In Pain? Call Caine

Average Wrongful Death Settlement: What to Expect

5 Min read

By: Caine Law

Share

Losing someone you love is a devastating experience. When that loss is caused by someone else's carelessness, the pain is often compounded by a desperate search for answers. One of the first questions families ask is, "What is the average wrongful death settlement?"

It’s a completely understandable question. But the hard truth is, there's no such thing. Every case is built on a unique life and an irreplaceable loss, making a single "average" a misleading and often unhelpful number.

Why a Single Average Wrongful Death Settlement Is a Myth

In the midst of grief, you're looking for some kind of certainty, a benchmark to hold onto. The idea of an "average" settlement seems to offer that, but it almost always creates false hope or unnecessary anxiety. Trying to slap a generic number on your family's profound loss is like trying to price a priceless family heirloom—it just doesn't work.

Your case isn't just another statistic to be plugged into a formula. It's a deeply personal story, and the legal process is designed to honor that story. The value of a wrongful death claim isn’t pulled from some master list; it’s carefully constructed from the ground up, piece by piece, based on the specific details of your loved one's life and the hole their absence leaves behind.

Building Your Claim from the Ground Up

The best way to think about a wrongful death settlement is to imagine building a custom home, not buying a cookie-cutter model from a big development. Every room, every material, and every finish is chosen specifically for the family who will live there. In a legal sense, the "building materials" are the unique factors of your case.

Some of the foundational elements we look at include:

The Financial Foundation: These are the tangible, calculable losses. It covers the income your loved one would have earned over their lifetime, the medical bills from their final injury, and the funeral and burial expenses.

The Human Impact: This is the intangible, yet most profound, part of the loss. It’s impossible to put a true price on the loss of companionship, a parent’s guidance, a spouse's support, or the deep emotional pain your family is going through. But the law requires us to do just that.

The Specifics of the Incident: How strong is the evidence? How reckless was the other party? How much insurance coverage is available? These practical realities play a massive role in shaping the final outcome.

A wrongful death settlement isn't about finding an average number. It’s about meticulously documenting a unique life and the immense void it leaves behind to ensure the compensation truly reflects the full scope of a family’s loss.

A settlement's value is determined by a combination of many specific, personal factors. Here's a quick look at what we mean.

Primary Factors That Determine a Settlement's Value

Factor Category | Examples of What's Considered |

|---|---|

Financial Contributions | The deceased's income, earning potential, benefits, and retirement savings. |

Non-Economic Losses | Loss of companionship, parental guidance, spousal support, and emotional pain. |

Dependents & Survivors | The number of dependents, their ages, and their relationship to the deceased. |

Case-Specific Details | The clarity of fault, the degree of negligence, and the quality of evidence. |

Medical & Final Expenses | All medical bills leading up to the death, plus funeral and burial costs. |

Insurance Policy Limits | The maximum amount of compensation available from the at-fault party's insurance. |

As you can see, each of these elements is unique to your family. This is why a generic "average" simply doesn't apply.

Shifting Your Focus

Instead of getting hung up on a misleading average, the most helpful thing you can do is understand the building blocks of a just settlement. When you recognize that your claim's value is a combination of measurable financial losses and the profound, personal impact on your family, you can start to see a clearer path forward.

This shift in perspective helps you focus on what really matters: telling your loved one's story to achieve a resolution that honors their memory and provides the financial stability your family needs to begin to heal.

Understanding these core concepts is the first step. The next is to explore exactly how attorneys and experts calculate these different damages to build a powerful case. If you feel lost in this process, remember you don't have to navigate it alone. In pain? Call Caine.

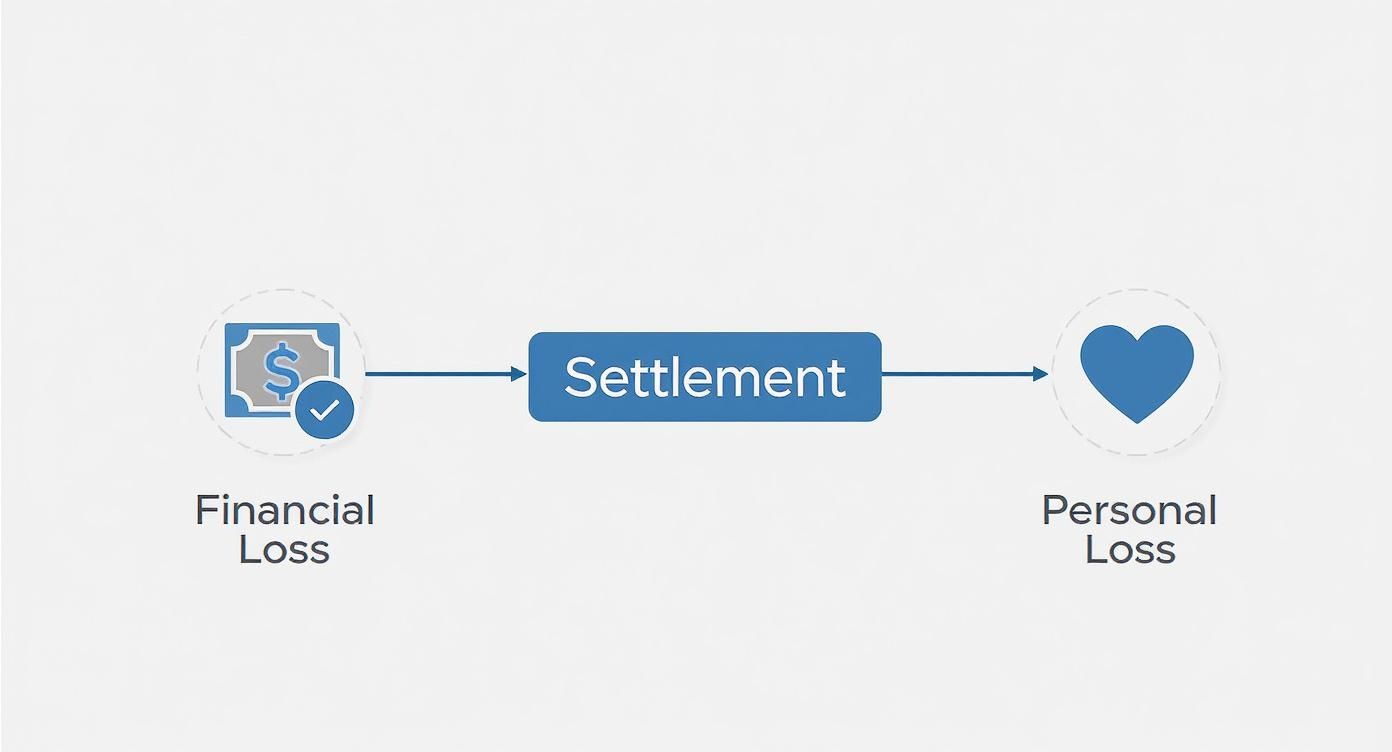

How the Value of a Wrongful Death Claim Is Calculated

Trying to put a number on the loss of a loved one feels impossible. How do you translate a lifetime of memories, support, and love into a dollar amount? While no amount of money can ever replace who you've lost, the legal process aims to provide a full and fair picture of what your family has endured.

This process involves a detailed calculation of two distinct categories of damages: economic and non-economic. Think of it like this: one part of the calculation uses receipts, pay stubs, and financial projections, while the other captures the irreplaceable human value your loved one brought to your lives.

This infographic breaks down these two core components of a settlement—the tangible financial losses and the profound personal ones.

As you can see, a true valuation has to account for both sides of the coin. It’s about recognizing the measurable economic impact and the deep, intangible void left behind.

The Foundation: Economic Damages

Economic damages are the tangible, calculable financial losses your family has suffered and will continue to suffer. These are the numbers we can prove with documents, expert analysis, and straightforward math, forming the financial bedrock of the claim.

These damages almost always include:

Lost Future Income and Benefits: This is often the single largest part of the claim. We calculate the total wages, bonuses, health insurance coverage, and retirement contributions the deceased would have earned over their expected working life.

Medical Expenses Incurred: Any medical bills from the final injury or illness—ambulance rides, hospital stays, surgeries, and other treatments—are tallied up and included.

Funeral and Burial Costs: This covers the reasonable expenses for a funeral service, burial, or cremation.

Loss of Services: This quantifies the value of all the things the deceased did for the family, like childcare, home repairs, managing finances, or caring for an elderly parent.

For example, imagine we're calculating the lost income for a 40-year-old engineer who was on a steady career path. An economist would project their earnings all the way to a planned retirement age of 65, factoring in likely raises, inflation, and promotions to arrive at a concrete figure. This part of the claim is designed to restore the financial stability your family has lost.

Valuing the Invaluable: Non-Economic Damages

While economic damages are about spreadsheets and projections, non-economic damages confront the profound human cost of your loss. This is where we seek compensation for the immense suffering and the personal voids that have no price tag. It's never easy to quantify, but it's a critical part of achieving justice.

Non-economic damages acknowledge a fundamental truth: the greatest losses are not financial. They are the empty chair at the dinner table, the lost guidance, and the absence of a cherished companion.

Here, the law attempts to place a monetary value on the emotional devastation your family is going through.

Common examples of non-economic damages include:

Loss of Companionship and Consortium: This applies to the loss of love, affection, and emotional support from a spouse or partner.

Loss of Parental Guidance: This compensates minor children for losing a parent's nurturing, instruction, and guidance as they grow up.

Mental Pain and Suffering: This addresses the grief, sorrow, and emotional anguish endured by the surviving family members.

There is no simple calculator for this kind of pain. An experienced attorney must build a powerful and compelling narrative that shows the true depth of your family's loss to a judge, jury, or insurance company. This is why the average wrongful death settlement in the United States typically falls somewhere between $500,000 and several million dollars, depending heavily on these unique factors.

States that allow for significant non-economic damages, like Alabama, often see settlements exceed $1 million. In contrast, states with strict caps on these damages might see lower amounts.

Calculating these damages is a core element of any personal injury claim. It requires a sensitive but methodical approach to ensure the final number truly reflects the full scope of what your family has endured. You do not have to face this overwhelming task alone. In pain? Call Caine.

Understanding Wrongful Death Claims in Florida

Navigating a wrongful death claim isn’t just about calculating a number; it’s about understanding the specific legal battlefield in the state where the tragedy happened. Florida has its own set of rules that dictate who can file a claim, what they can recover, and how long they have to act. Getting these state-specific guidelines right is the first, most critical step in protecting your family’s rights.

In Florida, the law makes a sharp distinction between two kinds of claims that come up after a fatal incident: a Wrongful Death Claim and a Survival Action. They are often pursued together, but they are built to compensate for two very different types of loss.

Wrongful Death Claim vs. Survival Action

A Wrongful Death Claim is brought by the surviving family members (or the estate, acting for them) to compensate for the losses they are now suffering. This claim is all about the survivors' pain and the massive financial and emotional hole left by their loved one's death.

A Survival Action, on the other hand, is filed by the deceased person’s estate to recover damages that the victim could have claimed themselves if they had lived. This is about compensating for the pain, suffering, and financial losses the person endured from the moment they were injured until they passed away.

Here’s a simple way to think about it:

Wrongful Death Claim: Compensates the family for their future without their loved one.

Survival Action: Compensates the estate for the suffering the deceased endured before death.

Pursuing both claims is the only way for a family to seek justice for the full, heartbreaking scope of the tragedy—both the victim's final suffering and the family's ongoing loss.

Who Can File a Wrongful Death Lawsuit in Florida

Not just anyone can walk into court and file a wrongful death lawsuit in Florida. The law is extremely specific. The action must be filed by the personal representative of the deceased person’s estate.

This representative then files the claim on behalf of specific family members, legally known as "survivors." Under Florida law, these are typically:

The surviving spouse

Minor children (and sometimes adult children, depending on the situation)

The deceased's parents

Any money recovered is then distributed among these survivors based on the individual losses each person has suffered. This structure ensures the compensation goes directly to those most devastated by the loss.

The Countdown Clock: Florida’s Statute of Limitations

One of the most unforgiving rules in any wrongful death case is the statute of limitations. This is a hard deadline for filing a lawsuit.

In Florida, you generally have just two years from the date of death to file a wrongful death lawsuit. If you miss this deadline, the court will almost certainly throw your case out forever, no matter how strong it is.

Two years might sound like a long time, but it disappears in a flash when a family is grieving. In that time, your attorney has to launch a full investigation, gather mountains of evidence, hire experts, and prepare all the complex legal paperwork.

Because this deadline is so final, it is absolutely essential to speak with an attorney as soon as you possibly can. Waiting too long could destroy your family's one and only chance to hold the responsible party accountable and get the financial stability you need to start rebuilding. The legal system is confusing and harsh, but you don't have to face it alone.

If you are dealing with the aftermath of a tragic loss and feel lost in the maze of Florida law, we are here to bring clarity and direction. In pain? Call Caine.

Real-World Scenarios and Settlement Examples

All the legal talk about damages and liability factors can feel a bit abstract. So, let's ground this conversation in some real-world situations. I find that walking through a few anonymized scenarios helps families understand how all these pieces fit together and why a single "average wrongful death settlement" number just doesn't exist.

While you can never put a price on a human life, a settlement has to translate that unimaginable loss into a number. Let’s look at how different circumstances can lead to drastically different outcomes.

Scenario 1: The High-Earning Professional

Picture a 45-year-old surgeon, a married mother of three young children, killed when a commercial truck runs a red light. The fault is clear. She was earning $450,000 per year and was on a partner track at her practice. Her family's claim is going to be built on several powerful, high-value pillars.

First, an economic expert will project her lost lifetime earnings, factoring in expected raises, bonuses, and benefits. That figure alone could easily top $10 million. But that's just the start. The non-economic damages—the human loss—are immense. A jury would have to consider the profound loss of companionship for her husband. Even more critically, they’d evaluate the loss of parental guidance, love, and support for her three young children—a loss they will carry for the rest of their lives.

Scenario 2: The Retired Grandparent

Now, let's consider a completely different situation. A 78-year-old retired grandfather dies from injuries after a slip-and-fall at a grocery store with a wet, unmarked floor. He lived on a modest pension and Social Security, and his children are all independent adults. The grief his family feels is just as real and just as deep, but the legal valuation of the claim looks entirely different.

The economic damages here are limited. They would mostly cover funeral expenses and any medical bills from the fall, since there's no future income to replace. The non-economic damages would focus on the loss of companionship for his wife and the loss of his presence in his adult children's lives. While still a significant claim, the total settlement would be a fraction of the surgeon's case simply because the calculable economic losses are so much lower.

These two examples show you how age, income, and who is left behind create completely different settlement landscapes. The emotional loss is equal, but the financial calculations required by law force a starkly different result.

A Sample Settlement Calculation

Let's break down how a settlement could be structured for a 35-year-old construction worker, a married father of two, who was killed on the job due to a faulty piece of equipment.

Lost Future Income: He was earning $70,000 per year. An economist projects his earnings over a 30-year work-life expectancy, accounting for modest raises. This results in an estimated economic loss of $2.1 million.

Loss of Benefits: The value of his health insurance and 401(k) match is calculated over that same period, adding another $300,000.

Loss of Services: Think about all the things he did around the house—repairs, yard work, car maintenance. The value of these contributions is estimated at $15,000 per year, totaling $450,000 over 30 years.

Final Expenses: Medical bills from the accident and funeral costs come to $40,000.

Non-Economic Damages: This is where the human story comes in. An attorney would argue for compensation for the spouse's loss of companionship and the children's devastating loss of their father's guidance. A jury might award $1.5 million for the wife and $1 million for each child, totaling $3.5 million.

Total Potential Case Value: $6,390,000

This figure becomes the foundation for negotiations. The final settlement will always be shaped by factors like insurance policy limits and whether the victim shared any fault in the accident.

Wrongful death awards can vary wildly. We've seen a $50 million settlement for a death caused by a failed medical device and even a $310 million verdict in a Florida theme park accident. These cases show the incredible potential when extreme negligence is involved.

Building a strong case starts from day one. Understanding the immediate steps to take after an incident is critical. For more on this, check out our guide on what to do when accidents happen for essential legal guidance. These real examples and calculations peel back the curtain, showing you exactly how a claim is built, piece by piece.

If you are facing this heartbreaking reality, you need someone who will meticulously build your family’s case. In pain? Call Caine.

Navigating the Settlement Process and Insurance Tactics

Knowing what your family’s claim might be worth is just the first step. Actually getting that fair compensation is a journey, one that requires a strategic approach, patience, and a clear-eyed view of how insurance companies really work. They have a playbook they follow every time, and the key to protecting your family is knowing their next move before they make it.

There's a definite path a wrongful death claim follows. It starts with a deep-dive investigation and ends with a resolution—either through a negotiated settlement or, if we have to, a fight in the courtroom.

The Typical Stages of a Wrongful Death Claim

Think of the settlement process as building an undeniable case, piece by piece, to get justice for your family. Each stage has a purpose, from digging up the facts to formally demanding accountability from the people responsible.

Here’s how a wrongful death claim usually unfolds:

Investigation and Evidence Gathering: We hit the ground running. Our team launches an exhaustive investigation, gathering everything from police reports and medical records to witness interviews and expert analysis. The goal is simple: prove exactly who was at fault and document every single loss your family has suffered.

Filing the Claim: This is the official starting gun. A formal claim is filed with the at-fault party’s insurance company, putting them on notice that we are coming.

The Demand Package: This is where we lay our cards on the table. Your lawyer assembles a powerful, comprehensive demand package. It’s a detailed document that spells out our legal arguments, presents the mountain of evidence we’ve gathered, and breaks down the calculation for both your economic and non-economic damages. It all culminates in a specific dollar amount we are demanding.

Negotiation: The insurance adjuster will review the demand and respond. You can bet their first counteroffer will be low—sometimes shockingly so. This is normal. It kicks off a back-and-forth negotiation where we argue the facts and push them to come up to a number that is truly fair.

Mediation or Litigation: If the insurance company refuses to be reasonable and negotiations hit a wall, the next step is often mediation. A neutral third party comes in to help find a middle ground. If that still doesn’t work, we don’t hesitate to file a lawsuit and prepare to take your fight to a jury.

Unmasking Common Insurance Company Tactics

You have to remember what an insurance company is: a for-profit business. Their ultimate loyalty is to their shareholders, not to you. Their goal is to protect their bottom line by paying out as little as they can on every claim, even on the most tragic and clear-cut cases. A good lawyer sees these tactics coming from a mile away and knows exactly how to shut them down.

Be ready for the insurance adjuster to try a few of these moves:

The Quick, Lowball Offer: They might dangle a check in front of you almost immediately. It’s a classic tactic. They know you're grieving, facing unexpected bills, and emotionally exhausted. They’re hoping you’ll grab the "easy" money before you have any idea what your claim is actually worth.

Intentional Delays: Get ready for the stall. Some insurers will drag the process out, asking for the same document five times or just going silent for weeks. They’re trying to wear you down and create financial pressure, hoping you'll get desperate enough to accept a fraction of what you deserve.

Unfairly Shifting Blame: This is one of their favorites. They will look for any possible way to pin some of the blame for the accident on your loved one. Why? Because in Florida, even partial fault can reduce the final settlement amount. It’s a cynical but effective way for them to save money.

An insurance company's first offer is almost never its best offer. It is a starting point in a negotiation designed to test your resolve and see how little you might be willing to accept.

Fighting these strategies is a huge part of what we do. It's not uncommon for families to find themselves tangled up in frustrating insurance disputes that require a dedicated lawyer to cut through the red tape. Our job is to be your shield. We handle every phone call, every email, and every letter from the insurer. We call them out on their bad-faith games and force them to negotiate based on the facts of your case, not on their internal profit goals.

This whole process—from the initial investigation to beating back the insurer's tactics—is about building leverage to get the full and fair compensation your family is owed. You should not have to go up against these massive corporations alone, especially not now.

If you're ready to seek justice and need an experienced advocate to fight for you, we are here to help. In pain? Call Caine.

Common Questions We Hear From Grieving Families

When your family is trying to process an unimaginable loss, a wave of practical and legal questions can make a stressful time feel even more overwhelming. Searching for answers online often just kicks up more dust and confusion.

To help, we’ve put together some direct, straightforward answers to the questions we hear most often from families thinking about a wrongful death claim. Our goal is to give you the clarity you need to feel more grounded as you consider the path forward.

How Long Will This Take?

This is usually one of the first things families ask, and unfortunately, there's no simple answer. The timeline for a wrongful death case depends entirely on the specifics of what happened.

A straightforward case, where fault is crystal clear and the insurance company is cooperative, might settle in under a year. Honestly, that’s not the norm. Most cases are tangled with complexities that require time to unravel correctly.

Several things can slow the process down:

Disputed Liability: If the at-fault party denies they did anything wrong, we have to launch a full investigation and a formal discovery process to prove it.

Complex Evidence: Cases involving things like medical malpractice or a defective product depend on extensive analysis from experts, which takes time to get right.

Multiple Defendants: When more than one person or company might share the blame, sorting out who is responsible for what can delay things.

Going to Trial: If the insurance company refuses to make a fair offer, taking your case to a jury can add a year or more to the timeline.

Complex cases can easily take two years or longer to resolve. While we know that's a frustrating thought, it’s often necessary. We have to be meticulous and build an ironclad case to make sure your family gets the maximum possible compensation.

Will We Have to Pay Taxes on the Settlement Money?

This is a critical concern for families who need to plan for their financial future. The good news is that, for the most part, the core of a wrongful death settlement is not considered taxable income by the IRS.

The IRS generally doesn't tax compensation awarded for personal physical injuries or sickness. This protection extends to wrongful death claims and usually covers the money you receive for:

Lost wages and what your loved one would have earned in the future

Medical bills from before their death

Emotional pain and mental anguish

Loss of companionship and support

The one major exception is punitive damages. If a jury awards these damages—which are meant to punish the defendant for truly egregious behavior, not to compensate your family—that specific portion of the award is usually taxable.

It’s always a good idea to chat with a financial professional or tax advisor about the specifics of your settlement to make sure everything is handled correctly.

What if the Person Who Caused the Death Has No Insurance?

This is a heartbreaking and difficult scenario, but it doesn't automatically mean there’s no way to recover compensation. A dedicated wrongful death attorney won't stop digging just because the most obvious at-fault party is uninsured. There are often other paths to explore.

An attorney will investigate every possibility, which could include:

Uninsured/Underinsured Motorist (UM/UIM) Coverage: If the death was caused by a car crash, your own family’s auto insurance policy might provide coverage.

Third-Party Liability: Was someone else partially at fault? Maybe it was an employer (if the person was working at the time), a property owner (in a negligent security case), or a manufacturer (if a defective product failed).

Personal Assets: This is usually a last resort, but it may be possible to pursue the at-fault individual’s personal assets. Recovery can be difficult, but it's an option.

In these tough situations, it's absolutely essential to explore every single potential source of recovery.

Can I File a Claim for My Unmarried Partner in Florida?

Florida’s wrongful death laws are very specific and, frankly, can be harsh. The right to file a wrongful death claim is strictly limited by statute to a specific list of relatives called "survivors." This list is primarily the person's spouse, children, and parents.

Unfortunately, this means that an unmarried partner, no matter how long or deep the relationship, does not have the legal standing to file a wrongful death claim for their own emotional losses, like pain and suffering or loss of companionship.

There is one potential exception. If the unmarried partner was financially dependent on the person who died, they might be able to make a claim against the estate for the loss of that financial support. This is a very complex area of law that requires a careful legal analysis.

Getting answers is the first step, but taking action is what secures your family's future. The legal system is complicated, but you don't have to face it alone. At CAINE LAW, we fight to get you the justice and compensation you deserve.

For a free, no-obligation consultation to discuss your case, contact us today. In pain? Call Caine.