In Pain? Call Caine

How to Calculate Pain and Suffering Damages in Florida

5 Min read

By: Caine Law

Share

Figuring out a dollar amount for pain and suffering isn't simple. Insurance companies often use a couple of standard starting points. There’s the multiplier method, where they take your total medical bills and other hard costs and multiply them by a number between 1.5 and 5. Then there’s the per diem method, which tries to assign a daily dollar value to what you’ve gone through.

The final number, however, is never that formulaic. It really comes down to the severity of your injuries, how drastically your life has changed, and how well you can prove it.

What Pain and Suffering Really Means in Florida

Before we get into the math, it’s critical to understand what "pain and suffering" actually covers in a legal sense. This isn't about getting revenge. It's about getting fair compensation for the real, human cost of an accident—the kind of harm that doesn’t show up on a bill or a receipt.

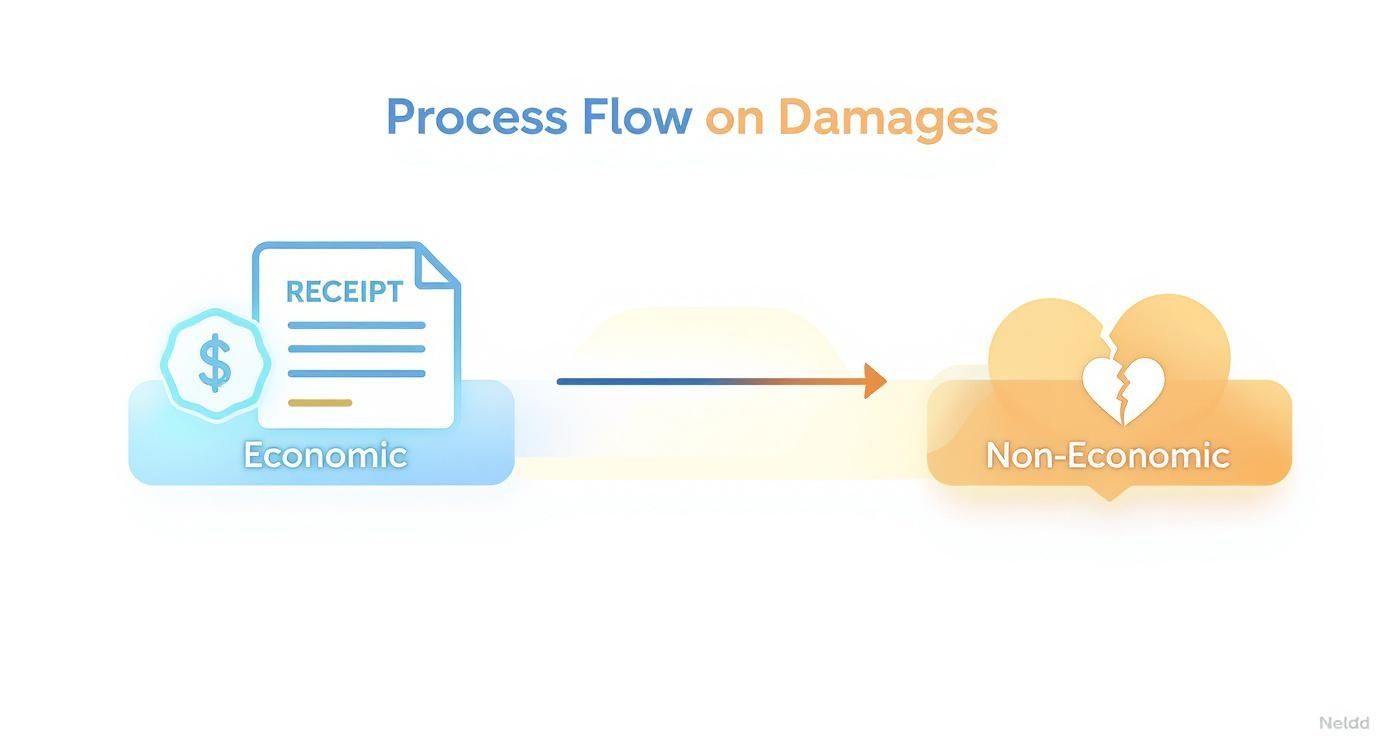

In Florida's courts, damages are divided into two buckets. The first is for economic damages. These are the straightforward, tangible losses you can add up. Think of anything you have a receipt for: medical bills, lost paychecks from missing work, and the estimated cost of future medical needs.

The second bucket is for non-economic damages, which is the official term for pain and suffering. This category exists to compensate you for all the profound, personal ways an injury has turned your life upside down.

Beyond the Bills: The Human Cost of an Injury

Pain and suffering is a broad umbrella term. It’s meant to cover the whole spectrum of physical and emotional turmoil that follows an injury caused by someone else's carelessness. It's so much more than just the immediate physical hurt.

It’s about the real-world experiences you’re forced to endure, like:

Physical Pain: The constant, nagging ache from a herniated disc, the sharp, searing pain of a broken leg, or just the day-in-day-out discomfort that comes with a long recovery.

Emotional Distress: The spike of anxiety you feel every time you have to get behind the wheel after a bad wreck, the depression that can creep in when you can't work or provide for your family, or the fear that you might never be the same again.

Mental Anguish: This covers the more severe psychological trauma that can develop, like post-traumatic stress disorder (PTSD), chronic insomnia, and other debilitating fears.

Loss of Enjoyment of Life: This is about all the little things that made life yours. Maybe you can no longer kneel down to play with your kids, go for your morning jog, or spend weekends gardening because the pain is too much.

At its core, pain and suffering damages are about providing a measure of justice for the quality of life that was stolen from you. It’s an acknowledgment that the true damage from an accident goes far beyond the financial balance sheet.

Why This Distinction Matters

Keeping economic and non-economic damages separate is crucial. It ensures the entire story of your ordeal is heard and valued. Just paying back your medical bills completely ignores the sleepless nights, the missed family moments, and the emotional trauma you’ve been put through.

A seasoned legal team knows how to weave all these elements together to tell your complete story. If you're struggling to document these less-obvious impacts, getting guidance from a dedicated personal injury firm can make all the difference.

Understanding this foundation is the first step. The next is to translate that human suffering into a concrete figure that an insurance adjuster—or a jury—can understand. That requires a smart strategy and rock-solid evidence.

In pain? Call Caine.

Using The Multiplier Method To Value Your Claim

When it comes to putting a dollar figure on pain and suffering, the most common tool in the legal world is the multiplier method. It’s not a perfect science, but it provides a solid, defensible starting point for negotiations with insurance companies.

The logic is pretty simple. First, you add up all your concrete, out-of-pocket financial losses. These are what we call your economic damages—every medical bill, physical therapy co-pay, lost paycheck, and even the projected cost of future care. Once you have that hard number, you multiply it by a factor that reflects the severity of your human losses.

That factor, the "multiplier," usually falls somewhere between 1.5 and 5. A minor injury that heals up completely might get a 1.5. A catastrophic, life-altering injury that leaves someone with permanent disabilities? That’s where you see multipliers of 4 or 5.

This chart gives you a clear visual of how your tangible financial losses become the foundation for your intangible pain and suffering claim.

As you can see, the path to valuing your non-economic damages starts with the pile of receipts and bills.

What Determines Your Multiplier

The real battle isn't about the math; it's about justifying the multiplier. Insurance adjusters are trained to argue for the lowest number possible. Our job is to build a case so compelling they have no choice but to agree to a higher one.

Several key factors will determine where on that 1.5-to-5 scale your case lands:

The Severity of Your Injuries: A broken arm that heals in a cast is worlds apart from a traumatic brain injury. The more devastating the initial harm, the higher the multiplier.

The Road to Recovery: Was it a few weeks of physical therapy or a year of multiple surgeries and grueling rehabilitation? A long, painful, and difficult recovery process absolutely justifies a higher multiplier.

The Long-Term Impact: Will you ever be the same? Injuries that result in permanent scarring, a limp, chronic pain, or the inability to return to your old job have a lasting impact that must be accounted for.

The Disruption to Your Life: This is about what was taken from you. Can you no longer play with your kids, enjoy your hobbies, or even perform basic daily tasks without help? The more your life has been turned upside down, the stronger the argument for a higher number.

The multiplier isn't just a number—it’s the story of your suffering, told in a language the insurance company understands. The more powerfully we can tell that story with hard evidence, the better the outcome.

Seeing The Multiplier Method In Action

Let’s look at a real-world example. Imagine a client, Maria, was rear-ended and racked up $25,000 in economic damages covering her ER visit, ongoing treatment, and time missed from work.

Her pain and suffering value, however, will change dramatically based on the human cost of her injuries.

The table below shows how different injury outcomes, all stemming from the same $25,000 in economic damages, result in wildly different valuations for her claim.

Factor | Calculation (based on $25,000 in economic damages) | Resulting Pain and Suffering Value | Injury Severity Example |

|---|---|---|---|

Low Impact | $25,000 x 1.5 | $37,500 | Maria suffers whiplash but recovers fully after a few months of physical therapy. |

Moderate Impact | $25,000 x 3 | $75,000 | The accident causes a herniated disc, requiring surgery and leaving her with chronic pain. |

Catastrophic Impact | $25,000 x 5 | $125,000 | The crash causes permanent nerve damage, ending her career and ability to enjoy her hobbies. |

As you can see, the exact same accident with the same initial medical bills can have a vastly different final value. It all comes down to the unique facts of your injury and how effectively we can prove its impact on your life.

This method is an industry standard because it grounds the subjective nature of "suffering" in the objective reality of financial loss. You can explore more about how these calculations are used in different scenarios in this detailed guide on calculating damages.

Fighting for a multiplier of 4 or 5 instead of settling for the 1.5 the adjuster offers is where an experienced personal injury attorney makes all the difference. We know how to gather medical expert testimony, depose witnesses, and use day-in-the-life videos to build a narrative so powerful it can’t be easily dismissed.

In pain? Call Caine.

Putting a Daily Value on Your Suffering: The Per Diem Method

While the multiplier method gives you a big-picture number, there's another way to look at it that can be very compelling, especially to a jury. It’s called the per diem method, which is just a fancy Latin way of saying "by the day." The idea is simple: you assign a dollar amount to every single day you've had to live with the pain and limitations from your injury.

Think of it like getting paid a wage for the miserable job of recovering from an accident. The logic is powerful because it's so easy to understand. If your time and effort were worth a certain amount at your job, shouldn't they be worth at least that much when you're forced to deal with constant pain and emotional distress? This approach creates a tangible, day-by-day record of your hardship.

How Do You Set a Fair Daily Rate?

The make-or-break part of a per diem calculation is landing on a daily rate that is both fair and, more importantly, defensible. You can’t just pull a number out of a hat. The most common and effective strategy is to use your actual daily earnings from before the accident as a baseline.

This approach is so effective because it directly ties your suffering to your proven economic worth. The argument becomes incredibly straightforward: if you were earning $250 a day to do your job, then enduring the agony of a shattered leg or the mental fog from a serious concussion is certainly worth at least that much. It takes the abstract idea of "suffering" and attaches a concrete, relatable number to it.

Of course, this isn't the only way. For people who were unemployed, retired, or had an income that fluctuated, we can find another reasonable benchmark. The goal is always to present a rate that makes logical sense based on your life and circumstances.

The Per Diem Method in Action: A Real-World Example

Let's walk through how this works in a practical sense. Imagine a construction worker here in Florida who takes a nasty fall on a poorly kept worksite, causing a serious back injury. His doctor is clear: he’s looking at six months of recovery and intensive physical therapy before he can even consider returning to such a physically demanding job.

Here’s how we’d start building his per diem claim:

His Daily Wage: He was making about $200 a day. We’ll use this as our daily rate for his suffering.

His Recovery Time: Six months works out to roughly 180 days of pain, limited mobility, and being unable to work or live his life normally.

From there, the math is simple and direct:

$200 (Daily Rate) x 180 (Days of Suffering) = $36,000 (Per Diem Value)

This $36,000 is the proposed value of his pain and suffering. It’s calculated completely separate from his economic damages, like his $36,000 in lost wages ($200/day x 180 days) and all his medical bills. It gives the insurance company a clear, logical reason for the compensation we’re demanding, tied directly to how long his ordeal lasted.

When Is the Per Diem Method the Right Tool?

The per diem method is a fantastic tool, but it's not the right fit for every single case. It really shines in situations where there's a clear, definable timeline for recovery.

This approach is most effective for:

Injuries with a predictable endpoint: Think broken bones, surgeries with standard recovery times, or other conditions where a doctor can confidently say when you’ll reach "maximum medical improvement."

Short-to-mid-term disabilities: When the suffering is intense but is expected to last for a specific number of months or maybe a year, the daily math is very persuasive.

Where this method falls short is with catastrophic injuries that cause permanent disability or lifelong chronic pain. In those tragic situations, trying to assign a daily value that stretches decades into the future just doesn't work—it becomes pure speculation. For those cases, the multiplier method is usually the better way to capture the enormous, long-term impact on someone's life. A good attorney will often calculate damages using both methods to build the strongest possible negotiating position.

If you’re facing a long road to recovery, don’t get lost trying to figure out these complex calculations on your own. We can help you build the strongest case for every penny you deserve. In pain? Call Caine.

How External Factors Can Change Your Settlement

After you’ve done the math with the multiplier or per diem methods, you get a starting figure. But it's critical to understand that this number is not the finish line. In the real world of personal injury claims, that initial calculation is more like a baseline—a solid starting point for negotiations that will get pushed and pulled by legal rules and practical limitations.

These external factors are exactly where an insurance adjuster will focus their energy to knock down your payout. Knowing what they are ahead of time gives you a realistic view of the road ahead and prepares you for the arguments they'll throw at you. In Florida, two of the biggest game-changers are the state's comparative fault rule and the at-fault party's insurance policy limits.

Florida’s Comparative Fault Rule

In Florida, the law gets that sometimes more than one person is to blame for an accident. This idea is called modified comparative fault. Under this rule, if you’re found to be partially responsible for what happened, your total compensation award gets cut by your percentage of fault.

But here’s the really critical part: if you are found to be more than 50% responsible for your own injuries, you are completely barred from recovering any damages. Zero. This makes proving the other party was overwhelmingly at fault an absolute necessity for your claim.

Here’s how it plays out in a real-world scenario:

You’re in a car wreck, and a jury decides your total damages are $100,000.

But, they also find you were 20% at fault for the crash because you were going a few miles over the speed limit.

Your final award would be slashed by that 20% ($20,000), leaving you with a final recovery of $80,000.

Insurance adjusters are masters at finding ways to shift blame. They'll argue you weren't paying attention, that you braked too suddenly, or that you didn't do enough to avoid the collision. Every single percentage point of fault they can pin on you is money their company saves.

The Reality of Insurance Policy Limits

This might be the single harshest reality in personal injury law: insurance policy limits. You can have a rock-solid case worth millions, but if the person who hit you only has a $50,000 insurance policy, that's often the absolute most you can get from their insurer.

It creates a frustrating and deeply unfair ceiling on your compensation, no matter how severe your pain and suffering is. We’ve seen it happen—a client with catastrophic injuries and a pain and suffering valuation of $500,000 might be forced to settle for a tiny fraction of that because the at-fault driver only carried the bare minimum insurance required by law.

An insurance policy's limit is a hard cap on what you can recover. A skilled attorney knows to immediately investigate every available insurance policy, hunting for things like umbrella policies or even other parties who could be held liable. The goal is to uncover every possible source of compensation.

State-Specific Caps and Legal Precedents

It's also important to remember that laws around damages can be wildly different from one state to the next. While the multiplier and per diem methods are common starting points, different places apply them in their own unique ways. Statistically, about 52% of personal injury lawsuits in the U.S. include a claim for pain and suffering, but how that value is determined is far from universal.

Some states put firm caps on these damages; California, for example, limits non-economic damages in medical malpractice cases. Fortunately, Florida does not currently have caps on pain and suffering damages for most personal injury cases, but knowing the broader legal landscape is still key. You can discover more insights on how different states handle these calculations.

These factors—comparative fault and insurance limits—are exactly why a simple calculator is never enough. You need a legal strategy designed to fight back against unfair blame and to find every dollar of recovery you’re entitled to.

In pain? Call Caine.

Building the Evidence to Prove Your Suffering

Figuring out a number for your damages is one thing; proving it is another battle entirely. You have to remember, an insurance adjuster’s primary job is to protect their company's bottom line. That means scrutinizing your claim and looking for any reason to pay out as little as possible.

Your word alone, no matter how honest, isn't going to cut it. You need to build a fortress of objective evidence that tells a clear, undeniable story of how this injury has turned your life upside down. Think of yourself as the lead investigator on your own case. Every photo, every doctor's note, every journal entry is a piece of the puzzle that justifies the compensation you're demanding.

Start a Detailed Daily Journal

One of the most powerful tools you have costs nothing: a simple daily journal. This isn't just a place to vent—it's a logbook of your new reality. Start it the day of the accident, if you can, and be relentlessly consistent.

Every day, jot down the facts:

Pain Levels: Rate your pain on a 1-10 scale. Where did it hurt? Was it a constant, dull ache or a sharp, shooting pain?

Emotional State: Were you anxious? Depressed? Frustrated? What specific things made you feel that way?

Daily Limitations: This is huge. Document all the things you couldn't do that day. Couldn't lift your toddler? Couldn't walk the dog more than a few feet? Couldn't cook dinner or sleep through the night? Write it down.

Medication Side Effects: Are your prescriptions making you drowsy, nauseous, or unable to focus? Note that, too.

This journal turns your subjective experience into a tangible, day-by-day record. When an adjuster tries to downplay your ordeal, a detailed log from the last 90 days is a powerful counterargument they can't easily dismiss.

Visually Document Your Injuries

A picture is worth a thousand words, and in a personal injury claim, it might be worth thousands of dollars. Photos and videos provide graphic, undeniable proof of your physical trauma in a way that dry medical records just can't.

Snap clear photos of your injuries immediately after the accident and keep taking them as you heal. This creates a visual timeline. It shows the severity of the initial injury, the painful healing process, and any permanent scarring left behind. It’s tough for an insurance company to argue an injury was "minor" when they're looking at a photo of surgical staples or a severely bruised limb.

Your collection of evidence should paint a complete picture of your life post-accident. It’s about showing, not just telling, the adjuster how every aspect of your world has been affected.

Gather Statements from Witnesses

The people around you—your friends, family, and coworkers—see the daily impact of your injuries. Their perspective can be incredibly compelling. They can talk about the changes in your personality, your physical struggles, and all the activities you've had to give up.

Ask them to write down what they’ve noticed. A spouse can describe needing to help you with simple tasks you always handled before. A coworker might explain how your focus has suffered because of the constant pain. These outside accounts add a serious layer of credibility to your claim, backing up everything you've been saying. To get a better handle on what to do right after an incident, check out our guide on essential steps to take when accidents happen.

In the end, it all comes down to organization. Keep every bill, doctor's note, photo, and journal entry in one dedicated file. A well-documented, organized claim shows the insurance company that you're serious and prepared, which gives you major leverage during negotiations.

In pain? Call Caine.

Why You Need a Professional to Handle Your Claim

Understanding how pain and suffering is calculated is one thing. Actually putting that knowledge to work and successfully navigating a Florida personal injury claim is a different ballgame entirely. Going it alone is a huge risk, and frankly, it can cost you dearly.

Insurance adjusters are professional negotiators. Their only job is to protect their company's bottom line by paying you as little as possible. They see hundreds of claims a year and know every trick in the book to downplay your pain, shift the blame, and pressure you into a quick, lowball settlement before you realize what your case is truly worth.

This is where having a skilled attorney in your corner becomes your single most important asset.

Beyond Calculations to Case Strategy

A seasoned personal injury lawyer does a lot more than just plug numbers into a formula. We build a comprehensive legal strategy from day one, designed for one purpose: to maximize your financial recovery and hold the at-fault party completely accountable.

At CAINE LAW, our approach is proactive and aggressive:

Arguing for the Highest Multiplier: We never justaccept the insurance company’s low-ball multiplier. We gather powerful evidence—from medical expert testimony to "day-in-the-life" videos—to prove why your case justifies the highest possible figure.

Challenging Unfair Fault Allegations: Insurance adjusters love to pin a percentage of the blame on you to reduce their payout. We fight back hard, using accident reconstruction reports and witness statements to prove the other party’s full liability and protect your compensation from being unfairly slashed.

Handling All Communications: We take over every single interaction with the insurance company. This immediately stops them from using their tactics on you, like calling for a recorded statement that's just a trap to get you to make damaging admissions.

We know the insurance defense playbook inside and out because our founding attorney, Daniel Caine, spent years working for a major defense firm. That insider knowledge gives our clients a serious advantage.

Leveraging Expertise for Maximum Value

Proving the full, devastating impact of your pain and suffering requires a sophisticated presentation of evidence. We work with a network of medical specialists, vocational experts, and economists to paint a detailed, undeniable picture of your life after the accident.

A strong personal injury claim isn’t just about proving what happened; it's about proving what was lost. We translate your physical pain, emotional distress, and diminished quality of life into a powerful narrative that an insurance company—or a jury—cannot ignore.

For example, in a crash involving a commercial truck, the stakes are sky-high and the legal maneuvering is incredibly intense. Understanding why you should hire the best truck accident attorney in Florida can really highlight the level of expertise needed to win these tough fights.

Don't make the mistake of thinking a simple calculation is enough. The nuances of Florida law, the tactics of insurance carriers, and the strict rules of evidence can quickly overwhelm anyone without legal training. Trying to handle a claim yourself almost always means leaving a substantial amount of money on the table—money that is rightfully yours and crucial for your recovery.

Protect your rights. Secure the full and fair compensation you deserve. In pain? Call Caine.

At CAINE LAW, we have the experience and resources to fight for you. Don’t settle for less than your claim is worth. Contact us today for a free, no-obligation consultation to discuss your case. In pain? Call Caine.