complete, the pressure shifts.

The core documents

Start with the documents that many individuals assume they already have. Often, they do not have all of them.

You want:

The complete insurance policy: Not just the declarations page. Endorsements, exclusions, conditions, and definitions matter.

Every communication with the insurer: Emails, letters, text messages, portal screenshots, denial notices, and claim requests.

Medical records and bills: These connect the injury to the event and show the scope of treatment.

Crash or incident reports: Police reports, incident reports, and witness information give the timeline structure.

Photos and video: Vehicle damage, visible injuries, the scene, roadway conditions, floor hazards, surveillance requests, and property damage.

If you are still gathering the basics, this guide on documenting the evidence needed for a personal injury claim in Florida is a useful starting point.

Why details beat arguments

Insurers often deny or discount claims by attacking one of a few predictable weak points:

they say the injury was preexisting

they argue that treatment was delayed

they claim the damage was minor

they insist the records do not support the symptoms

they point to missing proof and call the file incomplete

Documentation answers each of those points better than emotion does.

A timeline helps. So does consistency. If the records, photos, billing, treatment notes, and communications all fit together, the insurer has less room to recast the facts.

Keep your own claim log. Write down the date, time, name of the adjuster, what was requested, and what was said. Small inconsistencies in the insurer’s position often become major issues later.

When experts change the case

Some cases can be proved solely from records. Others need expert help.

That may include a treating physician, a specialist, an accident reconstruction expert, an engineer, or an insurance practices expert, depending on the dispute. The point is not to add cost for the sake of adding cost. The point is to answer technical defenses with credible analysis.

The value of that approach is not theoretical. That case illustrates something clients do not always see at the beginning. A strong expert does not just add an opinion. The expert provides the judge or jury with a standard for determining whether the insurer’s conduct was reasonable.

What good evidence collection looks like

A disciplined file usually has these characteristics:

Chronology: The records tell the story in order.

Consistency: The medical complaints match the incident and later treatment.

Completeness: Missing documents are identified and requested early.

Technical support: If the insurer leans on specialized opinions, you are ready to answer them.

In a Florida insurance dispute, Caine Law is one option for investigating claim files, preparing for bad-faith issues, and litigating when settlement efforts fail. The primary point, whatever lawyer you choose, is to work with counsel who knows how insurers build their defenses and how to dismantle them with evidence instead of guesswork.

The Lawsuit Process From Filing to Verdict

Once the dispute reaches the lawsuit stage, the process becomes more structured than one might expect. It is not a constant courtroom battle. It is a sequence of deadlines, paper exchanges, strategy decisions, and pressure points.

It starts before the complaint

A lawsuit should begin only after the case is ready. That means the policy has been reviewed, the denial or underpayment position has been analyzed, the damages are documented, and any required pre-suit steps have been handled.

That early work matters because the complaint frames the case. A rushed filing can create pleading problems, omit a viable theory, or make it easier for the insurer to delay.

The major phases

Most insurance lawsuits move through some version of the following stages:

Stage | What happens |

Investigation | Your lawyer reviews the policy, claim history, damages, and legal theories |

Filing | A complaint is filed, and the insurer responds |

Discovery | Both sides exchange documents, written questions, and testimony |

Negotiation or mediation | The parties test settlement options with the benefit of a fuller record |

Trial | A judge or jury resolves disputed issues if a settlement does not occur |

For a broader look at timing expectations in injury litigation, this overview of how long car accident lawsuits take helps explain why some cases move quickly, and others do not.

Discovery is where insurers lose control of the narrative

Discovery is the formal evidence exchange. It is here that many claimants first see the difference between complaining about unfair treatment and proving it.

Your lawyer may request claim file materials, internal communications, adjuster notes, policy documents, and the basis for the insurer’s decision. The insurer will also request records from you. Depositions may follow.

This phase matters because people often learn that the denial letter was only the surface explanation. Discovery can reveal inconsistent positions, thin investigation, missing analysis, or a claims process that was far less careful than the insurer suggested.

Mediation and settlement pressure

A large number of cases resolve before trial. That usually happens after enough evidence has been exchanged for both sides to assess risk accurately.

Mediation can be productive when the insurer sees that the file is well prepared and that trial counsel is ready to proceed. Mediation is less productive when the plaintiff’s side is still guessing about damages or coverage.

Filing suit creates a stronger position only if the insurer believes you are prepared to finish the case.

Why timing still matters after filing

Even strong cases can be lost by missing a deadline. As noted earlier, policy language and state law can shorten the time to act. Once litigation starts, the court adds another layer of deadlines for pleadings, discovery, motions, expert disclosures, and trial preparation.

Clients do not need to manage those rules personally, but they do need to understand the practical lesson. If you think you may need to sue, do not wait until the clock is almost gone. Insurance companies track deadlines carefully. You should assume they know exactly when your position weakens.

When to Call an Attorney for Your Insurance Dispute

Many individuals wait too long. They try to be reasonable, stay patient, and hope the insurer will correct course. Sometimes that works. Often, it gives the company more time to shape the record.

The moments that should trigger a call

You do not need to call a lawyer only after a formal denial. In many cases, the warning signs start earlier.

Call an attorney when you see any of these:

A lowball offer: The number does not come close to matching your medical care, wage loss, or documented harm.

A request for a recorded statement: Sometimes this is routine. Sometimes it is an effort to lock you into phrasing that gets used against you later.

A sudden coverage excuse: The insurer points to policy language that does not seem to match what you bought.

Long silence: Weeks pass with no real movement and no meaningful explanation.

Shifting reasons: The company changes its story about why it has not paid.

Why early advice matters

One of the biggest practical problems in this area is uncertainty about timing. Many sources are vague about when to hire a lawyer, leaving injured claimants in uncertainty.

That tracks with real-world experience. Early legal advice can prevent avoidable mistakes such as incomplete statements, missed deadlines, weak document preservation, and poorly framed appeals or notices.

If you are dealing with a first-party dispute, a lawyer can identify whether the issue is a contract claim, a bad-faith setup, or both. If it is a third-party liability dispute, counsel can determine whether the problem is really the insurer, the evidence of fault, the medical proof, or the amount of available coverage.

What does not help

People often hurt their own position by doing one of these:

sending emotional emails instead of organized evidence

accepting partial explanations without requesting the policy basis

assuming the adjuster’s deadline controls the case

waiting until the insurer has boxed them into a bad factual record

A consultation is not overreacting. It is risk management. If you need help with a dispute over a denial, delay, underpayment, or bad faith issue, speak to us today.

The practical bottom line

If you are asking, "Can you sue an insurance company?" the odds are good that something already feels off. Trust that instinct, but verify it with a lawyer who knows what insurers do behind the scenes.

The best time to get legal advice is usually before the claim hardens against you. Not every case needs a lawsuit. Some need a better demand package. Some need expert support. Some need a CRN. Some need immediate litigation.

What matters is making that decision from a position of knowledge, not frustration.

If an insurance company denied your claim, delayed payment, or treated your injury case like a number instead of a real loss, talk to Caine Law. The firm handles insurance disputes for injured Floridians and can evaluate whether the insurer breached the policy, acted in bad faith, or both. In pain? Call Caine.