In Pain? Call Caine

Florida Auto Accident Settlement Guide

5 Min read

By: Caine Law

Share

When you've been in a car crash, a settlement isn't just about getting your car fixed. A true auto accident settlement is a financial agreement that's meant to cover all your losses from the mountain of medical bills and lost paychecks to the very real physical pain and emotional trauma the wreck has put you through.

Understanding How a Settlement Is Calculated

There’s no magic formula or online calculator that can spit out the exact value of your case. Instead, figuring out a fair settlement is more like building a house, piece by piece. You start with the solid foundation of your tangible, out-of-pocket costs, and then you build on top of that with the less obvious, but equally crucial, elements of your personal suffering.

The calculation rests on two main types of damages: economic and non-economic. Getting a handle on both is the first step to understanding what your claim is actually worth.

The Two Pillars of Your Settlement

As you can see, a final settlement is built from both concrete financial losses (economic damages) and fair compensation for human suffering (non-economic damages). But non-economic damages aren’t determined by one universal formula. Insurance companies may use shortcuts to suggest a value, while an attorney’s job is to prove the real impact on your life using medical evidence, credibility, and case-specific facts.

The Multiplier Method Explained

So how do you assign a dollar value to something like pain and suffering? There isn’t a single formula that decides it. In practice, insurance companies often use internal formulas (including “multiplier-style” math) to start negotiations, not to determine what’s fair.

Here’s the key point: Non-economic damages should reflect the human impact of the injury pain, limitation, disruption, trauma, and loss of enjoyment of life, not just the size of the medical bills.

Some cases prove exactly why “medical bills × a number” can be wildly misleading. In a fatal crash, for example, economic damages may be relatively limited (like funeral expenses), but the non-economic losses for surviving family members can be profound. Florida law recognizes that survivors may seek damages tied to mental pain and suffering and loss of companionship/protection in wrongful death cases

Common ways non-economic damages are supported (UPDATED)

Instead of relying on a simplistic formula, a strong claim typically builds non-economic damages using evidence like:

Treatment records showing duration, intensity, and setbacks

Statements from doctors about limitations and prognosis

A pain and function journal (sleep issues, mobility limits, missed life events, anxiety, etc.)

Before-and-after proof (work impact, family roles, hobbies, daily activities)

Comparable case outcomes (when available and relevant)

Insurers may use “multiplier” logic to minimize payouts. A trial-ready attorney uses real evidence to demand a number that matches the reality of what you’ve endured.

Typical Settlement Ranges for Florida Car Accident Injuries

It’s the question on everyone’s mind after a crash: “What is my case actually worth?” While there’s no magic number that fits every situation, we can look at typical settlement ranges for common injuries here in Florida. This gives you a crucial benchmark—a way to understand what’s at stake and why the specific details of your injury matter so much.

Think of it this way: the value of your settlement is tied directly to the severity of the harm you’ve suffered. A minor muscle sprain that heals in a few weeks just isn't going to have the same value as a broken bone that requires surgery and months of grueling physical therapy. It's all about accounting for the true impact on your life, from the mountain of medical bills to your ability to work and simply enjoy your day-to-day activities.

Minor to Moderate Injuries

These are the injuries that are incredibly painful and disruptive, but thankfully, don't usually result in a permanent or long-term disability. They often involve soft-tissue damage such as sprains and strains, which can be notoriously difficult to prove without diligent, consistent medical documentation.

Whiplash and Neck Strains: A classic injury from rear-end collisions. Settlements can range anywhere from $10,000 to $50,000, depending on how long your treatment lasts and the intensity of your pain.

Minor Sprains and Bruising: For crashes causing less severe soft tissue damage, settlements often fall in the $5,000 to $15,000 range. The final number really comes down to the cost of physical therapy and how much work you had to miss.

Settlement values here can swing wildly. Back and neck cases are a staple of car accident claims. While a minor case of whiplash might settle on the lower end, a claim that ends up needing surgery or leaves you with a permanent impairment can easily push into the six-figure range and beyond. This is exactly why meticulous medical records are your best defense against an insurance company trying to downplay your pain.

Serious and Life-Altering Injuries

When an accident causes significant, long-lasting, or even permanent damage, the potential settlement value skyrockets. These cases almost always involve extensive medical treatment, and they might keep you from ever returning to your old job. We’re talking about a lifetime of pain and limitations.

The goal here isn't just to pay off old bills. It's about providing financial security for a future that has been permanently changed by someone else's negligence. This is where the true value of a well-documented auto accident settlement really comes into focus.

A settlement for a catastrophic injury must account for a lifetime of care. This includes future surgeries, in-home assistance, medical equipment, and compensation for a permanent loss of earning capacity.

For example, an injury that requires a spinal fusion surgery will result in a substantially higher settlement than a simple herniated disc. Why? Because the surgery itself is invasive and expensive, and it brings with it a long, painful recovery and the potential for lifelong complications.

Catastrophic Injuries

In the most tragic cases, the injuries are so severe they change a person’s life forever. These settlements are the highest because they have to compensate for the most profound losses a person can endure.

Traumatic Brain Injuries (TBI): Even a "mild" TBI (like a concussion) might settle for $75,000 to $150,000. But a severe TBI that causes lasting cognitive impairment can lead to settlements of $1 million or more.

Spinal Cord Injuries: Cases that result in paralysis (paraplegia or quadriplegia) almost always result in multi-million dollar settlements. This money is needed to cover lifelong medical care, home modifications, and the loss of all future income.

Severe Burns or Amputations: These injuries involve unimaginable physical pain, permanent disfigurement, and deep psychological trauma. As a result, settlements frequently reach into the seven figures.

Looking at these ranges is a good starting point, but they are by no means a guarantee. For a clearer picture of what your specific case might be worth, check out our guide on the average settlement for a car accident in Florida. The only way to know the true potential of your claim is to have it evaluated by an experienced professional. In pain? Call Caine.

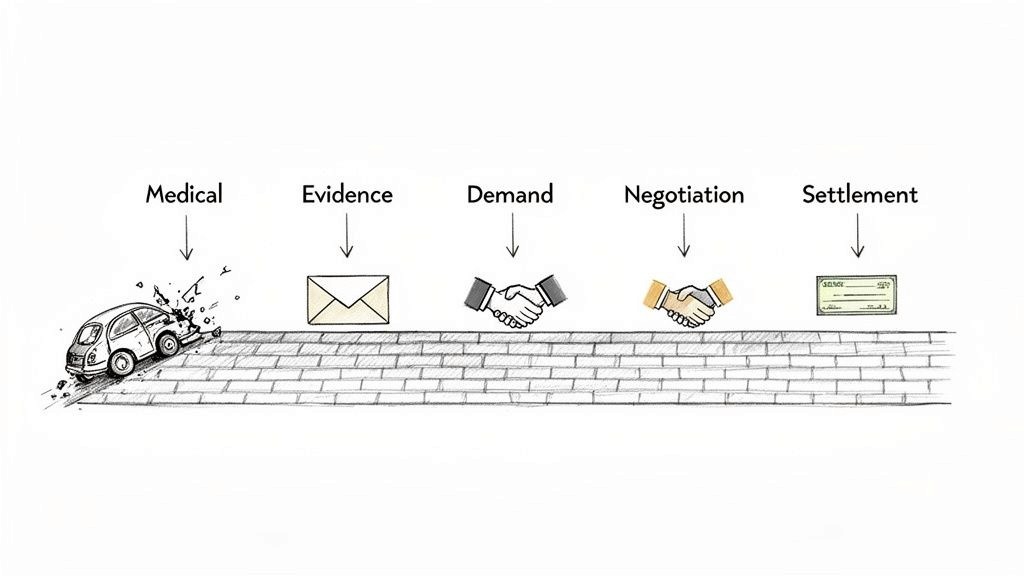

The Settlement Timeline: From Crash to Compensation

If you’ve been in a car accident, the journey to a settlement can feel like a long, winding road with no map. It’s natural to wonder, "How long is this going to take?" Understanding the typical timeline helps you set realistic expectations and takes some of the stress out of the unknown.

Think of it like building a house. You can't put the roof on before the foundation is poured and the walls are framed. Each stage has to be completed carefully and in the right order to make sure the final result is solid. A rushed settlement is like a poorly built house—it might look okay at first, but it will likely fall short in the long run.

While every case has its own unique twists and turns, the path from the crash to the final check generally follows a predictable pattern. Patience is your best ally here. Cutting corners just to get it over with almost always means leaving money on the table that you’re entitled to.

Phase 1: Initial Treatment and Investigation

The clock starts ticking the moment the accident happens. Your absolute first priority is getting medical attention. This not only starts your physical recovery but also creates the official medical records that link your injuries directly to the crash.

At the same time, the investigation gets underway. We start gathering all the crucial evidence: police reports, witness interviews, photos of the wreck and the scene, and damage estimates. The goal is to build a rock-solid case that clearly shows who was at fault. This foundational work can take anywhere from a few weeks to a few months, depending on how complex the accident was.

Phase 2: Reaching Maximum Medical Improvement

Here’s a hard truth: you can't know what your claim is truly worth until you know the full extent of your injuries. That’s why this next phase is all about your medical recovery. You'll need to follow through with all your prescribed treatments, whether that's physical therapy, seeing specialists, or undergoing surgery.

This continues until you reach what we call Maximum Medical Improvement (MMI). This is a huge milestone. It’s the point where your doctor says your condition has stabilized as much as it's going to. From here, they can give a clear picture of your long-term prognosis, including any permanent disabilities or future medical care you might need. Getting to MMI can take a few months for simpler injuries or well over a year for more serious ones.

Phase 3: The Demand and Negotiation Stage

Once all your damages are tallied up, your attorney puts together a comprehensive demand package. This is a formal, detailed document sent to the at-fault driver's insurance company. It lays out the facts, summarizes your injuries and treatment, lists every single financial loss, and makes a specific monetary demand for your settlement.

The insurance adjuster will then review everything and come back with a counteroffer. Be prepared because it’s almost always a lowball number. This is where the real negotiation begins. It’s a back-and-forth process where your lawyer fights on your behalf, using the evidence we’ve gathered to push for a fair amount. This stage can easily last for several months.

Phase 4: Finalizing the Settlement

When negotiations finally lead to a number both sides can agree on, you’ll sign a final settlement agreement. This is a legally binding contract. In exchange for the payment, you agree to release the at-fault party from all future claims related to the accident. Once the ink is dry, it usually takes a few weeks to get the settlement check in hand.

The whole process demands patience. In 2025, the average car accident case takes anywhere from 12 to 36 months to settle. A simple rear-end collision might wrap up in 12-24 months, while a truly straightforward claim might be done in 6-12 months.

Ultimately, a case that’s built carefully, even if it takes longer, nearly always results in a much fairer financial outcome. If you’re trying to recover from an accident, you need a team that knows this timeline inside and out. In pain? Call Caine.

How Insurance Companies Try to Reduce Your Payout

After a car crash, it’s easy to think the other driver's insurance company is there to help you. The reality is, their job is to protect their own profits. Every dollar they pay you in a settlement is a dollar out of their pocket, so their adjusters are highly trained in one thing: minimizing your auto accident settlement.

Think of it as a playbook. They've seen thousands of claims just like yours, and they have a set of go-to tactics designed to chip away at the value of your case. Knowing their game plan is your best defense.

The Quick and Low Settlement Offer

Don't be surprised if you get a call from an adjuster just days after the accident. They’ll sound incredibly sympathetic and concerned, and then they'll slide a settlement offer across the table, a quick check to "take care of things." This is a classic trap.

They are counting on your stress. You're in pain, the medical bills are starting to pile up, and you just want this whole ordeal to be over. They want you to grab that check before you’ve even had a chance to figure out how serious your injuries truly are.

Accepting an early settlement is a final decision. Once you take the check, you sign away your right to seek any further compensation, even if you later discover your injuries require surgery or long-term care.

This move is so effective because many common car accident injuries, like a herniated disc or whiplash, can take weeks or even months to show their full impact. The insurance company knows this. They're betting you don't.

Using Your Own Words Against You

Ever hear the phrase, "This call may be recorded for quality and training purposes"? When it comes from an insurance adjuster, see it as a giant red flag. They will almost always ask for a recorded statement about the accident, and it’s not to help you.

Adjusters are masters of asking tricky questions that sound innocent on the surface. For example:

"How are you feeling today?" If you give a polite, automatic response like "I'm fine," they’ll jot it down as an admission that you're not really hurt.

"What were you doing right before the crash?" They’re fishing for any detail they can twist to argue you were distracted and partially to blame.

"Are you sure you weren't going a little over the speed limit?" This question is designed purely to make you doubt yourself and admit to some level of fault.

Here’s the bottom line: You are not legally required to give a recorded statement to the at-fault driver’s insurance company. The best thing to do is politely decline and tell them your attorney will handle all future communication.

Questioning Your Medical Treatment

Another favorite tactic is to attack your medical care. The insurance company will comb through every single doctor's note and medical bill, looking for excuses to argue your treatment was either unnecessary or unrelated to the crash.

They might claim you waited too long to see a doctor, which "proves" your injuries weren't that bad. Or they’ll argue that the physical therapy you needed was excessive. Sometimes, they’ll even dig into your past medical records to blame your pain on a pre-existing condition. It's a calculated strategy to reduce the value of your medical damages, which in turn drives down their settlement offer.

Protecting your right to a fair auto accident settlement means being ready for these games. The adjuster isn't your friend—they are a skilled negotiator working for a massive corporation. It’s time to level the playing field.

Get in touch with us at 786-206-8726 to arrange your complimentary consultation and access the legal assistance you need.

Actionable Steps to Maximize Your Settlement

Document Everything Meticulously

Evidence is the bedrock of any successful injury claim. Your memory will fade over time, but photos, videos, and written records are permanent proof.

If you are physically able to, start gathering information at the scene. Take pictures and videos of everything: the damage to all vehicles, their final positions, skid marks, broken glass, and any relevant road signs or traffic signals. Swap insurance and contact info with the other driver, and just as importantly, get the names and phone numbers of anyone who saw what happened.

A detailed record is your best defense against an insurer's attempts to downplay your losses. Keep a simple folder or notebook where you log every accident-related expense, medical appointment, and conversation about your claim.

This simple act of documentation creates a clear, undeniable timeline of your experience and losses, making it much harder for an adjuster to poke holes in your story.

Seek Immediate Medical Attention

Your health always comes first. But getting prompt medical care also serves a critical legal purpose. Even if you feel okay right after the wreck, adrenaline is a powerful painkiller that can mask serious injuries like whiplash, a concussion, or even internal bleeding.

Get checked out as soon as possible, whether at an urgent care clinic or the emergency room. This visit creates an official medical record that directly links your injuries to the crash. A delay of even a few days gives the insurance company an opening to argue your injuries happened somewhere else or aren't as severe as you claim. Follow your doctor’s orders to the letter—attend every appointment and fill every prescription.

Protect Your Claim From Common Pitfalls

We live our lives online, but after an accident, a few careless clicks can seriously damage your case. You have to assume the insurance company’s investigators are looking for anything they can twist and use against you.

To protect yourself, follow these simple rules:

Stay Off Social Media: Don't post anything about the accident, your injuries, or your recovery. A single photo of you smiling at a family BBQ can be used to argue you aren't really hurt.

Do Not Give a Recorded Statement: You are under no legal obligation to give a recorded statement to the at-fault driver’s insurer. They are trained to ask leading questions to trap you. Politely decline and tell them to speak with your attorney.

Keep Detailed Financial Records: Save every single receipt and bill related to the accident. This includes everything from medical co-pays and prescription costs to mileage driving to and from the doctor.

Considering installing a dash cam can also provide undeniable proof of what happened, completely shutting down any debate over fault.

The bottom line is that every piece of evidence matters. And the final, most important step is knowing when it's time to bring in a professional to fight for you. An experienced attorney can handle the complexities of your claim and shield you from the insurance company's tactics. In pain? Call Caine.

Post-Accident Action Checklist

Right after an accident, it’s easy to feel overwhelmed. This checklist breaks down the essential steps to protect both your health and your potential settlement claim. Following these actions methodically can make a significant difference in the outcome.

Action Item | Why It's Critical for Your Settlement | When to Do It |

Ensure Safety | Your well-being is the top priority. It also shows you acted responsibly. | Immediately |

Call 911 | Creates an official police report, a key piece of evidence for establishing fault. | Immediately |

Document the Scene | Photos/videos capture unbiased evidence before it's cleaned up or forgotten. | At the Scene |

Gather Witness Info | Third-party accounts are powerful for corroborating your version of events. | At the Scene |

Seek Medical Care | Officially links your injuries to the crash and starts your recovery journey. | Within 24 Hours |

Report to Your Insurer | Fulfills your policy obligations, but stick to the basic facts. | Within 24-48 Hours |

Start a Claim Journal | Tracks pain levels, medical visits, expenses, and missed work—all compensable. | As Soon as Possible |

Decline a Recorded Statement | Prevents you from being tricked into saying something that hurts your claim. | Always |

Stay off Social Media | Avoids giving the opposing insurer ammunition to devalue your injuries. | For the Duration of Your Claim |

Consult an Attorney | Provides expert guidance and protects you from aggressive insurance tactics. | Before Talking to Adjusters |

Taking these steps helps build a strong foundation for your claim, ensuring you have the documentation and medical proof needed to pursue the compensation you deserve.

Common Questions About Florida Auto Accident Settlements

Do I Have to Pay Taxes on My Auto Accident Settlement in Florida?

This is one of the first things people ask, and the answer is usually good news. For the most part, the portion of your settlement that pays you back for physical injuries and medical bills is not considered taxable income by the IRS. The same goes for money to repair your car or other damaged property.

But there are a couple of important exceptions you need to know about.

Lost Wages: Any money you receive specifically for lost income is typically taxable. The IRS looks at it this way: you would have paid taxes on that money if you'd earned it at work, so you have to pay taxes on it now.

Punitive Damages: On the rare occasion that a case involves punitive damages (meant to punish the at-fault party for truly reckless behavior), that money is almost always taxable.

Emotional Distress: Compensation for emotional distress can sometimes be taxed if it isn't directly tied to a physical injury.

Tax laws can get complicated fast. It’s always a smart move to talk through the specifics of your settlement with your attorney and a qualified tax professional to make sure you're handling everything by the book.

What Happens If the At-Fault Driver Is Uninsured?

It's a driver's worst nightmare: you're hurt in a crash, and the person who caused it doesn't have insurance. Sadly, it happens all the time in Florida. When it does, your main option for getting compensation is through your own insurance policy, specifically, your Uninsured/Underinsured Motorist (UM/UIM) coverage.

This is optional coverage in Florida, but it is hands-down one of the most important protections you can have. It's designed to cover your medical bills, lost wages, and pain and suffering when the at-fault driver can't. Without UM/UIM coverage, your choices are very limited. You could sue the driver personally, but actually collecting any money is next to impossible if they don't have significant assets. A good attorney will explore every single possibility to find a source of recovery for you.

How Does Florida's No-Fault Law Affect My Settlement?

Florida is a "no-fault" state, which adds a unique twist to the whole process. The no-fault system means your own insurance is the first place you turn for immediate expenses, no matter who was responsible for the accident.

Your Personal Injury Protection (PIP) coverage is required to pay for:

80% of your initial medical bills.

60% of your lost wages.

This coverage maxes out at $10,000. Your auto accident settlement is for everything that goes beyond what your PIP covers. This includes the other 20% of medical bills, the remaining 40% of lost wages, any future medical care, and all of your non-economic damages like pain and suffering, which PIP doesn't cover at all. Your lawyer’s job is to carefully track all of this to make sure every last dollar you've lost is included in your settlement demand to the at-fault driver's insurance.

Trying to figure out a settlement on your own can be tough, but you don't have to go it alone. The legal team at CAINE LAW has the experience to answer your questions and fight for the full compensation you deserve.

Experiencing pain? Reach out to Caine. Call us at 786-206-8726 to arrange a complimentary consultation and obtain the legal assistance you need.