In Pain? Call Caine

Do Motorcycles Need Insurance in Florida

5 Min read

By: Caine Law

Share

When someone asks, "do motorcycles need insurance in Florida," the answer isn't as clear-cut as you might think. On one hand, you can legally register and ride your motorcycle without carrying an insurance policy. But this freedom comes with a huge catch, thanks to the state's Financial Responsibility Law.

That law makes insurance an absolute must-have the second you cause an accident.

Why Florida Motorcycle Insurance Is So Unique

Florida’s approach to motorcycle insurance is unlike anywhere else in the country. It’s a strange setup that often gives riders a false sense of security, leaving them completely exposed to massive financial risk when they hit the road unprotected.

The real issue is the gap between what's required before you ride versus the consequences after a crash. The state doesn't force you to buy insurance up front, but it absolutely holds you financially accountable for any damage or injuries you cause.

The Financial Responsibility Law Explained

Think of this law as a "delayed" insurance mandate. It doesn't come into play when you're at the DMV getting your plates. Instead, it kicks in with full force right after a crash.

If you’re found at fault for an accident that hurts someone or damages their property, the law will then require you to buy and maintain specific liability insurance for years. It creates a high-stakes gamble where one mistake can trap you in a cycle of severe, long-lasting financial penalties.

Riding without coverage is truly betting against the odds, especially when you consider Florida's high accident rates and the number of uninsured drivers already out there.

Understanding Florida's distinct motorcycle insurance laws is the first step toward safeguarding yourself. The law allows you to ride without initial proof of insurance, but it demands financial accountability after an at-fault accident, making subsequent coverage mandatory.

In a nutshell, Florida stands alone as the only state in the U.S. where motorcycle insurance isn't legally mandatory for every single rider. While 49 other states require proof of insurance just to register a bike, Florida lets you ride without it—unless you've caused an accident within the last three years. You can discover more insights about these unique state regulations and how they really impact riders.

To make this a bit clearer, here's a quick breakdown of when you do and don't need insurance as a Florida rider.

Florida Motorcycle Insurance At a Glance

The table below summarizes the key situations a motorcyclist might face and whether insurance is legally required.

Scenario | Insurance Required? | Key Consideration |

|---|---|---|

Registering a new or used motorcycle | No | You can legally register your bike without showing proof of insurance. |

Riding daily without an accident history | No | As long as your record is clean, you are not legally required to carry insurance. |

Causing an accident with injuries/damage | Yes | The Financial Responsibility Law is triggered, and you must purchase and maintain coverage for 3 years. |

Getting a motorcycle license or endorsement | No | Proof of insurance is not a requirement to get your motorcycle endorsement. |

Financing a motorcycle | Yes | While the state doesn't require it, your lender almost certainly will to protect their investment. |

As you can see, the "optional" nature of Florida's law is really just a loophole with serious consequences. The safest bet is always to carry proper insurance before anything happens.

Navigating Florida's Financial Responsibility Law

Think of Florida's Financial Responsibility Law less like a rule you have to follow before you start your engine, and more like a safety net you have to prove you had after you’ve already fallen. It’s this unique setup that makes the question “do motorcycles need insurance in Florida?” so tricky. Instead of forcing every rider to carry a policy from day one, the state uses a system of post-accident accountability.

As long as you’re riding without incident, the law stays quiet. But the second you’re found at fault for an accident that hurts someone or damages their property, it roars to life. That freedom to ride without a policy? It's gone. In its place are strict, non-negotiable legal demands.

When the Law Kicks In

Certain triggers bring the full weight of this law down on a rider, and it's not a gentle slap on the wrist. You aren't just looking at a potential lawsuit from the person you injured; you're also facing direct penalties from the State of Florida itself. Once the law is triggered, it's on you to prove you can cover the damages you caused.

This is the moment insurance becomes mandatory. If you can’t show proof of financial responsibility after a crash, the state can—and will—suspend your driving privileges, your motorcycle registration, and your license plate.

The Minimum Coverage You Will Be Forced to Carry

If you cause an accident and don't have insurance, Florida law spells out exactly what you have to do to get your license back. You’ll be required to buy liability coverage and keep it for three years straight. This isn't a suggestion; it's a condition of being allowed back on the road.

The post-accident coverage you’ll be forced to carry includes:

$10,000 in Bodily Injury Liability per person.

$20,000 in Bodily Injury Liability per accident.

$10,000 in Property Damage Liability per accident.

This is often called "10/20/10" coverage, and it's the absolute bare minimum the state will accept after you've caused a wreck.

The system essentially turns riding without insurance into a high-stakes gamble. You're betting you'll never cause an accident. The financial and legal consequences of losing that bet are severe and can follow you for years.

There are a couple of other ways to satisfy the law, like getting a self-insurance certificate or posting a massive bond with the state. But for the vast majority of riders, buying a standard liability policy is the only practical way to comply.

Ultimately, this reactive system puts all the risk squarely on the uninsured rider's shoulders. The law is there to make sure victims of negligence get compensated, and it will hold you personally accountable if you haven't planned ahead. If you've been in an accident and are now facing these complicated requirements, getting legal guidance is critical. In pain? Call Caine.

Choosing the Right Coverage for Florida Riders

Florida's motorcycle laws can be a little misleading. While you can technically get on the road without buying insurance first, the real question isn't what the state lets you get away with—it's what you actually need to protect yourself. Just meeting the bare minimum requirements after a crash is a recipe for financial disaster.

Think of it like buying riding gear. You don't wear a quality helmet and jacket just to follow a rule; you do it to protect yourself from serious harm. Your insurance policy deserves that same level of serious consideration.

At its core, a solid policy starts with liability coverage. This is what pays for the other person’s damages when you’re the one who caused the accident. It’s split into two crucial parts:

Bodily Injury (BI) Liability: This covers the medical bills, lost income, and pain and suffering for anyone you injure.

Property Damage (PD) Liability: This pays to fix or replace the other person's bike, car, or any other property you might have damaged, like a fence or guardrail.

Without this fundamental coverage, you're on the hook personally for every single dollar of the other person's losses. Those costs can easily climb into the tens, or even hundreds, of thousands of dollars after a serious wreck.

Your Most Important Shield: Uninsured Motorist Coverage

If there's one piece of coverage every single rider in Florida needs to have, it’s Uninsured/Underinsured Motorist (UM/UIM) coverage. Why? Because Florida has one of the highest rates of uninsured drivers in the entire country. More than 20% of drivers on our roads have zero insurance.

That means there’s a one-in-five chance the driver who hits you won’t have a dime of insurance to pay for your medical bills.

UM/UIM coverage is your safety net. It steps in and acts like the at-fault driver's insurance when they don't have any—or don't have enough—to cover your injuries. It pays for your medical care, lost wages, and suffering.

Imagine getting blindsided by a driver with no insurance and no money to their name. Without UM coverage, you're left holding the bag for your own massive medical bills and lost paychecks. It is, without a doubt, your single best defense against financial ruin.

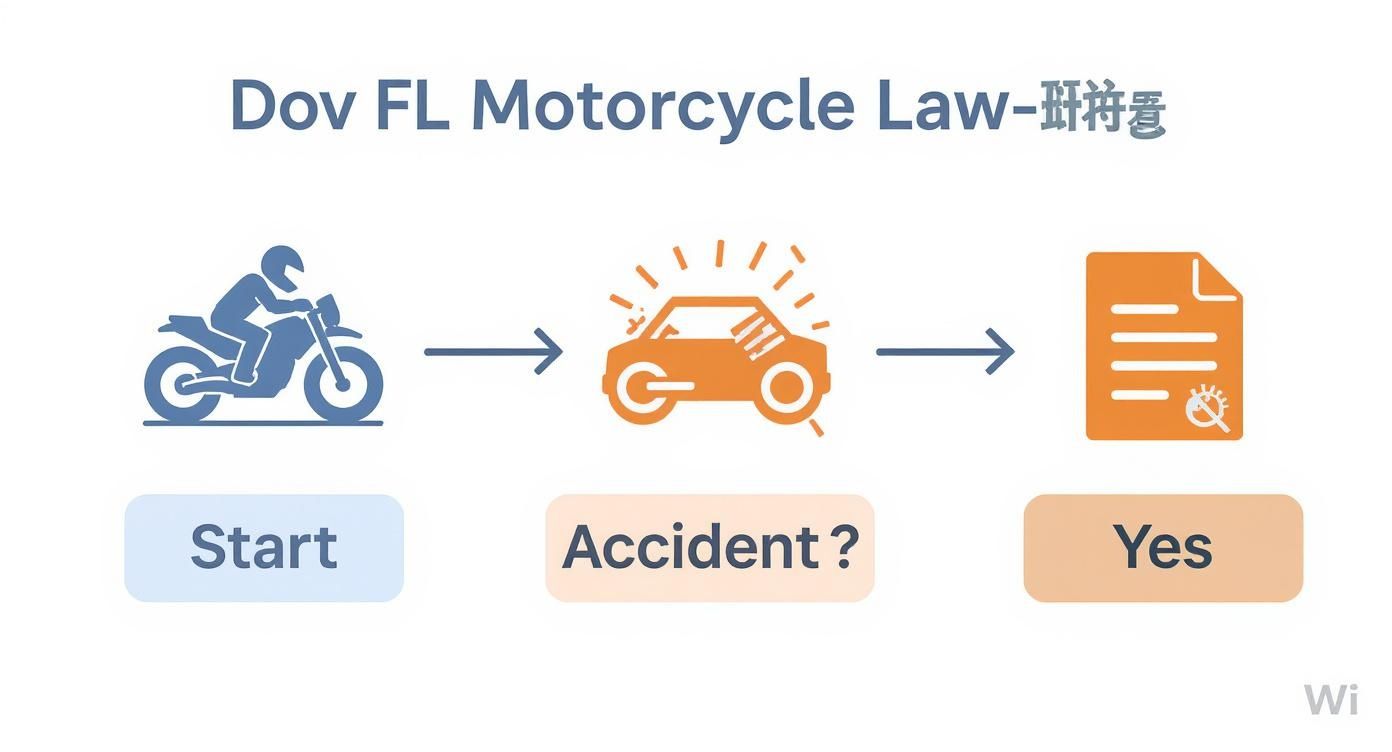

This decision tree shows how Florida law only forces financial responsibility after an accident has already happened.

As the flowchart makes clear, the legal trigger for insurance is an at-fault crash, which is why having proactive coverage beforehand is so essential.

Filling the Gaps: PIP and MedPay

Here’s a critical point that trips up a lot of riders: Personal Injury Protection (PIP) from your car insurance policy does not cover you on your motorcycle in Florida. That's a huge misunderstanding. PIP is designed only for four-wheeled vehicles, which leaves a massive gap in your protection when you're on two wheels.

This is exactly where Medical Payments (MedPay) coverage becomes so important. MedPay is an optional add-on for your motorcycle policy that helps pay for your medical expenses up to a set limit, no matter who was at fault for the crash.

It gives you immediate access to funds for things like the ambulance ride, ER visit, and health insurance co-pays without having to wait for the insurance companies to fight over who’s to blame. If you’ve been injured and aren't sure how you're going to cover your bills, we can help. In pain? Call Caine.

Alright, let's talk about what really matters to most riders: the bottom line. It's one thing to navigate the legal requirements, but the question on everyone's mind is, "What's this actually going to cost me?"

The price of a good motorcycle policy is a small, predictable monthly expense. Compare that to the unpredictable, often life-shattering costs of a single accident when you're uninsured, and the choice becomes pretty clear.

Insurance isn't a one-size-fits-all deal. The premium you pay is a direct reflection of the risk the insurance company takes on. They look at a whole host of factors to figure out how likely you are to make a claim, which means the final price tag is uniquely yours.

Key Factors That Drive Your Insurance Rate

Insurers weigh several variables when they put together your quote. While you can't change some of them, others give you a real opportunity to find some savings.

Your Riding History: A clean record is your best friend here. Tickets, at-fault accidents, or even just getting your motorcycle endorsement will push your rates up. Experience and a history of safe riding will do the opposite.

Age and Location: Younger, less-experienced riders are seen as a higher risk, so they almost always pay more. Where you park your bike at night also makes a huge difference. Densely populated urban areas with more traffic and higher theft rates mean pricier insurance.

The Motorcycle Itself: This one's a biggie. A high-performance sportbike is going to cost a lot more to insure than a standard cruiser. It comes down to speed, replacement cost, and how often they get stolen.

Your Coverage Choices: This is where you have the most control. A bare-bones, liability-only policy will be the cheapest option. But adding comprehensive, collision, and high-limit Uninsured Motorist coverage will increase the premium—while also giving you far better protection.

Think of your insurance premium not as just another bill, but as an investment in your financial future. It's a fixed cost that shields you from the wild, unpredictable, and potentially devastating expenses that follow a crash.

The cost of motorcycle insurance in Florida is all over the map, but on average, full coverage runs about $46 a month—which is quite a bit higher than the national average. If you're riding in a busy city like Miami, you could see premiums climb to $70 a month. Head to a smaller city like Deltona, and that number might drop closer to $36. You can discover more insights about motorcycle insurance costs in Florida to get a better sense of how your location plays a part.

At the end of the day, the few hundred dollars you might spend on a solid policy each year is just a drop in the bucket compared to the medical bills, lost wages, and legal fees that can pile up after a serious wreck.

If an accident has already left you staring down a mountain of debt, help is available. In pain? Call Caine.

Consequences of an Accident Without Insurance

Riding without insurance in Florida is a high-stakes gamble. While the state lets you register your bike without a policy, that all changes the second you cause an accident. If you're uninsured and at fault, the consequences aren't just a slap on the wrist—they're severe, immediate, and designed to get you off the road.

The first thing that happens? The state takes swift action. If you can’t prove you have the financial means to cover the damage, officials will immediately suspend your driver's license and your motorcycle endorsement.

At the same time, they'll also suspend your motorcycle registration and license plate. This isn't a temporary hold; your bike is legally barred from all public roads until you navigate a long and expensive process to get back in good standing.

The High Cost of Getting Back on the Road

Getting your license back isn't as simple as paying a fine. To prove you're no longer a risk, Florida law forces you to take some very specific—and very costly—steps. The biggest hurdle is purchasing what’s known as an SR-22 filing.

An SR-22 isn't actually insurance. It’s a certificate your insurance company files with the state to prove you have the required liability coverage. Here’s the catch: you must maintain this SR-22 coverage without a single break for three full years. If you let it lapse for even a day, your license gets suspended again, and you have to start the entire process over from square one.

The penalties for an uninsured, at-fault accident aren't a warning—they are a complete shutdown of your ability to legally ride. The money you thought you were saving on premiums gets wiped out instantly by long-term financial burdens and legal nightmares.

Beyond the state penalties, you are still personally on the hook for every dollar of damage you caused. The other driver and their passengers can sue you directly, putting your personal assets—your home, your savings, your future wages—at risk. A single judgment against you can dig a financial hole that takes years, or even decades, to climb out of. The aftermath of serious auto and motorcycle accidents is incredibly complex, which is why having experienced legal guidance is so critical.

The state’s message is loud and clear: you can start riding without insurance, but the consequences are designed to be punitive. The financial pain of an SR-22 and a lawsuit will always cost more than a standard policy. If you find yourself in this difficult situation, don’t face it alone. In pain? Call Caine.

What to Do Immediately After a Motorcycle Accident

In the chaotic moments after a crash, adrenaline floods your system, making it nearly impossible to think clearly. But the steps you take right then and there are absolutely critical—for your health, your safety, and any future insurance claim or legal action.

First thing’s first: check yourself for injuries. If you can move, get to a safe spot away from traffic. Then, call 911 right away to report the accident and get medics on the way. Even if you feel fine, make the call. Some serious injuries, like internal bleeding or concussions, don't show symptoms until much later.

Document the Scene and Gather Information

While you wait for help to arrive, switch into investigator mode. Use your phone to take as many pictures and videos of the scene as you can. Get shots from every conceivable angle. You’ll want to capture the final positions of the vehicles, all the damage to your bike and the other car, the road conditions, nearby traffic signs, and any skid marks on the pavement.

Next, you need to exchange information with the other driver. Don't argue or get emotional; just politely ask for the essentials:

Their full name and contact information

Driver’s license number

Insurance company and policy number

Vehicle license plate number

Make, model, and color of their vehicle

If anyone saw what happened, get their names and phone numbers, too. An objective witness can be a game-changer for your case down the road.

A common—and very costly—mistake is admitting fault at the scene. Never say "it was my fault" or even apologize. Stick to the facts when you talk to the other driver and the police. Figuring out who is legally liable is often more complicated than it seems.

Protecting Your Legal Rights

After you’ve been checked out by a medical professional, your very next call should be to an experienced motorcycle accident attorney. It won't take long for the other driver's insurance adjuster to contact you, hoping to get a recorded statement. Their goal is almost always to find a way to minimize their company's payout.

Talking to a lawyer first is the best way to protect your rights. For a more detailed guide, check out our post on the essential steps and legal guidance after an accident happens.

A skilled attorney will handle all the communications with the insurance companies, launch a proper investigation into the crash, and fight for the full and fair compensation you deserve for your injuries and damages. If you've been hurt, don't try to navigate the aftermath on your own. In pain? Call Caine.

A Few Common Questions About Florida Motorcycle Insurance

To wrap things up, let's clear up some of the most common points of confusion riders face. Florida's laws can be a bit tricky, so it's normal to have questions about how it all works in the real world.

Does My Car Insurance PIP Cover My Motorcycle Injuries?

This is a big one, and the answer is a hard no. Your Personal Injury Protection (PIP) policy, which is mandatory for your four-wheeled vehicles, legally does not apply to motorcycles in Florida.

If you get hurt on your bike, your car's PIP won't touch your medical bills. You'll have to lean on your personal health insurance, any MedPay coverage you bought for your bike, or go after the at-fault driver's liability policy.

What Is an SR-22 and When Do I Need It?

An SR-22 isn't actually insurance. Think of it more like a "proof of insurance" certificate that your insurer files directly with the state on your behalf. It’s a way of telling the government you’re meeting your legal financial responsibility obligations.

You'll be required to get an SR-22 if you cause a motorcycle wreck while riding uninsured. It becomes a non-negotiable condition to get your license back, and you have to keep it active for three years straight without any lapses.

Florida has a unique way of linking your helmet to your insurance. If you're over 21, the choice to ride without a helmet is legally tied to carrying proof of at least $10,000 in medical benefits coverage. Your gear and your policy are connected.

Can I Legally Ride Without a Helmet in Florida?

Yes, you can—but you have to check two boxes first. To ride legally without a helmet, you must be over 21 years old AND carry an insurance policy that provides at least $10,000 in medical benefits. This coverage can come from a MedPay add-on to your motorcycle policy or even a separate health insurance plan.

If you don't meet both of those requirements, the law says you must wear a helmet. It's easy to see how these kinds of rules can create complicated insurance disputes when a crash happens, which is why knowing your rights is so important.

If you're trying to pick up the pieces after a motorcycle accident, you shouldn't have to fight the insurance companies by yourself. At CAINE LAW, our job is to fight for the compensation you deserve. In pain? Call Caine. Get a free case evaluation today.