In Pain? Call Caine

Decoding Slip and Fall Settlement Amounts

5 Min read

By: Caine Law

Share

If you’ve been hurt in a slip and fall, one of the first questions on your mind is probably, "What is my case actually worth?" While there’s no magic number that fits every situation, most of these cases end up settling somewhere in the $10,000 to $50,000 range.

But that’s just a ballpark. To figure out where your specific case might land, we need to dig into the details.

Demystifying Typical Slip and Fall Settlement Amounts

Think of a settlement not as a fixed price tag, but as a unique recipe. The "ingredients" of your case—like the severity of your injuries and the strength of your evidence—determine the final outcome. A minor sprained ankle just won't command the same value as an injury that requires complicated surgery and months of rehab.

Ultimately, how clearly you can prove the property owner was at fault is one of the biggest factors that will push your claim toward the higher or lower end of that spectrum.

Understanding the Common Settlement Brackets

While every case has its own story, settlements tend to group together based on how badly someone was hurt. It usually breaks down like this:

Minor Injuries: These are your sprains, strains, or bad bruises. Since medical treatment is usually pretty limited, the settlements tend to be on the smaller side.

Moderate Injuries: When you’re dealing with something more serious like broken bones, a concussion, or an injury that needs ongoing physical therapy, the settlement value naturally goes up.

Severe Injuries: This is where you see the most substantial settlements, often hitting six or even seven figures. These cases involve catastrophic harm like traumatic brain injuries, spinal cord damage, or the need for multiple, complex surgeries.

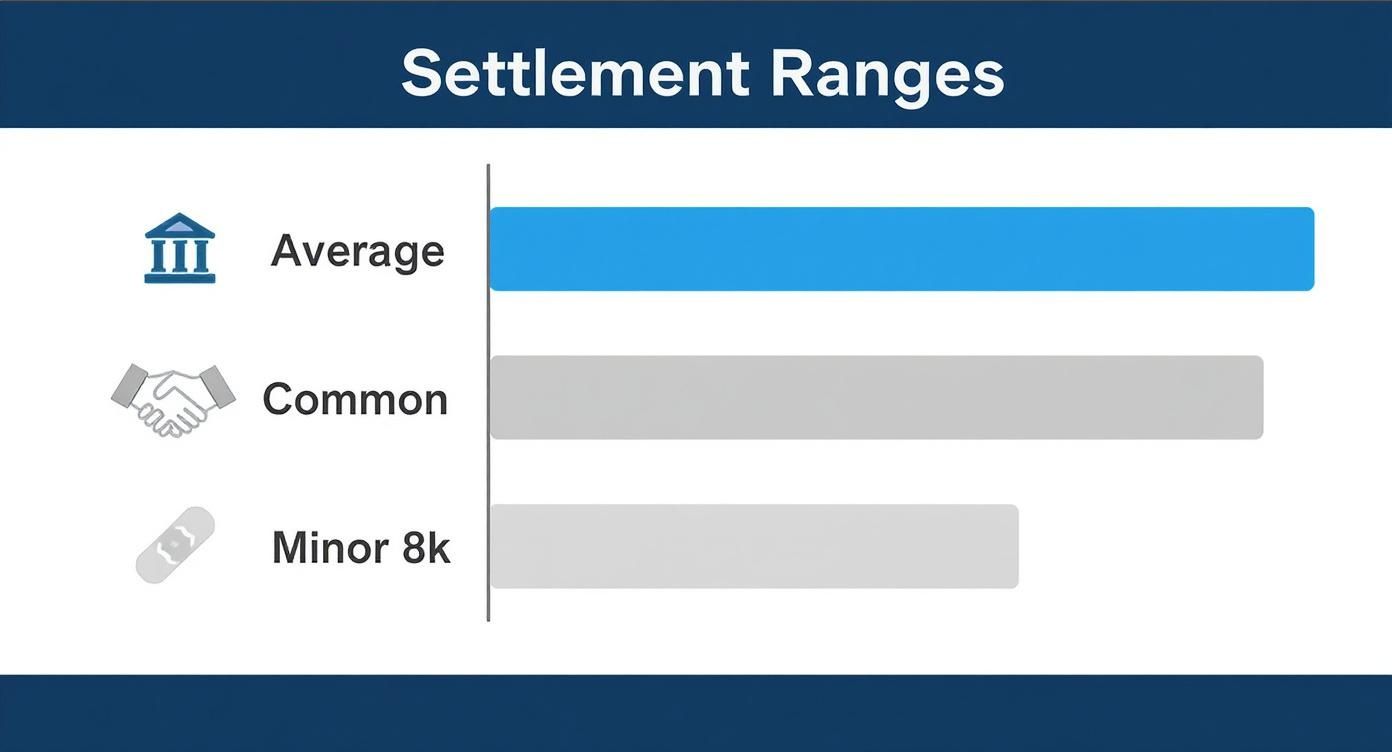

The infographic below gives a good visual breakdown of the most common settlement ranges you'll see in these types of claims.

As you can see, while the average can look high, the most frequent outcomes are often more modest. It's a great reminder to keep expectations realistic from the start.

A Look at the Numbers

Let's ground this in some real-world data. One recent analysis of over 5,800 personal injury cases found that the average settlement for a slip and fall was about $55,056. But for minor soft tissue injuries, settlements were much lower, typically falling between $2,000 and $8,000.

A key takeaway here is that an "average" figure can be a bit misleading. It's often pulled way up by a handful of multi-million dollar cases. The most common settlement range gives you a much more practical snapshot of what most people can expect.

Trying to figure all this out on your own can feel completely overwhelming, especially when you’re trying to recover. This is exactly where getting professional guidance can make all the difference. Understanding the ins and outs of personal injury law is crucial if you want to avoid getting a lowball offer from an insurance company that just wants to close your file. Every piece of the puzzle, from your medical bills to proving the owner was negligent, helps build a stronger case.

If you’re not sure what your claim is worth, the best first step is to get some legal advice. In pain? Call Caine.

The Building Blocks of Your Settlement Value

Insurance companies don’t just pull settlement offers out of a hat. Their numbers come from a specific formula, adding up quantifiable losses they call damages. Think of these damages as the individual bricks that build the foundation of your entire claim.

Each brick represents a different way the fall has turned your life upside down. Getting a handle on these building blocks is the absolute first step toward a fair settlement that actually covers what you’ve lost. Let's break down the four crucial components at the core of nearly every slip and fall case.

Building Block 1: Medical Expenses

The most obvious cost of a slip and fall is the mountain of medical bills that quickly piles up. This is always the starting point for negotiations because these expenses are concrete and easy to document. But it's about much more than just the bills you have right now.

A fair settlement has to account for every medical need, both past and future.

Immediate Medical Costs: This covers everything from the ambulance ride and ER visit to X-rays, MRIs, and any surgeries or prescriptions you needed right after the fall.

Ongoing and Future Care: This is the part people often forget, and it's critical. It’s an estimate for future physical therapy, ongoing rehabilitation, potential follow-up surgeries, chronic pain management, and even things like a wheelchair or necessary modifications to your home.

An insurance adjuster will pick apart every single expense, so keeping meticulous records is essential. If you fail to account for future medical care, you could be stuck paying for your injury-related costs out of pocket for years to come.

Building Block 2: Lost Income and Earning Capacity

A serious injury doesn't just hurt you physically; it can deliver a devastating blow to your finances. Lost income is another key building block, representing the wages you couldn't earn because you were recovering. But the calculation goes much deeper than just a few missed paychecks.

The real value here is based on how the injury impacts your ability to work—both now and for the rest of your career.

An injury that forces a construction worker into a lower-paying desk job will have a much higher "lost earning capacity" value than an office worker who misses two weeks but returns to their job without any long-term limitations.

To get the full picture, you have to calculate:

Wages Already Lost: This is the straightforward sum of money you missed out on from the day you were hurt until you went back to work. You'll prove this with pay stubs, W-2s, and letters from your employer.

Diminished Earning Capacity: This is where it gets more complex. It's a projection of how the injury will limit your earning potential for the rest of your life. If your injuries are permanent and you can no longer do your old job, this piece of the settlement can be massive.

Building Block 3: Pain and Suffering

This is often the largest part of a settlement, but it's also the hardest to pin a number on. How do you put a price tag on physical pain, emotional distress, or the simple loss of enjoyment in life? There's no receipt for suffering, but it is a very real, and very compensable, damage.

Insurance companies typically use one of two methods to assign a dollar value to these "non-economic" damages.

The Multiplier Method: This is the go-to approach. The adjuster takes your total economic damages (medical bills + lost wages) and multiplies that figure by a number, usually between 1.5 and 5. A minor sprain might get a 1.5 multiplier, while a catastrophic injury that changes your life forever could get a 4 or 5.

The Per Diem Method: This approach is less common. It assigns a daily rate (say, $100 per day) for your pain and multiplies it by the number of days you were recovering.

The multiplier they choose depends entirely on how bad the injury was, how long it took to recover, and whether you're left with any permanent problems.

Building Block 4: Strength of Proof

The final—and arguably most important—building block isn't a type of damage at all. It's the evidence you have to back up your claim. You can have a severe injury and thousands in lost wages, but if you can't prove the property owner was negligent, your claim is worth next to nothing.

Strong evidence is your leverage. It forces the insurance company to take you seriously.

Evidence That Boosts Settlement Value

Evidence Type | Why It Matters |

|---|---|

Clear Photos/Videos | This is visual proof of the hazard (a wet floor, a broken stair) before the owner can clean it up or fix it. |

Incident Report | It creates an official, time-stamped record of the event with the property owner. |

Witness Statements | This provides an unbiased, third-party account confirming the dangerous condition and how you fell. |

Medical Records | These documents directly connect your specific injuries to the fall, establishing what we call causation. |

Without this proof, the insurer has an easy out. They'll just argue you were clumsy or that the hazard never existed. Every piece of evidence you collect adds weight to your side of the scale and strengthens your negotiating position. If you're struggling to calculate these damages or gather the right proof, don't leave money on the table. In pain? Call Caine.

How Proving Negligence Shapes Your Settlement

Just getting hurt on someone else's property isn't enough to get the settlement you deserve. The key that unlocks your right to compensation is one critical legal concept: negligence. You have to be able to prove that the property owner failed to act with reasonable care and that their failure led directly to your fall.

Think of it this way: a grocery store isn't automatically on the hook just because a customer spills a drink. But if they knew about that spill—or should have known about it—and did nothing to clean it up or warn people in a reasonable amount of time, that's where their liability kicks in. This legal responsibility is known as a duty of care.

The Duty of Care Explained

Every single property owner in Florida, from a giant theme park down to a small neighborhood coffee shop, has a legal obligation to keep their grounds reasonably safe for visitors. This isn't a passive duty. It means they must actively look for potential hazards, fix them, and clearly warn people about any dangers that can't be repaired right away.

To prove negligence, your lawyer will need to establish a few key things:

The Owner Knew: This is called "actual knowledge." It's when you can show the owner or an employee saw the hazard and just walked away. An employee spotting a puddle and ignoring it is a perfect example.

The Owner Should Have Known: This is more common and is referred to as "constructive knowledge." It means a dangerous condition was there for so long that any reasonably attentive owner would have discovered it and fixed it. That piece of wilted, brown lettuce on the produce aisle floor? It didn't just get there.

Failure to Act: The owner either knew or should have known about the danger but failed to take the right steps, like mopping a spill, putting up a "Wet Floor" sign, or roping off a broken step.

Without proving this breach of duty, the insurance company will simply call your fall an unfortunate accident, not the result of the property owner's carelessness. That's why evidence showing how long a hazard existed is so vital for a strong claim.

Florida’s Modified Comparative Negligence Rule

Proving the owner was negligent is only half the battle. You can bet the insurance adjuster will try to turn the tables and shift some of the blame onto you. In Florida, this is handled by a rule called modified comparative negligence.

This rule means your final settlement will be reduced by your percentage of fault. If you're found to be partially responsible for your own injuries, your compensation gets cut.

For example, let's say you're walking through a dimly lit parking lot while texting. You trip over a huge, cracked piece of pavement and break your ankle. The total value of your damages comes out to $50,000.

A jury might decide the property owner was 80% at fault for not fixing the pavement or installing better lighting. But, they might also find you were 20% at fault for not watching where you were going.

Under Florida law, your $50,000 award would be reduced by your 20% share of the fault. You would walk away with $40,000. Critically, if you are found to be more than 50% at fault for the accident, you are barred from recovering any money at all.

How Comparative Fault Impacts Your Settlement Amount

Insurance companies are masters at using comparative fault to shrink their payouts. They will dig for any reason to assign blame to you, often arguing that:

You were wearing the wrong shoes (like high heels on a freshly mopped floor).

You were distracted by your phone or talking to a friend.

The hazard was "open and obvious," and you should have seen and avoided it.

You were in a part of the property where customers aren't allowed.

An experienced attorney knows these tactics well. Our job is to fight back against these accusations. By gathering powerful evidence—security footage, witness statements, and expert opinions—we can work to minimize your percentage of fault and protect the full value of your settlement.

Proving negligence is complex, but you don't have to do it alone. In pain? Call Caine.

Anatomy of a High-Value Slip and Fall Case

While most slip and fall settlements fall into a fairly predictable range, a select few generate life-altering, multi-million dollar awards. These aren't your average cases. They're the result of catastrophic harm colliding with clear, undeniable negligence.

Looking at what makes these high-value claims tick helps us understand the upper limits of what a settlement can be. A multi-million dollar result is almost always tied to injuries so severe and permanent that they completely shatter the victim's life. We're not talking about temporary pain here; we're talking about a total loss of normalcy and independence.

The Role of Catastrophic Injuries

The biggest driver behind a massive settlement is the injury itself. When an accident causes catastrophic harm, it kicks off a decades-long ripple effect of damages, sending the claim's value through the roof.

Think of it this way: a small crack in your car's windshield is a manageable repair. But if the engine explodes, the car's entire purpose is destroyed. Catastrophic injuries do the same thing to a person's life.

The injuries we often see in these cases include:

Traumatic Brain Injuries (TBI): These can leave victims with permanent cognitive problems, personality changes, and even the need for 24/7 medical care.

Spinal Cord Damage: An injury that leads to paralysis (paraplegia or quadriplegia) means a lifetime of expensive medical treatments, specialized mobility equipment, and major home modifications.

Multiple Complex Surgeries: When a case involves numerous operations, long hospital stays, and grueling, painful rehabilitation, the value naturally climbs.

These injuries don't just create a mountain of medical bills. They often mean the victim can never work again—a complete and permanent loss of earning capacity. This factor alone can tack millions onto a settlement.

When Negligence Is Blatant and Undeniable

The second crucial ingredient for a high-value case is extreme, blatant negligence. The property owner's disregard for safety has to be so obvious that an insurance company knows it would be a massive risk to face a jury.

This could be a situation where a property owner knew about a dangerous hazard for months, got multiple complaints about it, and flat-out chose to do nothing before someone was seriously hurt.

For instance, one well-known case involved a woman who suffered a brain injury and seizures after slipping in a Virginia convenience store, resulting in a $12.2 million award. In another, a University of Pennsylvania medical student who fell into an open manhole, breaking his back, received a settlement capped at $18 million. You can explore more about these significant slip and fall settlements to see what separates them from the rest.

These examples make it clear: when blatant carelessness meets life-altering harm, slip and fall settlement amounts can reach staggering figures. If you've suffered a devastating injury, you need a legal team that knows how to prove the full, long-term impact of your ordeal. In pain? Call Caine.

Building an Unshakeable Evidence File

A slip and fall claim lives and dies on the strength of its proof. Without solid, undeniable evidence, even the most legitimate case can get picked apart by an insurance adjuster looking for any reason to deny or devalue your claim.

Think of yourself as a detective at the scene of your own accident. Every detail you capture helps build a case file that tells a clear, convincing story of what happened and why the property owner is responsible. The more proof you gather from the very beginning, the less room an insurance company has to argue.

Start with Immediate Documentation

The moments right after a fall are chaotic, but they're also the most critical for gathering evidence. That puddle of water, broken floor tile, or slick patch of ice can be cleaned up or repaired in minutes, erasing your best proof forever.

Pull out your smartphone immediately. Before you do anything else, take photos and videos from every angle imaginable. Get close-ups of the specific hazard, wider shots of the surrounding area, and pictures showing the lighting conditions or lack of warning signs. This kind of visual proof is incredibly difficult for an insurance company to dispute and can make a massive difference in slip and fall settlement amounts.

Secure Credible Witness Statements

Nothing backs up your story like an unbiased, third-party account. If anyone saw you fall or can confirm the dangerous condition was there before your accident, their testimony is pure gold.

Get their name and phone number on the spot. Even a quick, signed note describing what they saw can be a powerful tool later on. It’s much harder for an insurer to claim you were just clumsy when an independent witness says otherwise.

A key legal strategy is establishing that the property owner had "constructive knowledge" of the hazard. A witness who can state, "I saw that spill 30 minutes ago and no one cleaned it up," provides powerful leverage during negotiations.

The Non-Negotiable Medical Paper Trail

Your medical records are the official link between the fall and your injuries. Without a complete paper trail, an insurance company will jump at the chance to argue your injuries were pre-existing or unrelated to the incident.

Go see a doctor right away, even if you think you’re okay. Some serious injuries, like concussions or internal damage, don’t show up immediately. Make sure to follow all medical advice, go to every follow-up appointment, and keep a file of every single bill and receipt. This creates an unbroken chain of proof.

For more guidance, we've outlined the essential steps and legal guidance for accidents in another one of our posts.

File an Official Incident Report

Always report the fall to a manager or the property owner before you leave. This creates an official, time-stamped record that the event occurred. When you file the report, stick to the facts—what happened and where.

Never apologize or say anything that sounds like you’re accepting blame. Simply state that you fell because of a specific hazard and were hurt. Ask for a copy of the report for your records. It acts as the business’s own acknowledgment that something happened on their watch.

To help you stay organized, we've put together a simple checklist of the evidence you'll want to gather.

Your Slip and Fall Evidence Checklist

Evidence Category | What to Collect | Why It's Important |

|---|---|---|

Scene Photos & Videos | Pictures of the hazard, surrounding area, warning signs (or lack thereof), and your injuries. | Creates undeniable visual proof of the dangerous condition before it's cleaned up or fixed. |

Witness Information | Names, phone numbers, and a brief signed statement of what they saw. | Provides an unbiased, third-party account that backs up your version of events. |

Medical Records | All doctor's notes, hospital bills, receipts for prescriptions, and therapy records. | Directly links the fall to your injuries and proves the financial cost of your medical care. |

Incident Report | A copy of the official report filed with the property manager or business owner. | Serves as official, time-stamped acknowledgment from the business that the incident occurred. |

Proof of Lost Income | Pay stubs, tax returns, and a letter from your employer detailing missed work days. | Documents the financial impact of your injuries on your ability to earn a living. |

Personal Log | A daily journal detailing your pain levels, physical limitations, and emotional distress. | Helps to quantify your "pain and suffering" and demonstrates the day-to-day impact on your life. |

Gathering this evidence can feel overwhelming, especially when you're in pain. If you need help building your case, we are here to fight for you. In pain? Call Caine.

A Few Common Questions We Hear All the Time

Even after breaking down all the factors, you probably still have some specific questions running through your mind. That's completely normal. Let's tackle a few of the most common ones we get from clients to give you a clearer picture of what to expect.

How Long Does a Slip and Fall Settlement Take?

This is the million-dollar question, and the honest answer is: it depends. There’s no magic number. A straightforward case where the fault is crystal clear and the injuries are minor might wrap up in 6 to 9 months.

But when you’re dealing with serious injuries, a fight over who was at fault, or the need for long-term medical care, the timeline can stretch out. These more complex cases can easily take over a year, especially if we have to file a lawsuit to get the insurance company to take you seriously.

A good personal injury lawyer is your timeline manager. Our job is to keep the ball rolling—gathering evidence, making sure every medical visit is documented, and pushing back against the insurance company's inevitable stalling tactics.

Are Slip and Fall Settlement Amounts Taxable?

This is a big one, and the answer isn't a simple yes or no. For the most part, the money you receive to compensate you for physical injuries and medical bills is not taxable, according to the IRS. They see it as making you whole again, not as income.

However, certain parts of a settlement can be taxed.

Lost Wages: Any money you get to cover lost income is usually taxed, just like your regular paycheck would have been.

Emotional Distress: This can be a gray area. If the emotional distress damages aren't directly linked to a physical injury, they might be taxable.

Punitive Damages: On the rare occasion punitive damages are awarded, you can bet they will almost always be taxed as income.

Because this gets complicated fast, it's always smart to talk with your lawyer and a tax professional. You need to understand the full financial picture before you sign on the dotted line.

Understanding the financial side of your settlement is just as crucial as getting a fair offer in the first place. Before you bring an attorney on board, it helps to have your questions ready. You can get a head start by reviewing these 9 questions to ask your slip and fall attorney before hiring them.

Can I Get a Settlement if a Wet Floor Sign Was Posted?

Yes, absolutely. Just because a "Wet Floor" sign was somewhere in the vicinity doesn't give a property owner a free pass. The real legal question is whether the warning was adequate and reasonable for the situation.

Think about it. Was the sign actually visible? Or was it tucked behind a plant? Was it big enough to catch your eye, or so small you'd easily miss it? A sign placed 30 feet away from the actual spill doesn't do anyone much good.

If that sign was knocked over, hidden, or otherwise ineffective, the owner can still be found negligent. Here in Florida, our comparative fault rules might mean your compensation is reduced if you were partially at fault, but a poorly placed sign is far from an open-and-shut defense for them.

Why Hire a Lawyer for a Slip and Fall Claim?

Let's be blunt: you're going up against a massive insurance company. Their goal is to pay you as little as possible, and they have entire teams of adjusters and lawyers dedicated to that mission. Hiring a lawyer simply levels the playing field.

An experienced attorney knows exactly what it takes to prove negligence under Florida law. We can get our hands on evidence you can't, like internal company incident reports or security footage they’d rather you never saw.

More importantly, we know how to calculate what your case is truly worth. That’s not just your current hospital bills. It’s the cost of future physical therapy, your lost ability to earn a living, and the very real value of your pain and suffering. We are trained negotiators who see right through the lowball offers and delay tactics that insurers use every single day. The data doesn't lie: people with legal representation consistently walk away with significantly more compensation than those who go it alone.

At CAINE LAW, we have the experience to build a powerful case on your behalf, ensuring you are positioned to receive the maximum compensation you deserve. We handle the legal fight so you can focus on healing. If you are struggling after a fall, don't wait. In pain? Call Caine.