In Pain? Call Caine

how to appeal denied insurance claim: A practical guide

5 Min read

By: Caine Law

Share

To successfully appeal a denied insurance claim, you need a game plan. It starts with understanding exactly why the insurer said no, gathering all your documents—medical records, emails, everything—and then formally challenging their decision before the deadline hits.

It sounds like a lot, I know. But it's an effort worth making.

Your Insurance Claim Was Denied. What Happens Now?

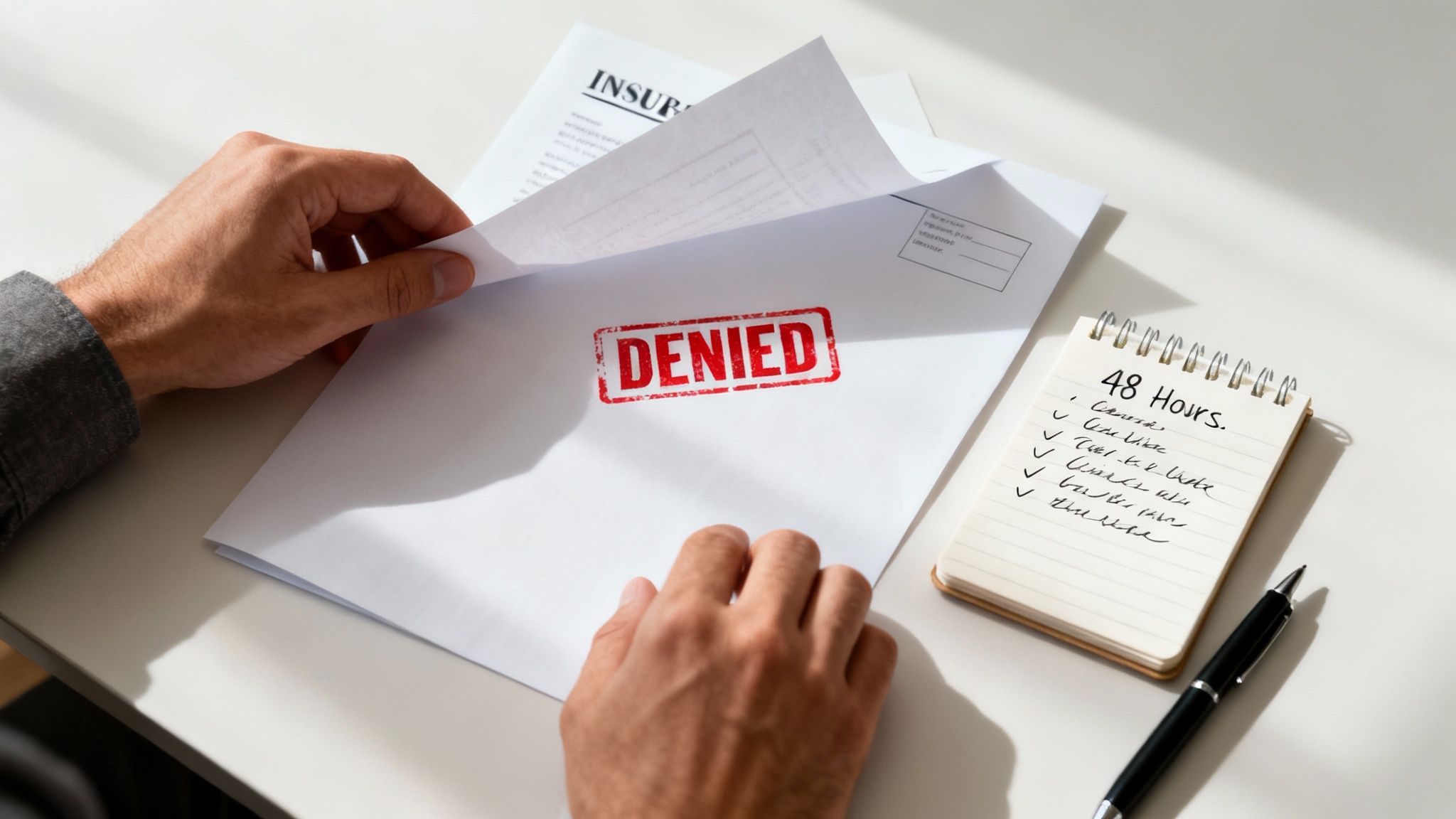

That denial letter hits hard. Seeing that bold "DENIED" stamped across the page can feel like a final, frustrating verdict, shutting the door on the money you need for your injuries, medical bills, or property damage.

But here’s what the insurance company doesn't want you to know: this is rarely the end of the road. It’s actually the beginning of a structured process where you have the power to fight back.

The trick is to replace emotion with methodical action. The two worst things you can do are panic or toss the letter aside. Instead, think of this denial as the insurance company's opening move. They've made their play, and now it's your turn to build a counter-argument backed by hard facts and solid evidence.

Why You Should Never Accept a First Denial

Here's a reality that I've seen play out time and time again: insurance companies deny a staggering number of claims, and almost no one pushes back. In the U.S. alone, about 850 million health insurance claims are denied every single year.

The shocking part? Less than 1% of those decisions are ever appealed. This is a massive missed opportunity, especially when you consider that nearly 75% of people who do appeal end up getting their claims approved.

This gap exists because most people are intimidated by the process or simply don't know where to start. Insurers are banking on that hesitation.

Your initial denial is not a final judgment on your claim’s merit; it’s often just a calculated business decision. By appealing, you force a real person to take a much closer look at the facts, which dramatically increases your chances of getting paid.

Your First 48 Hours: A Denial Response Checklist

Acting quickly and strategically in the first two days is critical. What you do right away sets the tone for your entire appeal and helps you avoid missing any deadlines.

Think of the time immediately after you get that denial letter as your "golden window" of opportunity. The checklist below outlines the first five things you need to do to get the ball rolling and build a strong foundation for your appeal.

Action Item | Why It Is Critical | Timeframe |

|---|---|---|

Read the Denial Letter Closely | Don't just skim it. Pinpoint the exact reason for the denial, the specific policy language they cite, and most importantly, find the appeal deadline. | Within 24 Hours |

Request Your Entire Claim File | Immediately send a written request for a complete copy of your claim file. It contains the adjuster’s notes, reports, and internal emails—gold for your appeal. | Within 24 Hours |

Organize All Existing Documents | Gather every single piece of paper related to your claim: medical records, police reports, photos, receipts, and all emails or letters with the insurer. | Within 48 Hours |

Start a Communication Log | From this point on, document every phone call and email. Note the date, time, who you spoke with, and what was said. This log is your proof. | Start Immediately |

Consult With an Attorney | Get a professional opinion. An experienced lawyer can review the denial and tell you if the insurer is acting in bad faith or simply made a mistake. | Within 48 Hours |

Taking these steps helps you shift from feeling like a victim to taking control. For complex cases, understanding your rights in insurance disputes can give you a significant advantage. If you're feeling overwhelmed, don't go it alone. In pain? Call Caine.

Decoding the Denial Letter to Find Your Advantage

That denial letter in your hands isn’t just bad news; it’s a treasure map. Buried under layers of dense insurance jargon and vague policy numbers is the exact reason the insurer said no. Learning to read this document is your first real step in turning their denial into your advantage.

Insurance companies count on you being too intimidated or confused to fight back. They use standardized language that feels final, but trust me, it’s often just their opening move in a negotiation. Your job is to take their argument apart, piece by piece, and find the cracks.

Think of the letter as your roadmap. It tells you exactly which documents to gather, what arguments to build, and which specific policy clauses you need to challenge head-on.

Translating Common Denial Reasons

In my experience, insurers tend to lean on a few common justifications for denying a claim. Once you understand what these phrases really mean, you can craft a targeted response instead of just firing back a generic complaint.

Let’s break down the three most frequent culprits you’ll likely see.

"Not Medically Necessary": This is a classic, especially in health insurance. The insurer isn't saying you weren't hurt; they're questioning if the specific treatment you got was the most appropriate or cost-effective option based on their internal guidelines. To fight this, you need to prove your doctor's choice was the accepted standard of care.

"Experimental or Investigational": You’ll often see this denial for newer treatments or procedures. The insurance company is basically arguing there isn't enough scientific proof that the treatment works. Your appeal will need to be armed with medical literature, peer-reviewed studies, and a strong, detailed letter from your physician explaining why this was the best—or only—option for you.

"Clerical Error or Missing Information": These are the most frustrating denials, but they're also often the easiest to fix. A simple typo in a billing code, a missing date of service, or a wrong policy number can trigger an automatic rejection. This isn't a real denial of your claim's merit; it's a system glitch that a quick phone call and resubmitted paperwork can usually solve.

Spotting the Insurer's Real Argument

It's critical to see past the boilerplate language and identify the insurer's core argument. They might cite a broad policy exclusion, but the real hang-up could be a single missing document they never even bothered to clearly request from your doctor.

The denial letter is designed to be a shield for the insurance company. Your goal is to look past the dense legal language and find the specific, actionable reason for the denial. That's the vulnerability you can exploit in your appeal.

For example, a denial for a car accident claim might vaguely mention "policy limitations." But after you read it carefully, you might discover the actual issue is a dispute over who was at fault, which they based on an incomplete police report. That single insight completely changes your strategy. Now you're not arguing about your policy; you're gathering witness statements and photos to prove liability.

How State Regulations Can Be Your Ally

Never forget that insurance is a heavily regulated industry. Florida has specific laws that dictate how insurers must behave. For one, the denial letter itself has to comply with these regulations, which often spell out how much detail they must give you and the exact timeline you have to appeal.

If their justification seems flimsy or goes against Florida statutes, that becomes a powerful point of leverage for you. For instance, if they deny a claim for a reason that Florida law explicitly deems invalid, your entire appeal can be built around their failure to comply.

Understanding these nuances is key, but I know it can be overwhelming when you're already trying to recover from an injury or loss. If you’re struggling to make sense of your denial letter or feel like the insurance company is just giving you the runaround, getting a professional opinion can make all the difference. In pain? Call Caine.

Gathering the Evidence for a Winning Appeal

An appeal isn't won with angry letters or frustrated phone calls. It's won with a mountain of undeniable proof. Once you’ve read the denial letter and understand why they said no, your next job is to gather every single document, photo, and expert opinion that proves them wrong.

This is how you turn a simple disagreement into an ironclad case they simply can't ignore. Your goal is to make it far easier for the insurance company to just pay the claim than to keep fighting you on it. Every piece of paper you provide closes another door on their excuses.

Think like a detective. You're building a case file that not only tells your story but directly attacks the specific reason they gave for the denial.

Building Your Evidence Checklist

What you need to collect obviously depends on the type of claim. A denied medical procedure requires a completely different set of proof than a lowball offer on a car wreck. Let’s break down what you should be looking for.

For Medical and Personal Injury Claims

When your health is on the line, your documentation needs to be rock-solid. Insurers often deny claims based on their own interpretation of what’s “medically necessary,” so you have to overwhelm them with expert proof to the contrary.

Your Complete Medical Records: This is non-negotiable. Get everything related to your injury or condition—doctor's notes, hospital admission and discharge papers, and all test results like X-rays, MRIs, and lab work.

A Letter of Medical Necessity: This is your secret weapon. Ask your primary treating physician to write a detailed letter explaining exactly why the treatment was necessary, how it’s the standard of care, and why cheaper alternatives wouldn’t have worked for you.

Prescription Information: A list of all medications prescribed for your condition helps paint a clear picture of the severity and ongoing nature of your medical problems.

Photos and Videos: If your injury is visible, document it. Clear photos taken right after the accident and throughout your recovery process can be incredibly powerful.

Your doctor's voice is one of the most persuasive tools in your arsenal. A well-written letter of medical necessity from a respected physician can single-handedly overturn a "not medically necessary" denial.

For Auto Accident Claims

After a car crash, the evidence needs to scream two things: who was at fault and how much the damage will cost to fix. The insurance company is hunting for any gray area they can find to reduce what they have to pay you. Don't give them one.

The Official Police Report: This is the foundation of your claim. It’s an objective account of the crash, and it often includes the officer’s initial thoughts on who was at fault.

Photos and Videos from the Scene: The pictures you take with your own phone are invaluable. Get shots of where the cars ended up, the damage to both vehicles, any skid marks on the road, and the general scene. For a full rundown, check out our guide on what to do when accidents happen provides essential steps and legal guidance.

Repair Estimates: Don't just get one. Get at least two, and preferably three, detailed estimates from body shops you trust. This proves you’ve done your homework and protects you from the insurer's lowball offer from their "preferred" (cheaper) shop.

Witness Statements: If anyone saw what happened, get their name and number. A short, signed statement from an impartial witness about what they saw can completely shut down any "he said, she said" arguments from the other driver.

How to Organize Your Evidence for Maximum Impact

Just having the right documents isn't quite enough. How you present them makes a huge difference.

Don't just jam a messy pile of papers into an envelope and hope for the best. Organize everything neatly in a binder or a digital folder. Put it all in chronological order and use clear labels.

It's also a great idea to create a cover sheet—a simple table of contents—that lists every single document you've included. This simple, professional step signals to the claims adjuster that you are organized, serious, and have built a case they need to take seriously. A clean file makes their job easier, which makes it harder for them to "accidentally" overlook a key piece of your evidence.

This careful preparation does more than just back up your appeal letter. It sends a message: you are ready and willing to fight for what you're owed. If pulling all of this together feels overwhelming, getting professional help can change the game. In pain? Call Caine.

Navigating the Appeal Process Timelines and Procedures

Once you've got your evidence lined up, you’re ready to enter the most critical phase of this fight: the formal appeal. This isn’t just a single step. It's a journey with multiple stages, strict rules, and deadlines that are completely unforgiving.

Let’s be honest—the insurance appeal process is designed to be a little confusing. But understanding its structure is your key to winning. The clock starts ticking the moment that denial letter hits your mailbox. Don't set it aside for later. Taking immediate action is the only way to protect your right to challenge their decision.

Understanding the Levels of an Insurance Appeal

The appeal journey usually has two main stages. You almost always have to complete the first one before you can move on to the second.

The Internal Appeal: This is your first official challenge. You'll send your appeal letter and all the evidence you’ve gathered straight back to the insurance company. They are required by law to have a different team—people who had nothing to do with the first denial—review your case. It’s your best shot at getting a fresh set of eyes on the facts.

The External Review: If the insurance company denies you again during the internal appeal, you often have the right to an external review. This is where an independent third party, someone with no ties to your insurer, examines your case. Here in Florida, this is typically handled by a state-regulated Independent Review Organization (IRO). Their decision is usually binding on the insurance company.

Think of it this way: the initial denial is just the opening round, not the end of the fight.

Calculating and Meeting Your Appeal Deadline

That denial letter must legally tell you the deadline for filing your appeal. This is, without a doubt, the most important piece of information in the entire document. Most of the time, you have 180 days from the day you receive the denial to file an internal appeal, but this can vary.

Don’t guess or assume. Circle that date on the letter, put it in your calendar, and set a few reminders on your phone. You have to treat this deadline as non-negotiable if you want your appeal to even be considered.

This process isn't just about throwing documents together; it's about building a solid foundation for your case, piece by piece.

Systematically gathering your records, official reports, and financial estimates is what sets you up for a timely and successful appeal.

Why Prompt Action Matters So Much

It’s easy to see why so many people just give up. The process feels overwhelming. In 2023, insurers handled about 425 million claims and denied roughly 19% of in-network claims. But the appeal rate is shockingly low—less than 1%.

Here’s the part that should get your attention: for those who do appeal, insurers overturn their own decisions in 44% of internal appeals. Persistence clearly pays off. You can dig into more of these claims industry statistics and trends to see the full picture.

These numbers tell a simple truth: insurance companies are banking on you doing nothing. By filing a well-documented appeal on time, you immediately join a small group of policyholders who are actually fighting for what they're owed.

The process is complex and the stakes are high. If you're facing a tight deadline or a complicated denial, you don't have to go it alone. An experienced attorney can take over, manage the procedures, and make sure your appeal is filed correctly and powerfully. In pain? Call Caine.

Crafting Your Appeal Letter and Making the Call

Your appeal letter isn't just a complaint—it’s your official, written argument. This is where you formally lay out your case, backed by all the evidence you’ve gathered, to build a persuasive and professional argument that the insurance company simply can't ignore.

At the same time, you'll be on the phone with them. Every call is an opportunity to push your case forward or, if you’re not careful, hit a new roadblock. Getting a handle on both written and verbal communication is absolutely critical to turning that denial around.

Writing an Appeal Letter That Gets Read

The tone you strike in your letter can make or break your appeal. Forget emotional pleas, angry rants, or threats—they don't work. What does work is a firm, factual, and professional voice. Your goal isn't just to tell your story; it's to systematically dismantle their reason for denial with cold, hard proof.

Keep your letter structured, concise, and easy for the reviewer to follow. Think of it as a roadmap for a non-lawyer. State your purpose immediately, reference their specific denial reason, and then launch into your counter-argument, pointing to the evidence you’ve included.

A powerful appeal letter doesn't just ask for a different outcome; it demonstrates precisely why the initial denial was incorrect based on the facts and the policy itself. Make their job easy by connecting the dots for them.

Key Components of a Strong Appeal Letter

To make sure your letter is taken seriously, it needs specific information in a logical order. If you miss any of these details, you risk delays or having the appeal thrown out on a technicality.

Your Identifying Information: Start with the basics: your full name, address, date of birth, and most importantly, your policy number and claim number.

A Clear Statement of Purpose: The very first paragraph should get straight to the point. State clearly that you are appealing the denial of claim number [Your Claim Number] dated [Date of Denial Letter].

Reference the Denial Reason: Call out the exact reason they gave for the denial. For example, "Your letter stated the claim was denied because the procedure was deemed 'not medically necessary.'"

Present Your Counter-Argument: This is the heart of your letter. Go point-by-point to explain why their reasoning is flawed. Reference your evidence directly, like, "As Dr. Smith’s enclosed letter of medical necessity confirms..."

State Your Desired Outcome: End with a clear statement of what you expect. For instance, "I request a full reversal of this denial and prompt payment for the claim."

Finally, sign and date the letter. Always, always send it via certified mail with a return receipt requested. This gives you undeniable proof of when they got it.

Mastering Phone Conversations with Adjusters

While the letter is your official record, phone calls are where you can get clarifications and keep things from stalling. But be warned: these calls can also be minefields if you’re unprepared. Never call without a clear goal in mind.

Before you even dial, have your claim number and a short list of specific questions ready. During the call, stay calm and professional, no matter how frustrating it gets. Take meticulous notes: the date, time, the representative's name and ID number, and a quick summary of what you discussed. This log is now part of your evidence.

Getting the letter right is half the battle. Here’s a quick guide to what works and what will sink your appeal.

Appeal Letter Best Practices

Do This | Don't Do This |

|---|---|

Be Factual and Professional | Use Emotional or Accusatory Language |

Reference Specific Evidence | Make Vague, Unsupported Statements |

Clearly State Your Policy/Claim Number | Forget to Include Key Identifiers |

Send via Certified Mail | Send via Regular Mail with No Tracking |

Stick to the Denial Reason | Bring Up Unrelated Complaints |

The appeal process demands precision and persistence. If you find the letter-writing process daunting or those calls with adjusters are going nowhere, it might be time to bring in a professional advocate. In pain? Call Caine.

When Your Appeal Gets Denied Again: What's Next?

You put together a strong appeal. You laid out the facts, attached all your evidence, and made a compelling case. And then... you get another denial letter.

It’s an incredibly frustrating moment, but it's not the end of the road. It’s a turning point. When your best efforts are met with a brick wall, it's often a sign you've pushed the internal process as far as it can go on your own.

Recognizing when to escalate isn’t admitting defeat—it's getting strategic. The insurance company is no longer the only decision-maker. It's time to bring in someone else.

The Power of an External Review

If your internal appeal for a health insurance claim is denied, you usually have the right to an external review. This is a game-changer.

Your case gets handed over to an Independent Review Organization (IRO), which is a neutral third party that has zero connection to your insurance company. Their only job is to look at the facts of your case objectively and make a final, binding decision.

Think of it as bringing in an impartial referee. The insurance company's financial motives are off the table. The decision is based purely on medical necessity and the black-and-white terms of your policy. It’s a powerful step that can level the playing field in a big way.

Red Flags: When It’s Time to Call an Attorney

Sometimes, an insurer's behavior makes it painfully obvious they have no intention of paying what they owe you. Their conduct can even cross the line into bad faith—a serious legal issue where an insurance company fails to uphold its basic duties to you, the policyholder.

You should seriously consider getting a lawyer involved if you see these signs:

Endless Delays: They’re constantly dragging their feet, blowing past their own deadlines, or conveniently "losing" the paperwork you just sent them.

Moving the Goalposts: They deny your claim for one reason, and as soon as you prove them wrong, they just invent a new one out of thin air.

Vague Denials: You get a denial letter with no specific, written explanation tied directly to your policy language.

The Lowball Offer: They make a settlement offer that is so insultingly low it doesn't even come close to covering your actual losses.

The moment an insurance company gets a letter from an experienced attorney, the whole dynamic shifts. Suddenly, phone calls get returned. Adjusters who were ghosting you are now ready to have a serious conversation.

Hiring a lawyer sends a powerful message: you won't be bullied, and you won't be ignored. It forces the insurer to weigh the cost of a fair settlement against the much bigger risk and expense of a lawsuit they might lose. An attorney who handles personal injury claims knows how to build leverage and fight for the full amount you're actually owed.

If you’ve hit a wall and your appeal has been denied, don’t keep banging your head against it alone. It’s time to escalate. In pain? Call Caine.

Common Questions We Hear About Insurance Appeals

When you're staring down a denial letter, a hundred questions probably pop into your head. It’s a confusing and frustrating process, but you're not the first person to go through it. Here are some of the most common questions we get from clients just like you.

How Long Does This Whole Appeal Thing Take?

There’s no single answer, but you can plan on it taking a while. For a standard internal appeal—where you're just asking the insurance company to take a second look—you can expect it to take anywhere from 30 to 60 days.

If they shut you down again and you have to take it to an external, independent reviewer, that can tack on another 45 to 60 days. It’s a marathon, not a sprint. Always double-check your policy documents and Florida's insurance regulations to know the specific deadlines you're up against.

My Health Insurance Was Denied for a "Pre-Existing Condition." Can I Fight That?

Yes, and you absolutely should. Under the Affordable Care Act (ACA), it is flat-out illegal for health insurance companies to deny claims or coverage based on pre-existing conditions.

If you see that phrase on your denial letter, it’s a massive red flag. That denial isn't just wrong—it’s against the law. Make that the core of your appeal. For other types of insurance, it will come down to the fine print in your policy, but it's always worth pushing back.

What if I Missed the Deadline to Appeal?

Missing a deadline is a big deal, and insurance companies are notoriously strict about them. They’ll often use it as an easy reason to close your case for good.

But life happens. If you had a legitimate, unavoidable reason for missing the cutoff—like a serious medical emergency or hospitalization—you might have a shot. You need to contact the insurer in writing immediately, explain what happened, and ask for an exception. If they still refuse to budge, it’s time to talk to an attorney.

When you've given it your all and the insurance company still won't do the right thing, that's where CAINE LAW comes in. We’re used to their games and know how to build a case they can't ignore. Schedule your free consultation today. In pain? Call Caine.