In Pain? Call Caine

Florida Personal Injury Protection (PIP) Guide 2026

5 Min read

By: Caine Law

Share

The crash is over, but your body has not caught up yet. Your hands are shaking. Your neck feels tight. Your phone is full of missed calls, and before the tow truck even leaves, a bigger problem starts forming in the background. Who pays for treatment, how fast do you need to act, and what happens if the pain gets worse tomorrow instead of today?

That is where Florida personal injury protection becomes important.

Most injured people think they just need to report the wreck and see a doctor when they can. That approach causes damage to claims. Florida’s PIP system helps quickly, but it also punishes delay, sloppy documentation, and the wrong medical pathway. Insurance companies know this. They do not need you to make a huge mistake. They only need you to miss one deadline, choose one unprepared provider, or give one inconsistent statement.

A serious Florida accident claim usually has two tracks. The first is your PIP claim. The second is everything PIP does not come close to covering. Knowing the difference is what protects both your treatment and your long-term recovery.

Your First Moments After a Florida Car Accident

A common Florida crash starts with something ordinary. You are stopped at a light, inching through traffic, or trying to get home before the rain gets worse. Then another driver hits you. At first, you may feel more angry than injured. That is normal. So is telling the officer, “I think I’m okay,” and waking up the next morning barely able to turn your head.

Those first hours matter because the record starts immediately. The crash report, the photos, the names of witnesses, and your first medical visit all affect what your insurer does next. If you are unsure where to begin, this guide on what to do when accidents happen and the legal steps that matter is a good place to start.

What people often get wrong

Many injured drivers make one of these mistakes:

They wait to see if the pain goes away. Delayed treatment creates problems with both medical recovery and insurance proof.

They focus only on car damage. A vehicle can look drivable while the person inside has a concussion, back injury, or worsening soft-tissue injury.

They assume the other driver’s insurance takes over right away. In Florida, your own coverage often covers immediate injury-related expenses first.

After a crash, act as if your future claim will be judged only by documents. If it is not written down, photographed, reported, or diagnosed, the insurer will try to minimize it.

PIP is supposed to be the first layer of protection during this chaotic period. It can help with medical bills and lost income quickly, but only if you move correctly from the start.

What is Florida Personal Injury Protection

Florida Personal Injury Protection, usually called PIP, is part of Florida’s no-fault auto insurance system. Think of it as accident coverage attached to your vehicle policy that pays certain injury-related losses first, without waiting for a final fault decision.

That is the point of the system. You do not begin by fighting over who caused the crash before starting treatment.

The legal foundation

Florida law requires this coverage. Under Florida Statute § 627.736, every owner of a four-or-more-wheeled vehicle must carry at least $10,000 in PIP coverage per person per accident, and that coverage pays 80% of reasonable medical expenses and 60% of lost wages, up to the policy limit.

Why Florida uses a no-fault model

The practical idea is simple. Smaller injury claims should not require a full liability fight just to get basic treatment paid. PIP provides injured people with a path to immediate benefits while larger fault issues are sorted out separately, if needed.

That does not mean PIP is broad or generous. It is limited, technical, and often misunderstood.

Who this coverage is designed to protect

PIP is not just for the named driver on the policy. It can also affect people involved in the crash in ways many drivers do not realize.

Typical situations include:

The policyholder was injured in a crash

Certain household relatives

Passengers in the insured vehicle

Pedestrians or cyclists struck by the insured vehicle

That wide reach is one reason PIP sits at the center of many Florida accident claims. It often becomes the first source of payment before any bodily injury case develops.

PIP is not your full injury claim. It is your first line of defense. It helps early, but it does not solve the whole problem in a serious accident.

Understanding that distinction prevents one of the biggest mistakes injured people make. They treat PIP as the end of the case when it is usually only the beginning.

Understanding Your PIP Coverage Scope and Limits

The phrase “I have PIP” sounds reassuring. The details are less reassuring once bills start arriving.

PIP does not hand you the full policy amount. It pays specific categories of loss, but only within strict limits.

What PIP can pay

Florida PIP generally covers:

Medical expenses. This includes reasonable and necessary treatment for accidents.

Lost wages. If the injury keeps you from working, PIP can reimburse part of that income loss.

Replacement services in some cases. These are basic services you cannot perform because of the injury, such as certain household tasks.

Death benefits. Funeral-related benefits may be available in a fatal accident claim.

The reimbursement formula is the part that many people do not expect. PIP pays 80% of reasonable medical expenses and 60% of lost wages, not the full amount. Those benefits are also subject to the policy ceiling already discussed.

Who may be covered under one policy?

Person potentially covered | How it commonly arises |

Policyholder | Injured while driving or otherwise involved in a covered accident |

Household relative | Injured in a covered auto-related event |

Passenger | Riding in the insured vehicle |

Pedestrian or cyclist | Struck by the insured vehicle |

This is why early insurance review matters. The available PIP path depends on who was involved, what vehicle was used, and whose policy applies first.

The practical limit is often lower than people expect

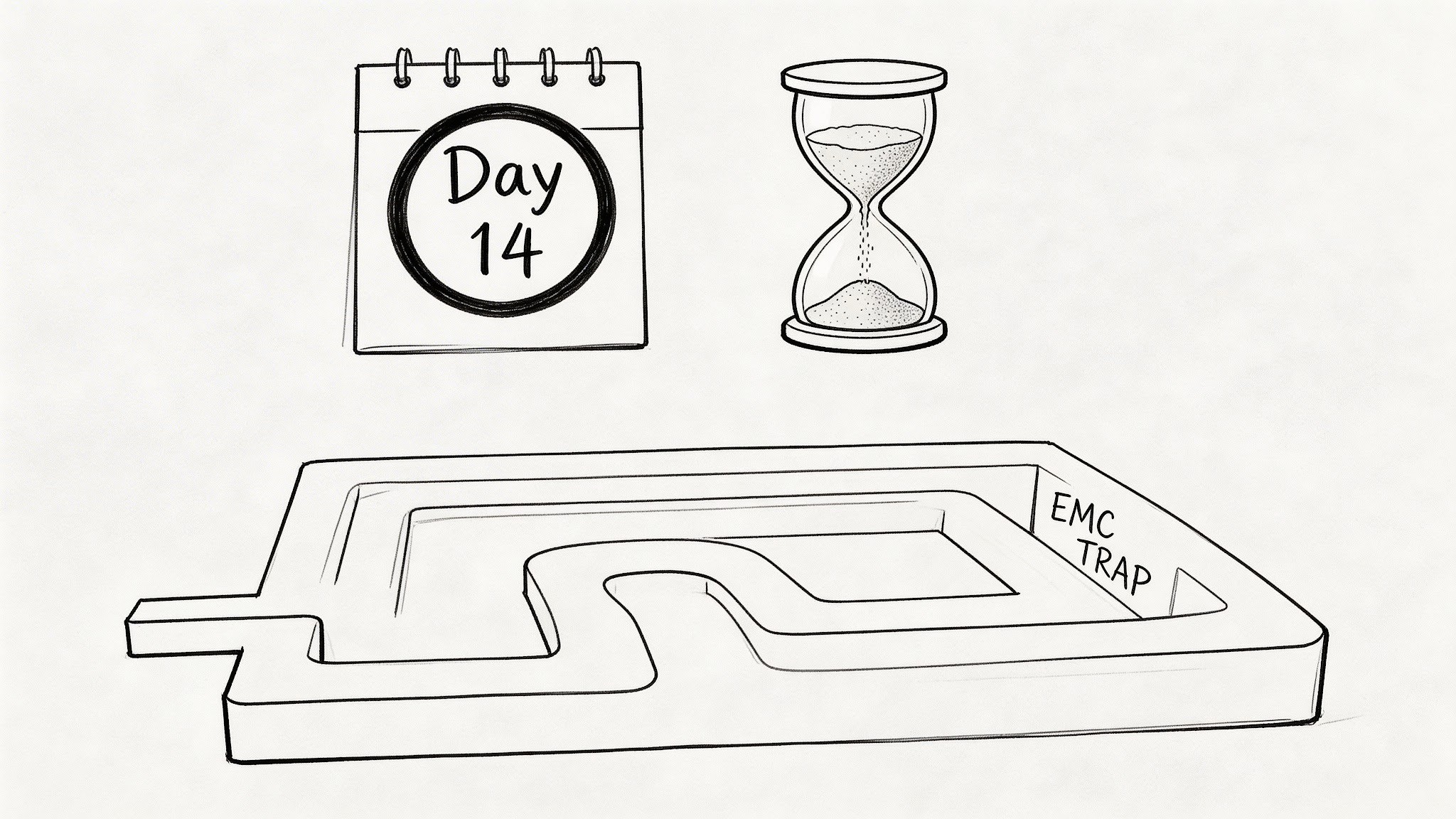

The biggest coverage shock comes from the medical qualification issue. Florida’s 14-day rule requires initial treatment within 14 days of the crash. If a provider diagnoses an emergency medical condition (EMC), you can access the full $10,000 in PIP benefits.

That lower cap is not theoretical. It can be devastating when treatment becomes expensive fast. Serious injuries requiring long-term treatment can exceed PIP limits quickly.

PIP Benefit Limits EMC vs. Non-EMC Diagnosis

Diagnosis Type | Maximum Medical Benefit Cap | Potential Coverage Reduction |

EMC diagnosis | $10,000 | None |

Non-EMC diagnosis | $2,500 | 75% reduction |

What this means in practice

A modest injury claim can quickly burn through available benefits. Once that happens, the unpaid balance does not disappear. It shifts to health insurance, out-of-pocket responsibility, provider balances, or a later injury claim against the at-fault driver.

PIP helps create access to treatment. It does not guarantee that treatment will be fully paid. Serious injuries outgrow PIP early.

That gap between what PIP pays and what recovery costs is where legal strategy becomes important.

The Critical 14-Day Rule and EMC Trap

Many people believe that if they see any doctor after a crash, they have protected their PIP rights. That is not enough.

Florida’s PIP system contains a gatekeeping rule that catches injured people at the worst possible time, when they are in pain, confused, and making rushed decisions.

Missing the deadline can wipe out benefits

Florida law generally requires treatment within 14 days of the accident. The more serious issue, though, is not just the deadline. It is the provider’s first determination.

If that provider does not document an emergency medical condition, your medical benefit may be limited to $2,500 instead of $10,000, a 75% reduction.

Why provider choice matters

Not every clinic approaches accident documentation the same way. Some providers are focused on treatment but do not document the claim issues carefully. Others understand that proper evaluation and charting affect benefit access from day one.

That does not mean anyone should chase paperwork instead of proper care. It means proper care includes competent documentation.

A better approach after a meaningful crash often includes:

Getting evaluated promptly. Waiting can lead to both medical and insurance complications.

Choosing a qualified provider who is prepared to assess crash injuries carefully.

Making sure your symptoms are fully reported. Severe pain, dizziness, radiating symptoms, headaches, numbness, and functional limits should be accurately described.

Keeping records from the start. Discharge papers, imaging referrals, work notes, and follow-up instructions all matter.

What does not work

Mistake | Why does it hurt the claim |

Waiting to “see how you feel.” | The insurer argues your injury was minor or unrelated |

Going somewhere that does not document well | The file may never support full benefit access |

Downplaying symptoms | Your own statements become evidence against you |

Skipping follow-up care | The insurer frames the injury as resolved |

The first medical visit after a Florida crash is not just treatment. It is the moment that often shapes the entire PIP claim.

Insurance companies understand this perfectly. If the initial record is weak, they gain an advantage before the claim begins. If the initial record is strong, they face a much harder fight.

How to File a Florida PIP Claim Step by Step

A PIP claim moves better when it is treated like a file you are building, not a phone call you made once.

The claim sequence that usually works best

Get medical attention first. Your health comes before paperwork, and your treatment record starts the claim.

Report the crash. Law enforcement documentation helps create an independent record of what happened.

Notify your insurer promptly. Give basic facts. Be accurate. Do not guess.

Collect the core documents. Police report, photos, witness details, medical records, work-loss information, and insurer forms all belong in one place.

Submit the PIP application and related paperwork. Many delays start here, with incomplete forms or missing signatures.

Continue treatment consistently. Gaps in care become insurer arguments.

Track every insurer contact. Save emails, letters, portal messages, and call notes.

A practical file-building method

A practical file-building method. Many individuals benefit from using a single folder, whether digital or physical, for the entire claim. Keep these items together:

Accident documents. Crash report, scene photos, vehicle photos.

Medical records. Initial evaluation, imaging orders, prescriptions, treatment notes.

Employment proof. Pay records, disability slips, and missed-work verification.

Insurance correspondence. Coverage letters, requests for information, payment logs, and denial notices.

Communication rules that protect you

When speaking with your insurer:

Stick to facts you know. If you do not know, say so.

Do not minimize symptoms. Casual phrases like “just sore” can be repeated later as admissions.

Confirm requests in writing when possible.

Review forms before signing. A rushed signature can create a long dispute.

If you are dealing with uncertainty after the crash, focus on timely care, organized records, and clear communication. Those basics carry more weight than people realize.

If the insurer asks for more records, dates, or provider details, respond carefully and keep proof of what you sent.

A PIP claim is often won or weakened in the paperwork phase. Strong facts and a clean record reduce the insurer’s room to maneuver.

Why Insurers Deny or Limit PIP Claims

A driver gets treatment, follows instructions, and assumes PIP will handle the bills. Then the insurer pays part of the claim, questions the rest, and says more records are needed before any additional benefits will be considered.

That pattern is common. PIP disputes usually do not start with a dramatic accusation of fraud. They start with friction that the carrier can turn into savings.

The insurer's underlying objective

The carrier knows PIP is limited from the start. It also knows many injured people need more care than PIP will pay for. That gap creates pressure. If the insurer can slow payments, question treatment, or cut off benefits early, it increases the chance that the injured person will give up, treat less, or settle the larger case too cheaply.

That is why a PIP fight is rarely just about one bill. It often shapes the value of the entire injury claim.

The pressure points insurers use

Post-2013 changes gave insurers stronger tools to challenge treatment, including the ability to request mental or physical examinations under § 627.736(7). In practice, carriers often use those tools the same way.

The usual arguments are familiar:

Medical necessity. The insurer says the care was excessive, too frequent, or no longer reasonable.

Causation. The adjuster points to prior complaints, degenerative findings, or any gap in treatment and argues the crash was not the cause.

Documentation problems. A vague chart, missing referral, inconsistent history, or incomplete provider note becomes the excuse for a broader denial.

Insurer examinations. The carrier sends you to a doctor it selected, then relies on that opinion to stop paying.

How these denials are built

Many denials are prepared long before the formal denial letter arrives. The file starts to move in the wrong direction when records fail to explain why the treatment was needed, how symptoms changed after the crash, or what limits the injury caused in daily life and work.

Insurers look for ordinary weaknesses because ordinary weaknesses are enough.

A patient who misses appointments may be labeled noncompliant. A provider who documents pain but not objective findings gives the insurer room to say the complaints are subjective. An exam doctor who spends little time with the patient can still produce a report that the carrier will use to cut off benefits.

Where an attorney changes the outcome

An experienced attorney handles PIP as an early contest over proof, timing, and pressure. The goal is not just to argue with the adjuster. The goal is to close off the easy reasons for denial, force the insurer to commit to its position, and turn a weak explanation into a dispute the carrier may have to defend.

That changes the conversation.

When the insurer knows the record is organized, the treatment course is medically supported, and the denial will be challenged through a formal insurance dispute claim process, its cost-benefit analysis changes. Some carriers still resist. But they lose the advantage they were counting on.

When PIP Is Not Enough to Cover Your Bodily Injury Claim

You leave the hospital, open the mail a week later, and realize ambulance charges, imaging, and follow-up care are already swallowing the $10,000 PIP policy you thought would protect you. Meanwhile, you are missing work, your pain is getting worse, and the insurer starts talking as if the case should wrap up quickly.

That is the gap that injured drivers in Florida run into every day.

PIP is short-term, no-fault coverage. A bodily injury claim is the part of the case that addresses what the crash cost you when the injuries are serious enough. That can include unpaid medical bills, full wage loss, future care, and the human damage PIP never touches, such as pain, physical limits, and loss of normal daily function.

Why does the case often start after the PIP runs thin

PIP helps at the front end. It does not come close to making many people whole after a significant crash.

The problem is not only the coverage cap. It is timing. PIP starts paying while the full extent of an injury is still developing. Insurance companies know that early records are often incomplete, people try to push through pain, and financial pressure makes a quick check look tempting. They use that window to frame the claim before the long-term picture is clear.

A proper bodily injury claim closes that gap with proof.

What has to be shown to recover beyond PIP

A bodily injury case is fault-based. That changes the fight.

Florida’s modified comparative negligence rule means your share of fault matters. If the defense can push your responsibility too high, it can reduce or block recovery. In practice, that means the at-fault driver’s insurer is not just reviewing medical bills. It is building arguments about how the crash happened, whether your injuries were caused by it, and whether your treatment was reasonable.

That is why these cases are won or lost on details that seem small early on.

How the defense tries to shrink the value of the claim

Once the claim moves outside PIP, the carrier usually shifts to familiar pressure points:

Minimizing the force of impact to argue that you could not be badly hurt

Blaming preexisting conditions for symptoms that became worse after the crash

Using treatment gaps to say you recovered sooner than you did

Pulling isolated statements from records or social media to question credibility

Pushing a quick settlement before future care needs are documented

None of that is accidental. The insurer is trying to keep your case inside the narrow PIP frame even when the law allows more.

How an attorney turns that pressure into settlement value

The answer is not louder demands. It is a file the insurer cannot dismiss cheaply.

That usually means preserving liability evidence before it disappears, organizing the medical timeline into a clean, consistent form, identifying what PIP paid and what remains unpaid, and presenting future losses in a way that makes sense to an adjuster, a defense lawyer, and, if necessary, a jury. It also means controlling the sequence. I do not want a client pushed into a low settlement while treatment is still revealing the full scope of the injury.

This is also where strategy matters. A weak BI claim lets the insurer argue, delay, and discount. A prepared one creates risk for the carrier. Risk changes offer.

If you want more context on how insurers value fault-based claims after a crash, this Florida auto accident settlement guide explains the bigger settlement picture.

A serious injury case is rarely about a single bill or denial. It is about proving the difference between what PIP covered and what the crash took from you. That difference is often where the largest part of the eventual recovery comes from.

Frequently Asked Questions About Florida PIP

Does PIP pay even if the other driver caused the crash

Yes. PIP is a no-fault benefit. Its basic purpose is to provide access to certain benefits without forcing you to prove fault first.

What happens if I wait too long to get treated

That can create severe problems for the claim. Florida’s system has a strict treatment deadline, and delay can destroy or sharply limit available benefits depending on how the medical record develops.

Will PIP pay all of my medical bills?

Usually not. PIP only pays part of covered medical expenses, and it has firm coverage limits. If injuries are substantial, unpaid balances often remain.

Does PIP cover lost wages?

Yes, but only in part. PIP can reimburse lost income within its statutory formula and overall policy restrictions, not full wage loss in every case.

Why did the insurer say I only qualify for limited medical benefits

This often happens because the initial provider did not document the medical finding required to unlock the higher-tier benefits. That first record can shape the rest of the claim.

Can I still bring a claim against the at-fault driver

In many serious cases, yes. That depends on your injuries, the available evidence, and whether you meet Florida’s comparative fault requirements for pursuing recovery beyond PIP.

Do I need to keep treating if I already opened the claim

If your doctor recommends continued care, follow that plan. Stopping and starting treatment gives insurers an opening to argue that your condition resolved or was never serious.

What if the insurer sends me to its doctor

Take the request seriously and get advice quickly. Insurer-requested exams are often used to support limiting or ending benefits, especially when the carrier wants a basis to challenge ongoing care.

Does PIP apply to every accident involving a vehicle

No. Coverage questions can become more complicated depending on the type of vehicle and how the injury happened. Those details should be reviewed carefully before making assumptions.

When should I speak with a lawyer?

Speak with a lawyer early if your injuries are worsening, your bills are mounting, your claim is being delayed, or the insurer is disputing treatment. Early action is often what prevents a PIP issue from becoming a larger compensation problem.

If you were hurt in a Florida crash and are struggling with medical bills, claim delays, or an insurer that is already pushing back, CAINE LAW can help you understand your options and protect the part of your case that Florida personal injury protection does not cover. Serious injuries require more than opening a claim and hoping the adjuster gets it right. In pain? Call Caine.