In Pain? Call Caine

What Is Insurance Bad Faith and How to Fight Back

5 Min read

By: Caine Law

Share

When you buy an insurance policy, you’re not just buying a piece of paper. You're buying a promise—a promise that if something goes wrong, the insurance company will be there to help you pick up the pieces. You hold up your end of the bargain by paying your premiums on time, every time.

But what happens when the company you trusted breaks that promise?

Understanding Insurance Bad Faith Beyond The Legal Jargon

This is where the concept of insurance bad faith comes in. It’s when an insurer unreasonably and without a legitimate reason refuses to honor its obligations to you. It's more than a simple disagreement over a claim's value; it's a fundamental breach of the trust you placed in them.

At its heart, every insurance policy has what’s known in the legal world as an implied covenant of good faith and fair dealing. Think of it as the unwritten rules of the road for your relationship with your insurer. It's a legal duty that requires them to treat you fairly and honestly, giving your interests the same level of consideration as their own bottom line.

The Broken Promise

So, what is insurance bad faith in plain English? It’s what happens when an insurer deliberately puts its own profits ahead of its duty to you. This isn't about an honest mistake or a legitimate dispute over technical policy language. It’s a conscious decision to handle your claim in a way that is fundamentally unfair.

Thankfully, the law recognizes this breach of trust and provides a way for policyholders to fight back. Across the country, legal frameworks exist to hold insurers accountable for actions like unreasonable claim delays, shoddy investigations, or flat-out refusing to pay what’s owed. This gives you the power to seek damages that can go far beyond your original policy limits, sending a clear message that this behavior won't be tolerated. You can learn more about the legal basis for these protections and how they shield consumers.

An insurer has a duty to not just investigate a claim, but to do so thoroughly and objectively. When they search only for reasons to deny coverage while ignoring evidence that supports it, they are stepping over the line from claim evaluation to bad faith.

It's critical to know the difference between a simple claim denial and a true bad faith action. A denial based on a clear and unambiguous policy exclusion is a normal, if frustrating, part of the process. Bad faith, on the other hand, involves a deeper level of misconduct.

Legitimate Claim Denial vs. Potential Bad Faith

Differentiating between a standard denial and potential bad faith is key to knowing your rights. The table below lays out the contrasts between a legitimate action based on policy terms and behavior that could signal a much more serious problem.

Action | Legitimate Claim Denial | Potential Bad Faith |

|---|---|---|

Investigation | The insurer conducts a prompt and thorough investigation, considering all evidence you provide. | The insurer unreasonably delays the investigation or ignores clear evidence supporting your claim. |

Communication | You receive a clear, written explanation for the denial that cites specific policy language. | The insurer provides vague reasons for denial, misrepresents policy terms, or fails to communicate at all. |

Settlement Offer | An offer is based on a reasonable evaluation of the damages, though it may be lower than you expected. | You receive a "lowball" offer that is drastically less than the claim's actual value, with no valid reason. |

Understanding this distinction is the first step toward protecting yourself. If your insurer's actions feel less like a fair assessment and more like a strategy to avoid paying, it might be time to get a professional opinion.

An experienced attorney can cut through the excuses and determine if the insurance company has truly crossed the line. If you believe your claim was handled unfairly, don't try to face them alone. In pain? Call Caine.

Recognizing Bad Faith Tactics Used by Insurers

Knowing the legal definition of insurance bad faith is one thing, but spotting it in the wild is another. Insurers have a playbook of tactics designed to protect their bottom line, often at your expense. These moves can be subtle, created to make you feel confused, frustrated, and ready to give up. Recognizing these red flags is the first step toward fighting back and holding your insurer to the promise they made when you bought the policy.

Don’t mistake these actions for isolated errors. When an insurer drags its feet, they might be hoping you’ll get tired of waiting and accept a fraction of what you deserve. When they twist the words of your policy, it's a calculated move to create doubt where there shouldn't be any. These are deliberate strategies, not simple slip-ups.

Unreasonable Delays and Stall Tactics

One of the oldest tricks in the book is the strategic delay. Sure, a complicated claim takes time to sort out, but an insurer acting in bad faith will invent unnecessary hold-ups without any good reason. This isn't just poor customer service; it’s a deliberate strategy to wear you down emotionally and financially.

Here’s what that looks like in the real world:

Going Silent: Your adjuster becomes a ghost. They don't return your calls or answer your emails for weeks on end, leaving you completely in the dark.

The Adjuster Shuffle: Just when you think you're making progress, your claim is handed off to a new adjuster. Now you have to start from scratch, explaining everything all over again.

Endless Paperwork Loops: The insurer keeps asking for the same documents you’ve already sent, trapping you in a cycle of repetitive, pointless tasks designed to do one thing: stall.

This waiting game is more than just an annoyance. It can stop you from getting your car fixed, your home repaired, or the medical care you need, piling stress on top of an already awful situation.

Inadequate Investigations and Lowball Offers

Your insurance company has a duty to conduct a prompt, fair, and thorough investigation. When they act in bad faith, they do the exact opposite. They might glance over the evidence, ignore crucial photos or reports you provide, or even hire their own "experts" to create a biased report that justifies denying your claim.

This shoddy investigation almost always leads to the next red flag: the lowball settlement offer. After barely looking at your claim, the insurer offers you an amount that is frankly insulting. They're betting that you’re desperate enough to take whatever you can get and walk away.

Think about it this way: Multiple contractors confirm your home has $75,000 in storm damage. Your insurer’s adjuster shows up, walks around for 15 minutes, and a week later you get an offer for $12,000 with no real explanation. That’s not a negotiation—it’s a slap in the face and a clear sign of bad faith.

Misrepresenting Your Policy or the Law

Insurance policies are notoriously dense and confusing, and some companies use that to their advantage. A classic bad faith tactic is to flat-out misrepresent what your policy says. An adjuster might tell you, "Sorry, that type of water damage isn't covered," when a careful reading shows it absolutely is.

They might also misstate Florida law or invent requirements that don't actually exist, all to make you think you don't have a case. These kinds of deliberate misinterpretations are at the heart of many bad faith claims. As detailed in industry analyses, these actions are a direct violation of their duties—you can find more insights on these common insurer bad faith behaviors on NAMIC.org.

When an insurer uses its expertise to mislead you instead of to help you, they’ve crossed a serious line. If any of this sounds familiar, it's time to act. Document every conversation, save every email, and don’t let them bully you. If their behavior feels wrong, it probably is. You don't have to face them alone. In pain? Call Caine.

Your Action Plan When You Suspect Bad Faith

It’s an incredibly frustrating feeling to be stonewalled by a massive insurance company, but you have more power than you might think. If you have a gut feeling that your insurer is acting in bad faith, it's time to act. Here’s a practical guide to building your case and protecting your rights, starting right now.

The key is to shift your mindset. You're no longer just a claimant waiting for a check; you are now the primary investigator building a case. Every phone call, every email, and every missed deadline needs to be treated with the seriousness it deserves. Your goal is to create a crystal-clear record of the insurer's behavior, leaving them no room to wiggle out of their responsibilities later.

Document Everything—Meticulously

From this moment on, become a relentless record-keeper. Solid documentation is the bedrock of any successful challenge against an insurance company's bad faith tactics. Grab a notebook or start a digital file and log every single interaction.

For every phone call, make sure you jot down:

The date and time of the call.

The full name and title of the person you spoke with.

A quick summary of what was discussed, including any promises or key statements they made.

The call reference number, if they give you one.

This isn't just busywork. This organized log creates a timeline that can reveal a damning pattern of delays, contradictions, or outright avoidance. A single undocumented phone call is just your word against theirs. A detailed log showing a dozen unreturned calls over two months? That’s powerful evidence.

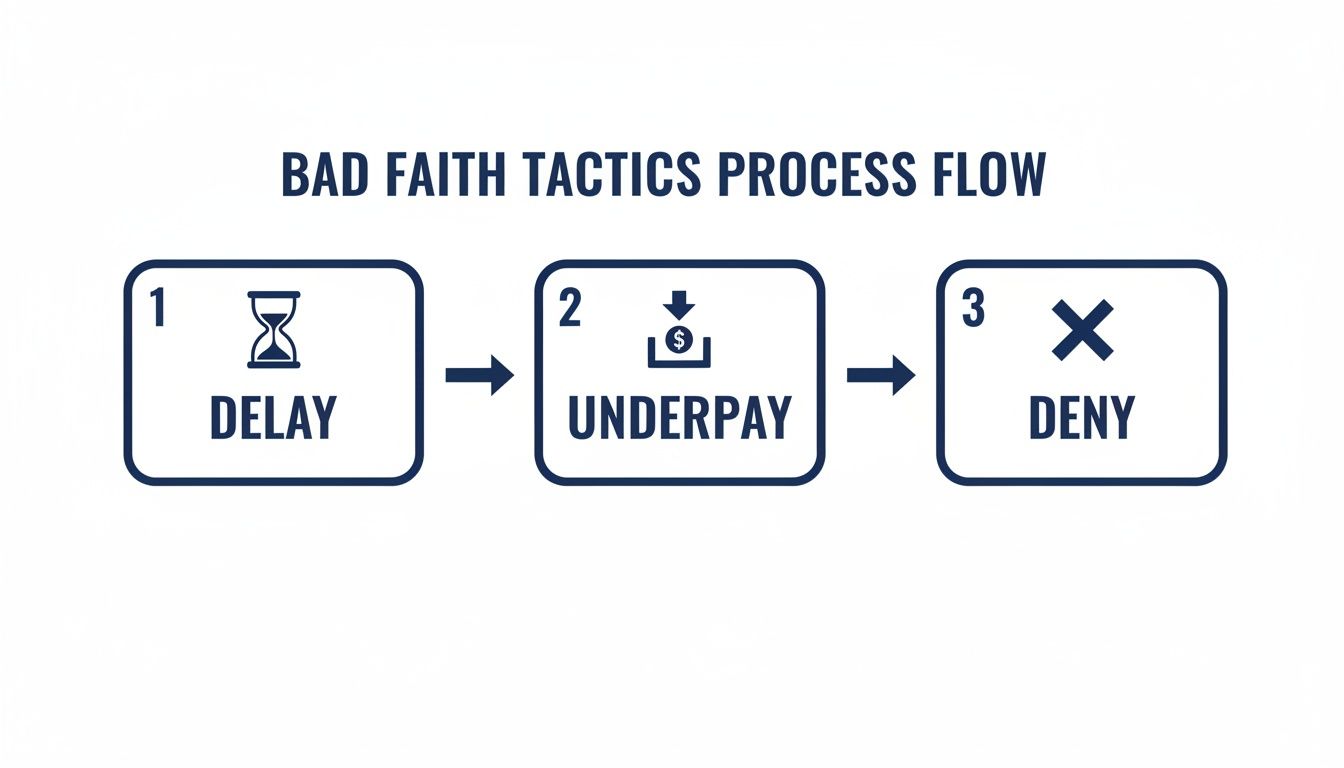

The process of bad faith often follows a predictable, frustrating path.

As you can see, it often starts with stalling tactics designed to wear you down before they move to underpay or deny your claim altogether.

Demand Answers and Build Your Own File

Never, ever accept a vague verbal denial. If your claim gets denied or the offer is ridiculously low, you need to formally demand a written explanation. That letter should force them to point to the exact policy language they are using to justify their decision.

A company's refusal to provide a clear, written reason for a denial is a massive red flag. It often means they don't have a legitimate leg to stand on and are just hoping you’ll give up.

While you're waiting on their response, get busy gathering your own proof. You are building an independent claim file to prove the real value of your loss. This is how you counter their lowball offers and lazy investigations.

To make sure you don't miss anything, we've put together a checklist of the essential documents you'll need. Think of this as building the foundation of your case.

Essential Evidence Checklist for Your Claim File

Evidence Type | Description & Importance | Example |

|---|---|---|

Your Insurance Policy | You need the complete policy, not just the summary pages. This includes all declarations and endorsements. It’s the contract that governs their obligations. | The 50-page PDF document your agent emailed you, not the one-page "declarations" summary. |

All Communications | Keep every single email, letter, and even text message. This creates an undeniable timeline of who said what and when. | Printouts of email chains with the adjuster; certified mail receipts for letters you sent. |

Photo & Video Proof | Take more photos and videos of the damage than you think you need, from every conceivable angle. Do this before any repairs begin. | Wide shots of a damaged roof, close-ups of water stains on the ceiling, video walkthrough of the affected rooms. |

Independent Estimates | Get detailed, written repair estimates from at least two reputable, independent contractors. This shows what a fair repair cost actually looks like. | A line-item estimate from a trusted local roofer that details labor and material costs. |

Medical Records | If you were injured, this is non-negotiable. Collect every doctor's note, hospital bill, and prescription receipt. | All records from your emergency room visit, physical therapy notes, and pharmacy bills. |

Proof of Value | For damaged personal property, you need to prove what it was worth. Find receipts, credit card statements, or professional appraisals. | The original receipt for your television; an appraisal for a damaged piece of jewelry. |

Having these documents organized and ready will give you a significant advantage and show the insurer—and your attorney—that you are serious about getting what you're owed.

Protect Your Legal Position

As you build your case, be very careful with what you say to the insurer. Never agree to give a recorded statement without talking to a lawyer first. Adjusters are trained to ask leading questions to trap you into saying something that weakens your claim.

Finally, keep a close eye on all deadlines. Missing a deadline to submit a form or, eventually, file a lawsuit can permanently sink your chances of recovery. If you feel overwhelmed or know you're not being treated fairly, it's time to get professional help. You don’t have to fight this battle alone. In pain? Call Caine.

The Florida Legal Standard for Bad Faith Claims

Navigating an insurance dispute in Florida means understanding that "bad faith" is much more than just a feeling of being treated unfairly. It’s a specific legal concept, and proving it is a high bar to clear. In the eyes of the law, terrible customer service, while incredibly frustrating, doesn't automatically equal bad faith.

To win a bad faith claim, you have to prove that your insurance company's actions weren't just wrong, but completely unreasonable and without any legitimate basis. This goes far beyond a simple disagreement over the value of a claim. The real task is to show the insurer failed to act fairly and honestly toward you when it could and absolutely should have.

The Totality of the Circumstances

Florida law doesn’t hang its hat on a single mistake or delay. Instead, courts look at the "totality of the circumstances" to figure out if an insurer’s conduct, taken as a whole, actually rises to the level of bad faith. This means every action—and every inaction—from the moment you filed your claim can become a crucial piece of evidence.

An insurer might try to excuse a three-month delay by blaming a single piece of missing paperwork. But a court will look at that delay alongside a log of unreturned phone calls, evidence of a biased investigation, and a ridiculously lowball offer to see the bigger picture: a pattern of unreasonable conduct.

The core question the court asks is whether the insurer's actions were "fairly debatable." If the company had a reasonable and legitimate reason for its decisions—even if that reason ultimately turned out to be wrong—it can often defeat a bad faith claim. Proving there was no fairly debatable reason is the key to winning your case.

This high standard is in place to prevent every single disputed claim from turning into a bad faith lawsuit, but it also creates a major hurdle for policyholders. It’s not enough to prove the insurer should have paid; you have to prove they had no good reason not to.

First-Party vs. Third-Party Claims

In Florida, the legal path for a bad faith claim can change slightly depending on what kind of claim you have. It's critical to know which category your situation falls into, as it will shape the entire legal strategy.

First-Party Bad Faith: This is the most common kind. It happens when you sue your own insurance company for dropping the ball on your claim. For instance, if your homeowner's insurance provider unreasonably denies your valid roof damage claim after a hurricane, you would file a first-party bad faith action. You are the "first party" to the insurance contract.

Third-Party Bad Faith: This situation pops up from a liability claim. Imagine you cause a car accident, and the injured person sues you. Your auto insurer has a duty to defend you and act in your best interests, which includes settling the claim against you within your policy limits if they can. If they refuse a reasonable settlement offer and the case goes to trial—resulting in a verdict against you that is way above your policy limits—you could sue them for third-party bad faith for failing to protect you from that massive judgment.

Understanding these distinctions and the demanding legal standard in Florida is essential. An insurer will throw every legal argument it has at the wall to show its actions were "fairly debatable." Building a case that can overcome this defense requires meticulous documentation and a deep understanding of Florida insurance law.

If you believe your insurer has broken its duty of good faith, you need an advocate who knows these complex legal standards inside and out. You don’t have to decipher the law on your own. In pain? Call Caine.

What You Can Recover in a Bad Faith Lawsuit

When an insurance company acts in bad faith, the financial damage can spread far beyond the original unpaid claim. A successful bad faith lawsuit isn’t just about getting the money you were initially owed; it’s about holding the insurer accountable for the entire mess their actions created.

The law recognizes that a wrongful denial can set off a chain reaction of financial and emotional hardships. Fortunately, it also provides a way for you to recover damages for all of them. This is why understanding what you can recover is so critical. A bad faith verdict is meant to make you whole again, putting you back in the financial position you would have been in if the insurer had just done the right thing from the start.

The Full Value of Your Original Claim

Naturally, the foundation of any recovery is the full value of the benefits your policy should have paid in the first place.

If your insurer wrongly denied a $50,000 claim for storm damage to your home, that $50,000 is the starting point. But it doesn't stop there. This is just the beginning of holding them accountable for the consequences of their bad faith conduct.

Consequential Damages: The Ripple Effect

This is where a bad faith claim gets its teeth. The most critical part of a recovery is often what the law calls consequential damages. Think of these as the ripple effect—the reasonably foreseeable losses you suffered as a direct result of the insurer's wrongful denial or delay.

Common examples of these ripple-effect damages include:

Lost Income or Business Profits: Maybe the failure to repair your work vehicle or business property kept you from earning a living.

Damage to Your Credit Score: Did you have to run up credit cards or default on loans to cover expenses the insurer should have paid?

Foreclosure or Repossession: In the worst-case scenarios, an insurer’s failure to pay can lead to you losing your home or car.

Additional Living Expenses: All the costs you racked up for temporary housing or other necessities while waiting for a payment that never arrived.

Essentially, if the insurer's bad faith caused a separate financial injury, you can seek compensation for it. This is a crucial element in many personal injury cases where insurance disputes arise, making an already difficult recovery even harder.

Damages for Emotional Distress and Attorney Fees

The stress, anxiety, and frustration of battling an insurance company can be enormous. Florida law gets this, and it allows victims to recover damages for emotional distress, mental anguish, and inconvenience.

Proving your claim forced you to relive a traumatic event, deal with constant financial pressure, and fight for months or even years. These damages acknowledge that the harm you suffered wasn't just financial—it was deeply personal.

On top of that, if you win your bad faith lawsuit, the insurer is typically required to pay your attorney’s fees and legal costs. This provision is vital. It levels the playing field, allowing you to hire a qualified attorney to fight for your rights without having to worry about the cost of taking on a corporate giant.

The stakes in these disputes are incredibly high. With the overall cost of liability claims in the U.S. hitting $429 billion, and Florida households paying some of the highest insurance costs in the nation, the pressure on insurers can lead to aggressive, bad faith tactics. You can discover more insights about U.S. bad faith claim trends on Marsh.com.

If you’re facing a wall of denial from your insurer, you don’t have to absorb the consequences alone. An experienced attorney can calculate the full extent of your damages—every last ripple—and fight for the compensation you deserve.

In pain? Call Caine.

Why an Experienced Bad Faith Attorney Is Essential

Trying to take on a massive insurance company by yourself is the modern-day version of David versus Goliath. These companies don't just have deep pockets; they have entire legal departments and decades of experience dedicated to one thing: protecting their profits. Going it alone is more than just stressful—it puts you at a serious, and often costly, disadvantage.

This is exactly why hiring a seasoned bad faith attorney isn't just a smart move; it's the only way to level the playing field. These lawyers aren't just legal experts. They are your personal advocates in a system that feels intentionally stacked against you.

Leveling the Legal Playing Field

A lawyer who specializes in insurance bad faith knows every trick in the insurer's playbook. They’ve seen all the tactics used to delay, deny, and underpay legitimate claims, and they understand the complex web of Florida law, including every procedural deadline and legal nuance. Most importantly, they know how to build a powerful case that can stand up to the most aggressive defense an insurance company can muster.

Simply hiring an attorney sends a clear signal to the insurer: you mean business, you know your rights, and you won’t be bullied. That single action can completely change the dynamic, forcing the company to take you and your claim seriously right from the start.

An unrepresented policyholder often looks like an easy target for a quick, lowball settlement offer. The moment an experienced law firm gets involved, that same insurer knows their usual delay-and-deny games won't fly. They're now facing a real legal threat.

Maximizing Your Financial Recovery

One of the most crucial things a bad faith attorney does is calculate the full value of your damages—and it’s often far more than just the original claim amount. They dig deep to uncover and prove all the related losses you've suffered, like lost income or damage to your credit score, which you might not have even known you could recover.

To build the strongest case possible, your attorney will bring in the heavy hitters, including:

Expert Witnesses: Professionals like engineers, contractors, or medical specialists who can provide rock-solid testimony on the true scope and cost of your damages.

Forensic Accountants: These specialists are experts at tracing the financial ripple effects of a denied or delayed claim, proving things like lost business profits and other monetary harm.

By putting together a detailed, evidence-backed demand, your lawyer is in a prime position to negotiate a fair settlement. And if the insurance company still refuses to do the right thing? Your attorney will be ready to take them to court. After all, untangling complex insurance disputes is what they do best.

Don’t let an insurer’s bad faith tactics control your future. You have every right to fight back with a powerful advocate in your corner. In pain? Call Caine.

Frequently Asked Questions About Insurance Bad Faith

When you're trying to navigate the choppy waters of an insurance claim, a lot of questions can pop up. This section tackles some of the most common concerns we hear from policyholders who feel like their insurance company is giving them the runaround.

How Long Do I Have to File a Bad Faith Claim in Florida?

In Florida, the clock starts ticking the moment your insurer acts in bad faith. You generally have five years from the date the company breached its duty to you to file a lawsuit. But don't let that number fool you into waiting.

This deadline, legally known as the statute of limitations, can get tricky. Pinpointing the exact date the "breach" happened isn't always cut and dry. Was it the day they denied your claim without a good reason? The day an unreasonable delay started? Because of this gray area, it's critical to talk to an attorney as soon as you suspect something is wrong. Waiting too long could mean losing your right to seek justice for good.

Can I Sue if the Insurer Eventually Paid but Took Too Long?

Yes, absolutely. A check that shows up months or years late doesn't just erase the damage done. The heart of a bad faith claim isn't just about if you got paid, but how and when the insurance company handled its obligations.

An unreasonable delay can be just as devastating as an outright denial. If an insurer's foot-dragging forced you into debt, wrecked your credit, or allowed your property to suffer even more damage while you waited, you may have a strong case. You can seek compensation for all those extra damages, even if they eventually paid the original amount owed.

What Is the Difference Between Breach of Contract and Bad Faith?

This is a really important distinction, as it completely changes what you can recover in a lawsuit. Think of it like this: a breach of contract is about the policy itself, while bad faith is about the insurer's terrible behavior.

Breach of Contract: This lawsuit is all about getting the money you were owed under your policy. If your policy covers $50,000 in damages and the insurer flat-out refuses to pay, a breach of contract lawsuit aims to force them to pay that $50,000. It’s about enforcing the deal you made.

Insurance Bad Faith: This is a separate and more serious legal action. It goes beyond the policy limits and focuses on the insurer's wrongful conduct—the shady delays, the ridiculous lowball offers, and the dishonest tactics. In a successful bad faith case, you can recover not just the policy benefits but also compensation for your financial losses, emotional distress, and attorney's fees.

Knowing your rights and the details of these claims is the first step toward holding your insurer accountable. For more deep dives into these topics, feel free to explore the resources on the CAINE LAW blog.

At CAINE LAW, we know the playbook insurance companies use, and we fight to protect your rights every step of the way. If you’re getting the runaround, you don't have to face them alone. In pain? Call Caine. Contact us today for a free, no-obligation consultation at https://cainelegal.com.