In Pain? Call Caine

What is stacked uninsured motorist coverage? A Practical Guide

5 Min read

By: Caine Law

Share

Let’s talk about one of the most powerful, and often misunderstood, parts of your car insurance policy: stacked uninsured motorist (UM) coverage. Think of it as a way to seriously multiply your financial protection if you get hit by a driver who has little or no insurance.

Instead of just one layer of coverage, stacking lets you combine the UM limits from every vehicle on your policy. This creates a much bigger safety net for your medical bills, lost wages, and other damages—a critical choice for anyone driving in Florida.

Your Financial Shield Against Uninsured Drivers

When another driver causes a crash, you’d normally file a claim against their insurance to cover your losses. It sounds simple enough. But what if they don't have insurance? Or what if their cheap, bare-bones policy can't even begin to cover the cost of your serious injuries?

That’s exactly when your own uninsured motorist (UM) coverage is supposed to kick in and save the day.

Stacked UM coverage takes that protection to a whole new level. Imagine your non-stacked policy is a single shield, its strength limited to the coverage amount on just one car. If you choose to stack, you get to weld together the shields from every single vehicle on your policy. The result is a much stronger, multi-layered defense against financial ruin.

Why Stacking Is So Important in Florida

This isn't just some minor insurance detail; it's a huge financial decision, especially here in Florida. We have a massive problem with uninsured drivers.

While the national average for uninsured drivers hovers around 12.6%, Florida's rate is downright alarming. At times, nearly 1 in 4 drivers on our roads are cruising around without any insurance at all. This puts every responsible, insured driver at serious financial risk every single time they get behind the wheel.

That statistic is staggering, and it highlights a dangerous reality on Florida's roads. When one of those drivers hits you, their lack of insurance instantly becomes your problem. Without enough protection on your end, you could be left holding the bag for devastating medical debt and lost income. You can learn more about Florida's uninsured motorist statistics and see how they compare nationally.

This is where stacked coverage proves its worth. By letting you combine your UM limits, it creates a much larger pool of money to draw from after a crash. It ensures you have what you need to actually recover without having to drain your life savings or sell your home.

Stacking transforms your auto insurance from a simple legal requirement into a robust financial safeguard for you and your family.

If you’ve been hurt by an uninsured driver and are fighting to make sense of your own policy, don't try to take on the insurance company by yourself. An experienced attorney can cut through the confusion and fight for the full compensation you deserve. In pain? Call Caine.

How Stacking Your Coverage Actually Works

It’s one thing to hear the term "stacked uninsured motorist coverage," but it’s another thing entirely to see how it can multiply your financial protection when you really need it. Forget complex insurance jargon; think of it as simply building a stronger financial shield for yourself and your family. Stacking is a straightforward way to combine smaller coverage amounts into a much larger, more effective safety net after a crash.

The way it works is simpler than you might think. Stacking is designed to let you pull from different sources of coverage you're already paying for, making them work together to maximize your resources when you're hit by a driver who doesn't have enough insurance to cover your injuries.

The Two Main Types of Stacking

The most common method is what we call vertical stacking. Picture it like stacking bricks. You take the Uninsured Motorist (UM) coverage from each car insured under a single policy and pile them on top of each other. Every car you add to the policy adds another brick, building a taller, stronger wall of protection.

The second method is called horizontal stacking. This lets you link the UM coverage from separate insurance policies within your household. For example, if you and your spouse have separate car insurance policies, horizontal stacking could allow you to combine the UM limits from both.

These two methods—vertical stacking on one policy and horizontal stacking across different policies—are what make this coverage so powerful. For instance, if you insure two cars on one policy and have $25,000 in UM coverage for each, vertical stacking gives you a total of $50,000 for a single accident. A third car bumps that up to $75,000. You can find more examples of how stacking increases your policy limits on Bankrate.com.

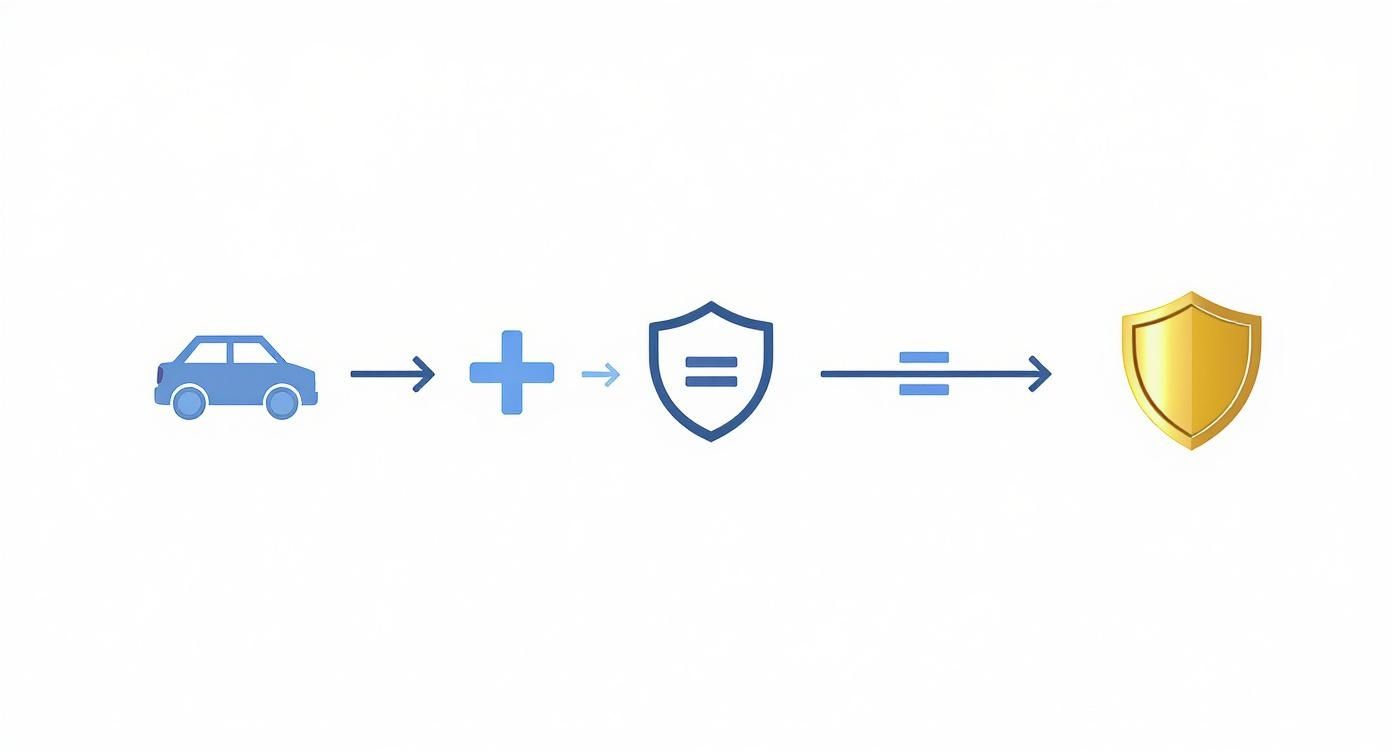

This graphic helps visualize how you can combine coverage from multiple vehicles to create a much stronger shield.

As you can see, it’s a simple addition problem: coverage from one car plus coverage from another equals a more substantial layer of protection when you need it most.

A Clear Example of Stacking in Action

Let's put some real numbers behind this to show you the difference it can make.

Imagine you’re a responsible Florida driver with three family cars on a single auto policy. You made the smart choice to include UM coverage with a $50,000 per person limit for each vehicle.

Vehicle 1: $50,000 in UM Coverage

Vehicle 2: $50,000 in UM Coverage

Vehicle 3: $50,000 in UM Coverage

With non-stacked coverage, if you're in an accident, you can only access the $50,000 limit tied to the specific car you were driving. That’s it. Your total protection is capped, no matter how many other cars you insure.

But with stacked coverage, you can combine the limits from all three of your vehicles. That means your total available coverage for a single wreck jumps from a mere $50,000 to a much more substantial $150,000 ($50,000 x 3).

This multiplication is a game-changer if you’re facing serious injuries. Remember, stacked UM coverage is specifically for bodily injuries. It’s there to help pay for your medical bills, lost wages, and pain and suffering—it doesn't cover repairs to your car.

After a crash, trying to decipher your own policy can feel overwhelming, and insurance companies aren't always quick to explain your right to stack coverage. An experienced attorney can cut through the confusion and make sure you understand the full extent of the benefits you've paid for. In pain? Call Caine.

The Real-World Financial Impact of Stacking

Theory is one thing, but seeing how stacked uninsured motorist coverage plays out in a real-life crisis is where its value truly hits home. Honestly, the choice between stacked and non-stacked coverage can be the single most critical financial decision you make to protect your family.

Let’s walk through two scenarios to show the staggering difference this one policy detail can make after a serious crash. These stories highlight how an abstract insurance term can mean the difference between weathering a storm and facing financial ruin.

Scenario One: The Financial Cliff with Non-Stacked Coverage

Meet Sarah, a nurse and mother of two who always pays her insurance premiums on time. Her policy covers three family vehicles, each with a $50,000 non-stacked Uninsured Motorist (UM) limit. One afternoon, a driver with no insurance blows through a red light and T-bones her minivan. The crash leaves her with severe injuries that require surgery and a long, painful road of rehabilitation.

Her medical bills quickly balloon past $150,000. But here's the problem: because her UM coverage is non-stacked, she can only access the $50,000 limit tied to the one car she was driving. That’s it. That’s her entire safety net.

Once her insurance pays out the $50,000 maximum, Sarah is stuck with the remaining $100,000 in medical debt. On top of that, she’s lost a huge chunk of income from being unable to work. Suing the at-fault driver is pointless—they have no assets to collect from. Now, she’s facing a mountain of debt, constant calls from collectors, and the crushing stress of a financial crisis while trying to recover physically.

Scenario Two: The Safety Net of Stacked Coverage

Now, let's look at David, a teacher who finds himself in the exact same horrible situation. He also insures three family cars and, just like Sarah, has a $50,000 UM limit on each. The key difference? He chose to pay a little extra for stacked coverage. When the same uninsured driver hits him, his injuries and medical bills also total $150,000.

This is where his story takes a completely different turn. Because David’s policy is stacked, he can combine the UM limits from all three of his vehicles.

Vehicle 1: $50,000 UM Limit

Vehicle 2: $50,000 UM Limit

Vehicle 3: $50,000 UM Limit

Total Available Coverage: $150,000

David’s stacked policy creates a $150,000 pool of coverage, which is enough to cover all of his medical bills. It also provides a crucial buffer to help make up for his lost wages and compensate him for the immense pain and suffering he’s been through. He can focus entirely on getting better, free from the terror of financial collapse.

A Head-to-Head Financial Comparison

The difference in these outcomes is night and day. A simple choice made when setting up the policy became the single factor that separated financial security from disaster.

By choosing to stack, a driver transforms their coverage from a simple, single-vehicle limit into a powerful, combined asset that can fully protect them in a worst-case scenario. This turns multiple small policies into one large shield.

The table below breaks down the numbers, highlighting just how massive the financial gap can be.

Financial Outcome Comparison After a Serious Accident

Financial Item | Non-Stacked Policy ($50k UM Limit) | Stacked Policy (3 Vehicles, $50k UM Limit each) |

|---|---|---|

Total Medical Bills | $150,000 | $150,000 |

Maximum UM Payout | $50,000 | $150,000 |

Out-of-Pocket Debt | $100,000 | $0 |

Coverage for Lost Wages | Potentially none | Available within the limit |

Financial Outcome | Overwhelming debt | Full financial recovery |

As you can see, the impact isn't just about numbers on a page; it’s about peace of mind, stability, and the ability to heal without facing a second crisis.

Unfortunately, insurance companies don't always volunteer this information or make the claims process easy. If you are struggling to get the compensation you're owed after an accident, professional legal help can make all the difference. In pain? Call Caine.

Is Stacked Coverage Worth the Extra Cost?

It’s the question every responsible driver asks when looking at their policy: is this extra coverage really worth the money?

When it comes to stacked uninsured motorist coverage, the answer is surprisingly clear. While adding any feature to your insurance policy will bump up your premium, the price for stacking is often far less than people assume—especially when you weigh it against the catastrophic financial risk it helps you avoid.

This isn't about adding a luxury feature; it’s about making a smart investment in your family's financial security. The slightly higher premium is a predictable, manageable expense. On the flip side, the medical bills and lost wages from a serious crash caused by an uninsured driver are unpredictable, uncontrollable, and potentially ruinous.

Breaking Down the Numbers

So, how much more are we really talking about? While every driver's premium is unique, some research gives us a helpful benchmark.

Opting for stacked uninsured motorist protection adds approximately $36 per month to an average insurance premium. That number can shift based on your driving record, where you live, and how many cars you insure. For some drivers, though, stacked coverage can cost as little as $20 per year—less than what many people spend on coffee in a week. You can find more details on the costs of stacked vs unstacked insurance on dontgethittwice.com.

As a general rule, you can expect stacked coverage to cost about 20-30% more than a standard unstacked policy. That might sound like a lot, but remember, this increase only applies to the UM portion of your bill, which is usually just a small fraction of your total insurance cost.

An Investment in Peace of Mind

Think of the small, added cost of stacking as buying yourself an enormous amount of peace of mind. For just a few extra dollars each month, you're putting a powerful safeguard in place for a worst-case scenario.

The real value of stacked coverage becomes crystal clear when you need it most. It transforms a modest policy limit into a substantial safety net capable of covering severe injuries, extensive medical treatments, and long-term income loss—protecting your savings, your home, and your family’s future.

In a state like Florida, where your risk of running into an uninsured driver is exceptionally high, this isn't a gamble—it's a calculated decision. Paying a little more now prevents you from having to pay an unbearable price later.

If you're grappling with the aftermath of a collision, understanding what your coverage can actually do for you is crucial. Navigating the complexities of stacked claims can be a real challenge, especially when you're also trying to heal from your injuries. Learning more about your options after auto and motorcycle accidents is a vital step toward protecting your rights and getting the compensation you're owed.

When you weigh the small monthly cost against the potential for six-figure medical debt, the choice becomes obvious. Stacked uninsured motorist coverage isn't just another line item on your bill; it’s one of the smartest, highest-return investments you can make for your financial well-being. If you're facing this difficult situation and the insurance company is giving you the runaround, getting expert legal help is essential. In pain? Call Caine.

How to Navigate a Stacked UM Insurance Claim

Having stacked uninsured motorist coverage is a great start, but what really matters is knowing how to use it when you're hurt. After a collision with an uninsured or underinsured driver, getting the compensation you deserve can be a surprisingly tough road. This section is your practical guide to the claims process, designed to help you take the right steps and access the full benefits you've been paying for.

The minutes, hours, and days after a crash are absolutely critical. Every action you take—or don't take—can swing the outcome of your claim. Your insurance company will be looking for very specific evidence, and the best way to protect yourself is to build a clear, well-supported claim from day one.

Your First Steps in the Claims Process

Right after an accident, your top priority is your health and safety. Period. But once the initial shock wears off, you need to shift gears and start documenting everything. Think of it as building your case, piece by piece. Meticulous record-keeping is your single most powerful tool.

Start gathering key information at the scene if you're able to. From that point on, your job is to keep a running log of your medical treatment and recovery.

Here are the essential actions you need to take:

Report the Wreck and See a Doctor: Always call the police. An official accident report is a vital piece of evidence you can’t get later. Just as important, get checked out by a doctor right away, even if you think you’re fine. Many serious injuries don’t show symptoms for hours or days, and a medical record creates an undeniable link between the crash and your injuries.

Document Absolutely Everything: Pull out your phone. Take tons of photos and videos of the accident scene, the damage to all vehicles, the road conditions, and any visible injuries you have. Get the names and numbers of anyone who saw what happened. Start a journal to track your pain levels, every doctor's appointment, and all the ways the injuries are messing up your daily life.

Notify Your Insurer Immediately: Call your own insurance company as soon as you can. When you speak to them, tell them clearly that you are opening an Uninsured Motorist claim and that you plan to stack your coverage. Getting this on record is a crucial step in the process.

Common Tactics Insurers Use to Deny or Reduce Claims

You’d think your own insurance company would be on your side, but don't count on it. Insurers are businesses, and their primary goal is to pay out as little as possible. Knowing their playbook can help you stay a step ahead.

Insurance companies have entire departments dedicated to picking claims apart. They’ll use your policy's confusing language against you, question how bad your injuries really are, or throw a lowball offer at you, hoping you’re desperate enough to take it.

They might try to argue your injuries were from a pre-existing condition or that you waited too long to see a doctor. Another classic move is to dispute the fine print in your policy, claiming your specific situation doesn't qualify for stacking. This is exactly why your detailed documentation is so critical—it's the proof you need to shut down their arguments. For anyone hitting these roadblocks, understanding the tactics used in insurance disputes can give you a major advantage.

When to Bring in a Personal Injury Lawyer

You might be thinking, "Can't I just handle this myself?" For a minor fender-bender, maybe. But the second your claim gets complicated or the insurance adjuster starts giving you the runaround, it’s time to call a lawyer.

You should seriously consider hiring an attorney if you run into any of these situations:

Serious Injuries: If you need surgery, face a long road of physical therapy, or might have a long-term disability, the financial stakes are simply too high to handle this alone.

Insurer Delays or Denials: Is the insurance company ghosting you? Not returning calls? Or have they flat-out denied your right to stack your coverage? You need an advocate in your corner, now.

Low Settlement Offers: The first offer is almost never the best one. An experienced attorney knows how to calculate the true value of your claim—including all medical bills, lost income, and pain and suffering—and has the skill to negotiate a fair settlement.

Complex Policy Language: If you’re getting lost in the jargon and the insurer is using your confusion to their advantage, a lawyer can cut through the noise and defend your rights.

Successfully navigating a stacked UM claim takes diligence, clear communication, and often, professional legal muscle. A good lawyer doesn't just help; they level the playing field, making sure the insurance company treats you fairly and pays the full amount you are owed under your policy.

If you're hurt and facing a fight with your insurer, you don't have to do it by yourself. In pain? Call Caine.

What To Do After an Uninsured Motorist Wreck

After a crash with an uninsured driver, the choices you make in the hours and days that follow can make or break your physical and financial recovery. Knowing what stacked uninsured motorist coverage is is the first part of the puzzle; knowing what to do with that knowledge is the second. Your absolute priority is to protect your health and lay the groundwork for a solid claim.

If you're ever in this incredibly stressful situation, zero in on these immediate, practical steps. They're designed to safeguard your well-being and your legal rights right from the start.

Your Post-Accident Checklist

Taking calm, deliberate action is your best defense. Here’s a straightforward checklist to guide you through those first critical moments.

See a Doctor. Period. Your top priority is medical care. Get checked out right away, even if you think you’re fine. Adrenaline is a powerful painkiller that can mask serious injuries, and a documented medical visit is crucial evidence for any claim.

Document Everything. Use your smartphone. Take photos of the accident scene from multiple angles, the damage to all vehicles, and any visible injuries. If there are witnesses, get their names and numbers. Jot down every detail you can remember about how the crash happened.

Call Your Insurer. Report the accident to your own insurance company as soon as you can. Be very clear that the other driver was uninsured and you need to open an uninsured motorist claim using your stacked benefits.

Find Your Policy. Pull up the declarations page of your auto insurance policy. You need to confirm your UM/UIM coverage limits and double-check that your coverage is, in fact, stacked.

For a deeper dive into handling the immediate aftermath of a crash, you can learn more about what to do when accidents happen in our essential guide.

Trying to handle a stacked UM claim on your own is like walking into a legal battle without a weapon. Insurance companies have entire legal teams dedicated to paying out as little as possible; you deserve to have a fierce advocate fighting just for you.

Don't go up against the insurance company by yourself. A free, no-obligation consultation can help you understand your rights and see the path forward. In pain? Call Caine.

A Few More Questions About Stacked Coverage

We've walked through the nuts and bolts of stacked uninsured motorist coverage, from how it works to what it costs. But it's totally normal to still have a few questions about how it all applies to your specific life and your family.

Let's clear up some of the most common questions we hear from drivers every day.

Can I Stack Coverage If I Only Own One Car?

In most cases, no. Stacking is built on the idea of combining the coverage from multiple vehicles you insure. If you only have a single car on your policy, you're working with a standard, non-stacked UM policy.

That said, there's a less common exception called "horizontal stacking." In some situations, you might be able to combine coverage from separate policies within your household, even if you only own one vehicle yourself. Whether this is an option really comes down to the fine print in your policy and what Florida law allows.

Does Stacked UM Cover Me as a Pedestrian or Cyclist?

Yes, it almost always does. This is easily one of the most valuable—and most overlooked—perks of stacked UM coverage. It’s designed to protect you, not just the car you happen to be driving.

Think of it this way: if you’re hurt by an uninsured or underinsured driver while you’re out for a walk, jogging, riding your bike, or even just catching a ride in a friend’s car, you can typically file a claim under your own stacked UM policy. It’s a layer of protection that travels with you, long after you’ve parked your car.

Do I Have to Reject Stacked Coverage in Writing in Florida?

Absolutely, yes. This is a big one. Florida law is written to protect you, the consumer, by making stacked coverage the default option. Your insurance company is legally required to offer it to you whenever you buy or renew your policy.

If you decide you want less protection—either by choosing a non-stacked policy or getting rid of UM coverage altogether—you have to make it official. You'll need to sign a specific form from your insurer to document your choice. This is a legal safeguard to make sure that giving up this important coverage is a conscious, deliberate decision, leaving no room for doubt later.

Dealing with the chaos after a car accident is hard enough. The last thing you need is a fight with an insurance company over the benefits you've been paying for. When claims get complicated, having an experienced legal advocate in your corner can make all the difference. In pain? Call Caine.

At CAINE LAW, we know how insurance companies think and operate. We’ll fight to get you the full and fair compensation you’re entitled to. If you're hurt and struggling after an accident, don't try to handle it alone. In pain? Call Caine. Contact us for a free consultation at https://cainelegal.com.